One Year of Korea’s June 27 Loan Crackdown — Did It Work?

Exactly one year ago today, South Korea’s financial regulators unveiled a sweeping package of household lending restrictions under what became known as the “6·27 Measures.” The goals were clear: slow down surging mortgage volumes, curb household debt growth, and cool overheated housing prices—particularly in Seoul and the broader metropolitan area. Twelve months later, we have a report card. The short version: mortgages got tighter, but prices kept climbing.

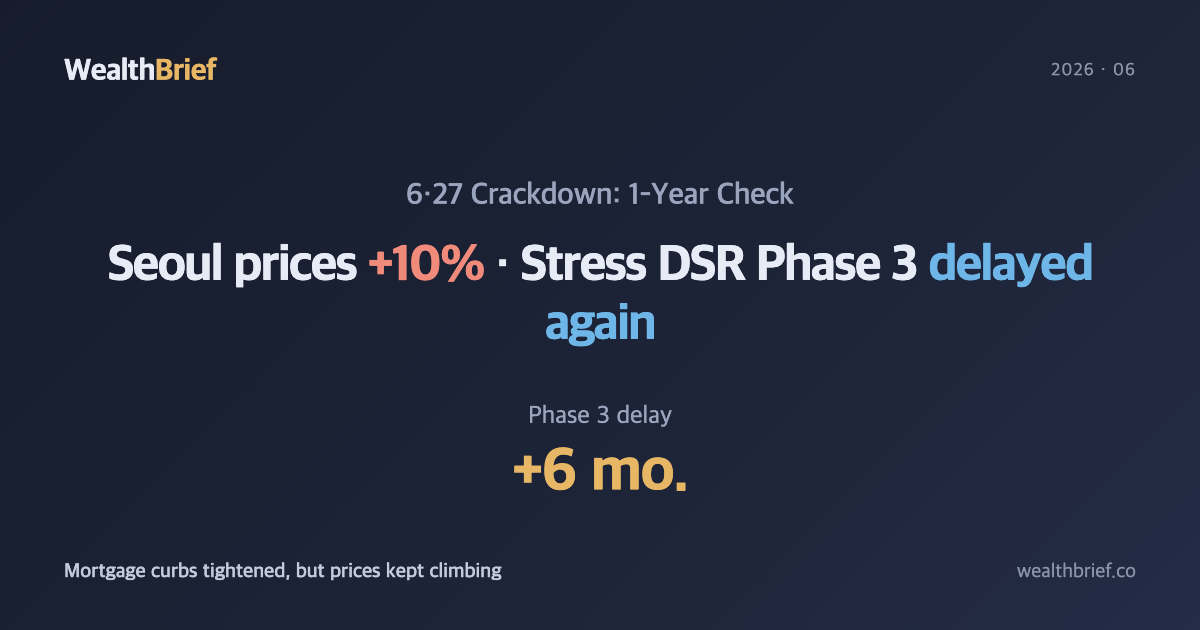

Seoul Apartments Up ~10%, Household Debt Still Growing

According to media reports compiled as of June 2026, Seoul apartment prices rose approximately 10% in the year following the 6·27 crackdown—the opposite of what regulators had hoped to see. Aggregate household debt also failed to shrink meaningfully. Worse, unsecured personal loans (신용대출) reportedly expanded, suggesting that borrowers who hit mortgage walls simply found other channels.

The mechanism is familiar to anyone who’s watched regulatory arbitrage play out elsewhere. When the front door (mortgage windows) gets narrower, demand doesn’t disappear—it looks for side doors. Business-purpose loans and unsecured credit became those side doors. Banks are now tightening post-disbursement checks on business loans to close the workaround, but plugging one leak at a time is slow work when the underlying demand pressure remains intact.

