June 29, 2026: The Day Korea Placed a ₩3,755 Trillion Bet

At 2 p.m. on a Monday afternoon, South Korea’s President Lee Jae-myung took the podium inside the Yeongbingwan banquet hall of Cheong Wa Dae — the former presidential compound turned public venue — flanked by two of the country’s most powerful industrialists: Lee Jae-yong, Chairman of Samsung Electronics, and Chey Tae-won, Chairman of SK Group.[1]

The numbers that followed were staggering. Private investment commitments totaling over ₩3,755 trillion (approximately $2.8 trillion USD at prevailing rates) — roughly 1.6 times South Korea’s entire 2025 GDP. Four new semiconductor fabrication plants (fabs), a physical AI robotics “mother factory,” and gigawatt-scale AI data centers. The event was officially titled Korea’s Three Mega-Projects for the Great Leap Forward National Report, subtitled “From Recovery to Great Leap — Korea’s Decisive Edge.”[2]

The ambition is unmistakable. But between a ₩3,755 trillion announcement and actual silicon wafers rolling off a production line in southwestern Korea, there are power grids to build, water supplies to secure, and hundreds of thousands of skilled workers to recruit. This article unpacks what was announced, what it means structurally, and — just as importantly — where the risks lie.

“Semiconductors, physical AI, and AI data centers form the three-pillar axis of Korea’s great leap. Speed is the only path to survival.”

What Are the Three Mega-Projects?

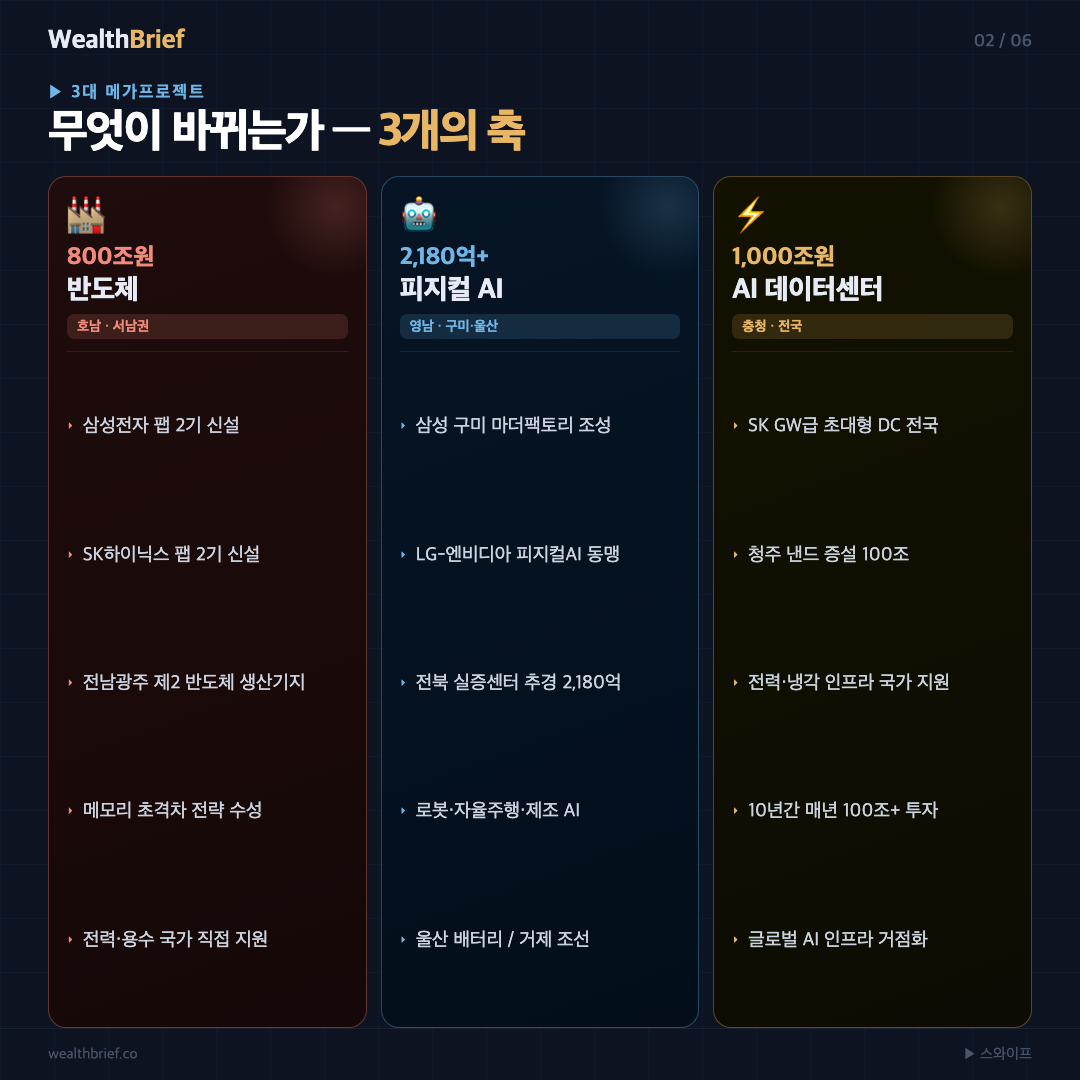

Each of the three pillars has a distinct geography and industrial focus. The Honam region (southwestern Korea, encompassing Gwangju and South Jeolla Province) gets semiconductors. Yeongnam (the southeast, anchored by cities like Gumi, Ulsan, Busan, and Geoje) gets physical AI and robotics. Chungcheong (the central region, centered on Cheongju and the greater Daejeon corridor) gets AI data centers. Together, they form a national industrial map unlike anything Korea has attempted in a single policy push.

