The Question Every Korean Mortgage Borrower Is Asking Right Now

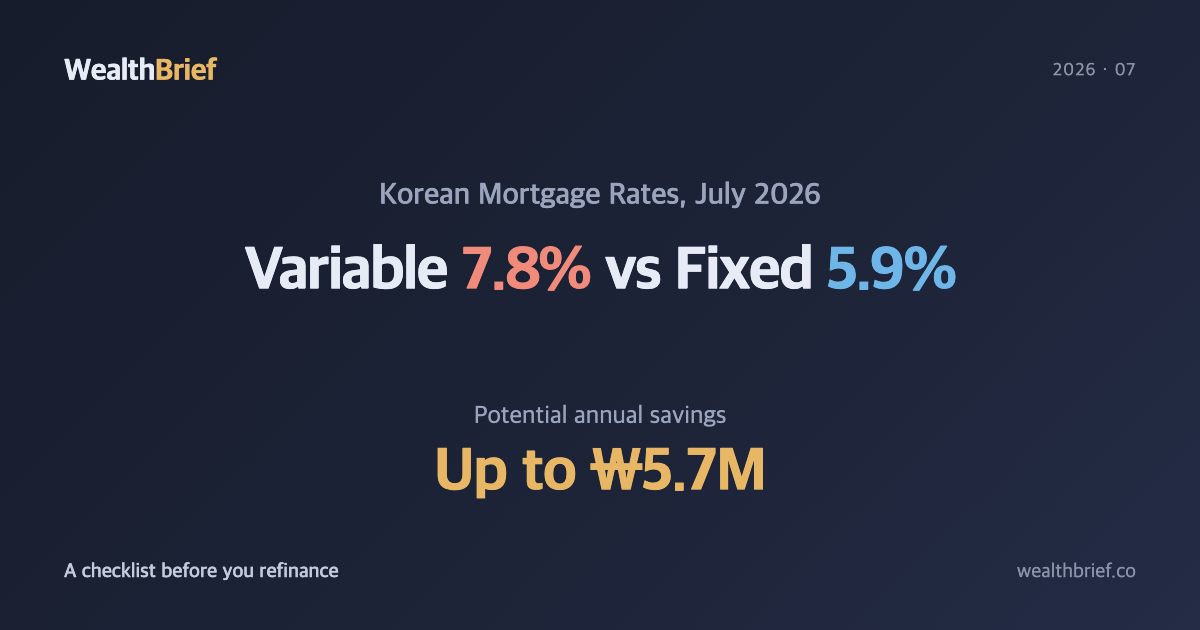

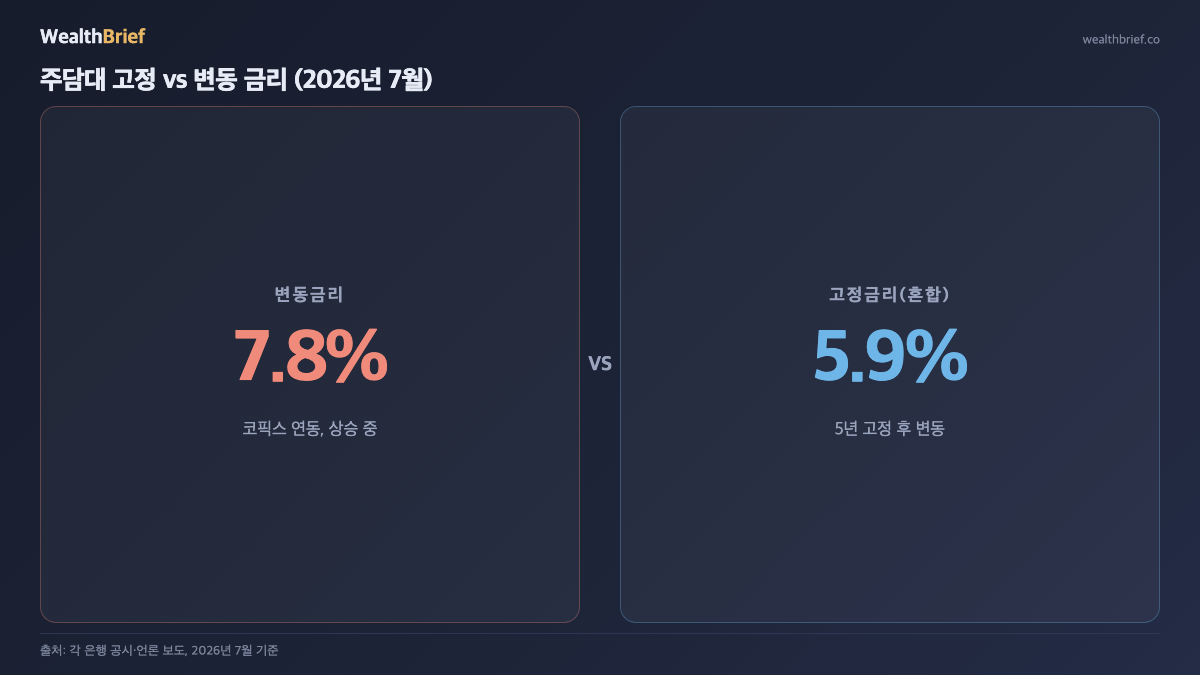

Korean mortgage rates have been climbing hard. By early July 2026, variable-rate home loans at major banks — KB, Shinhan, Kakao Bank — were pushing 7.5 to 8 percent, with some products already breaching the 8% mark. The Korea Housing Finance Corporation (HF) raised Bogeumjari Loan rates by 0.3 percentage points in July, bringing fixed government-backed rates to a range of 4.9–5.2% annually (HF public disclosure, July 2026).