- Seoul apartment prices: approximately +10% since the 6·27 Measures (compiled media reports, June 2026)

- Household debt: aggregate growth continued; unsecured lending rebounded (same sources)

- Bank mortgage windows: alternating open-and-shut cycles throughout H2 2025 and H1 2026

Stress DSR Phase 3: Delayed Again by Six Months

The most immediate development is another postponement of Stress DSR Phase 3. On June 24, 2026, regulators announced a six-month extension of the phase-in deadline, citing weakness in regional construction activity (source: MSN and other Korean media outlets, June 24, 2026).

A quick explainer: Stress DSR (Debt Service Ratio under stress conditions) takes Korea’s standard DSR calculation—total annual loan payments divided by annual income—and applies an additional buffer rate on top of current interest rates to simulate how a borrower would fare if rates rose further. Phase 1 (February 2024) applied this to bank mortgage loans only. Phase 2 (September 2024) extended coverage to bank unsecured loans and non-bank mortgage loans. Phase 3—the final step—would have covered non-bank unsecured lending, effectively closing off every remaining channel from the stress-test framework. That closure is now pushed to at least early 2027.

The reason tells you a lot about the bind policymakers are in. Korea’s housing market is deeply bifurcated: Seoul and its suburbs face supply shortfalls and sustained price pressure, while provincial cities are dealing with unsold inventory, stalled construction projects, and real estate project financing (PF—development loans collateralized against future sales proceeds) under severe strain. Tightening the screws any further risks tipping already-fragile regional builders into insolvency.

What the Loan Market Looks Like Heading Into H2 2026

| Policy Tool | Status (June 2026) | Practical Impact |

|---|---|---|

| Stress DSR Phases 1 & 2 | In effect | Mortgage and bank unsecured loan limits tighter than pre-2024 |

| Stress DSR Phase 3 | Delayed 6 months | Non-bank unsecured borrowers unaffected for now |

| Bank lending quotas | Ongoing | Mortgage windows may tighten again in Aug–Oct |

| Business loan reviews | Intensified | Regulatory arbitrage route narrowing |

Two variables are worth watching in H2. First, interest rate direction: if the Bank of Korea cuts its benchmark rate, the COFIX index (the bank funding cost benchmark that sets variable mortgage rates) should follow, easing the burden on existing variable-rate borrowers. Second, quota burn rates: last year, bank lending quotas filled rapidly in late summer, snapping loan windows shut for weeks at a time. That pattern could repeat.

For Owner-Occupier Buyers: What to Check Now

This isn’t investment advice—it’s a checklist for people making real housing decisions in this environment.

- Run your own DSR math first. Bank-sector DSR limit is 40% of gross annual income. If you’re using a variable rate, the stress buffer is already baked into Phase 1 and 2 calculations—your actual borrowable amount may be lower than a pre-2024 estimate suggested.

- Watch lending window timing. If you have a purchase planned for late 2026, check monthly quota utilization at your target bank starting in July. Windows that closed abruptly last August could do so again.

- Non-bank credit plans: note Phase 3’s new timeline. If non-bank unsecured financing is part of your bridge strategy, factor in that conditions could tighten significantly once Phase 3 takes effect—likely sometime in early 2027.

The Honest Takeaway at the One-Year Mark

The consensus read on 6·27 at its one-year anniversary is that it put a partial brake on mortgage origination but didn’t solve the price equation. Critics argue it failed. Defenders counter that prices might have climbed far more steeply without any intervention—a counterfactual that’s genuinely impossible to disprove.

What’s harder to argue with: a single demand-side policy set cannot fix a supply-side problem. Seoul’s housing stock isn’t growing fast enough to absorb demand. Regulations that restrict who can borrow don’t build apartments. And as long as regional construction remains fragile, full-strength macro-prudential tightening will keep getting deferred—because the same policy setting that cools Seoul cools regional builders who are already on life support.

The Phase 3 delay is a symptom of that bind, not a cause. Expect the tug-of-war to continue through 2027.

This article is for informational purposes only and does not constitute financial, investment, or real estate advice. Loan and property decisions should be made based on your personal financial situation and in consultation with qualified professionals.

Leave a Reply