For anyone sitting on a variable-rate mortgage, the math is starting to look uncomfortable. And the question circulating in every finance forum and real-estate chat group is the same: Should I lock in a fixed rate now?

There’s no single answer. But with the spread between variable and fixed widening past 1–2 percentage points in some cases, the calculation deserves a serious look.

Fixed vs. Variable — Where Rates Stand Today

| Product Type | Rate Range (July 2026) | Benchmark |

|---|---|---|

| Variable-rate mortgage (major banks) | ~7.5–8.0% | COFIX (bank funding cost index) |

| Mixed fixed-rate (5-year lock) | ~5.5–6.5% | 5-year financial bond yield |

| Bogeumjari Loan (HF, gov’t-backed) | 4.9–5.2% | MBS (mortgage-backed securities) |

Sources: Individual bank disclosures, Korea Housing Finance Corporation, July 2026. Variable rate ranges based on multiple news reports (Newsis, Hankyung, News1, July 2026) and represent approximate market levels, not guaranteed quotes.

COFIX — the Cost of Funds Index — tracks the weighted average cost of funds raised by Korea’s nine major banks. When market rates rise, COFIX follows, and variable mortgage rates move with it. Fixed (or mixed-fixed) rates are locked to the 5-year financial bond yield at the time of signing. The divergence we’re seeing now is real, and it’s widening.

Three Things to Check Before You Refinance

- Prepayment penalty: Most Korean mortgage contracts charge a prepayment fee of roughly 1.2–1.5% of the outstanding balance if repaid within three years. Past that window, the fee is usually zero or minimal. Some banks have also reduced or waived these fees since 2024 — check your specific contract before assuming.

- Stress DSR recalculation: DSR (Debt Service Ratio) caps the share of annual income that can go toward loan repayments. Refinancing counts as a new loan origination, triggering a fresh DSR assessment under current rules. As of July 2026, Seoul and the broader metropolitan area are under Phase 3 Stress DSR (applying a maximum 1.5 percentage point rate premium to DSR calculations), while non-metropolitan areas remain on Phase 2 through year-end (Financial Services Commission, July 2026). Metropolitan borrowers switching lenders may find their maximum loan amount reduced.

- Fewer lenders to choose from: Insurance companies — historically a secondary source of home loans — have been suspending mortgage products amid the tightening environment (Chosunbiz, July 3, 2026). The refinancing market is getting narrower. Know your options before committing to a process.

What the Numbers Look Like — KRW 300M Loan, 30-Year Term

| Scenario | Rate | Est. Monthly Payment | Est. Annual Interest |

|---|---|---|---|

| Stay variable (current levels) | 7.8% | ~KRW 2.15M | ~KRW 23.4M |

| Switch to mixed-fixed (5-year) | 5.9% | ~KRW 1.78M | ~KRW 17.7M |

| Bogeumjari Loan (if eligible) | 5.0% | ~KRW 1.61M | ~KRW 15.0M |

Illustrative calculation: KRW 300M outstanding balance, 30-year term, equal-principal repayment. Rates are mid-range estimates from the July 2026 market. Actual payments depend on remaining balance, term, and repayment method.

The gap between staying variable and switching to a 5-year fixed comes to roughly KRW 370,000 per month — or KRW 5.7M per year. If the prepayment penalty is KRW 1.8M, you’d break even in about five months. That’s the case for the fixed switch to make sense from a pure math standpoint. The unknown is what rates do afterward.

So — Is Now the Right Time to Switch?

The case for switching is stronger if: your remaining loan term is 15+ years, your current variable rate is above 7.5%, and your prepayment penalty period has already elapsed. There are expectations of eventual rate cuts from the Bank of Korea, but long-term fixed mortgage rates are more sensitive to domestic and US long-bond yields than to the short-term policy rate. Without stabilization in US Treasury yields, domestic fixed rates are unlikely to fall meaningfully in the near term.

The case against switching: if your remaining term is short (under five years), if DSR recalculation would significantly limit your eligible amount, or if the “fixed” product you’re considering only locks the rate for five years — after which it reverts to variable — the protection is more limited than it might seem. That five-year-then-variable structure is the most common form of “fixed” mortgage in Korea. It’s worth being clear-eyed about what you’re actually buying.

The Bogeumjari Loan, at 4.9–5.2%, is the most attractive rate available right now. But it comes with eligibility conditions: home price ceiling (generally KRW 900M or below), income limits, and restrictions around homeownership status. Worth checking against your situation at the HF website before ruling it in or out.

Regional Divergence: One Difference Worth Knowing

Non-metropolitan borrowers are currently operating under Phase 2 Stress DSR rules, while Seoul metro borrowers face Phase 3. This means the DSR headroom for regional borrowers is somewhat wider — potentially making refinancing more feasible. That said, regional banks have also begun raising rates independently in response to regulatory pressure, so the gap may narrow (Daum/Yonhap, July 5, 2026).

A Quick Checklist Before You Make the Call

- ✅ Pull your current contract — what’s your exact variable rate right now?

- ✅ Check prepayment penalty status: still within penalty period? How much?

- ✅ Ask the target bank for a DSR recalculation — will you still qualify for the amount you need?

- ✅ Check Bogeumjari eligibility: home value, income, and ownership status

- ✅ Clarify what happens after the fixed-rate lock period ends

This article is for informational purposes only and does not constitute financial advice or a recommendation to take any specific loan action. Rates and regulations as of July 2026; market conditions change. Consult a qualified financial professional before making decisions that affect your mortgage.

Leave a Reply