① Semiconductors

Location: Gwangju & South Jeolla Province (Honam region; planned South Jeolla-Gwangju Special City)

Core: Four new memory semiconductor fabs — two from Samsung Electronics, two from SK Hynix

Investment: Samsung ₩400T + SK ₩400T = ₩800 trillion total

A fab (fabrication plant) is a semiconductor manufacturing facility requiring ultra-clean rooms and tens of trillions of won in precision equipment. Think of it as a city-sized, dust-free factory where silicon wafers become memory chips.

② Physical AI & Robotics

Location: Gumi, Ulsan, Busan, Geoje — Yeongnam (southeastern Korea)

Core: Samsung’s Gumi Robotics Mother Factory; LG Electronics–NVIDIA physical AI alliance

Government support: K-Robot Physical AI Validation Center — ₩218 billion in supplementary budget (North Jeolla Province)

Physical AI refers to AI systems that don’t just generate text or images — they operate robotic arms, control factory machinery, and navigate autonomous vehicles in the real world.

③ AI Data Centers

Location: Chungcheong region (central Korea) + nationwide

Core: SK Group AI data center investment of ₩1,000 trillion; Cheongju NAND flash expansion ₩100T

Government figure: ₩550 trillion[4]

GW-scale (gigawatt-scale) refers to data centers consuming over one gigawatt of electricity — roughly equivalent to the output of a nuclear power plant, and an order of magnitude larger than today’s biggest Korean data centers.

① Semiconductors — Honam’s Industrial Transformation

Four Fabs, ₩800 Trillion, and the South Jeolla-Gwangju Special City

Korea’s semiconductor industry has, for decades, been synonymous with the greater Seoul metropolitan area and Chungcheong. Samsung’s main fabs sit in Hwaseong and Pyeongtaek; SK Hynix anchors Icheon and Cheongju. The Honam region — the agricultural southwest — has been largely absent from that map.

This announcement changes the coordinates. Samsung Electronics will build two memory semiconductor fabs in the Gwangju–South Jeolla area; SK Hynix will add another two. The combined investment stands at ₩800 trillion (as of June 29, 2026, per Chosun Ilbo).[5] At typical fab construction costs of ₩150–200 trillion per facility, building four simultaneously represents an unprecedented concentration of capital in a single region.

The government will designate the zone as a South Jeolla-Gwangju Special City — Korea’s “Model No. 1” for AI-driven industrial revolution and regional economic development. President Lee pledged to assign a direct presidential attaché to oversee the project personally.[3]

Historical Context: Breaking the Capital-Region Monopoly

Korea’s regional inequality in high-tech manufacturing is not a recent phenomenon. It has accumulated over five decades of centralized industrial policy. If the Honam fab plan proceeds to actual groundbreaking, it would represent the most significant geographic redistribution of Korea’s advanced manufacturing base in the country’s modern economic history.

The cautionary note: in Korean industrial policy, announcements have sometimes outpaced execution. Securing land, water rights, power grid capacity, and environmental permits for a fab complex typically takes three to five years before a single brick is laid. The quality of follow-through matters enormously.

② Physical AI & Robotics — Yeongnam Reinvents Itself

What Is Physical AI? A Plain-Language Explanation

Until recently, AI lived on screens — recommending videos, generating text, flagging fraud in bank transactions. Physical AI is the next stage: AI that reaches into the physical world and operates machinery directly. A robotic arm that teaches itself to pick irregularly shaped objects. An autonomous forklift that adapts its route as warehouse conditions change. A manufacturing line that self-calibrates based on real-time sensor data.

NVIDIA CEO Jensen Huang has positioned physical AI as the defining wave of the next decade, and the LG Electronics–NVIDIA alliance announced alongside these mega-projects is explicitly built on that thesis.[6]

Samsung’s Gumi Mother Factory

A mother factory is not just another production site — it is the originating facility where new manufacturing processes and robotic systems are first developed, refined, and proven before being replicated at plants worldwide. Samsung is building this anchor facility in Gumi, North Gyeongsang Province, alongside a Samsung SDS AI data center on the same campus.

The broader Yeongnam cluster sketched out: Gumi (robotics and AI data center), Ulsan (batteries), Busan (semiconductor packaging), Geoje (shipbuilding). Korea’s traditional heavy industry and automobile corridor is being reframed as an AI-robotics belt.

The K-Robot Physical AI Validation Center

In North Jeolla Province, the government has earmarked ₩218 billion in supplementary budget for a K-Robot Physical AI Validation Center (as reported by Hankyung Business, 2026).[7] The facility is designed to give smaller robotics companies — the ecosystem of startups and mid-sized manufacturers that would otherwise lack access to real factory environments — a place to test and certify their technologies before commercial deployment.

The LG–NVIDIA Alliance: What It Actually Means

When LG Electronics and NVIDIA formalized their physical AI partnership, the substance went beyond a press-release handshake. NVIDIA’s Isaac robotics platform provides the AI training infrastructure; LG’s manufacturing and consumer electronics hardware provides the physical substrate. The combination could span household robots to industrial automation — but the pace of actual product delivery will determine whether this partnership reshapes markets or remains a pilot program.

③ AI Data Centers — What Does GW-Scale Really Mean?

Putting a Gigawatt in Perspective

One gigawatt of power can supply electricity to roughly one million average Korean households simultaneously. Today’s largest Korean data centers operate in the tens-of-megawatts range — one to two orders of magnitude smaller. Training a frontier AI model like GPT-4 consumed an estimated 50 megawatt-hours of energy. Running clusters of such models at scale, continuously, for millions of users, requires the kind of infrastructure that only a handful of facilities worldwide currently provide.

SK Group has committed ₩1,000 trillion to AI data center investment (as of June 29, 2026, per Newspim).[8] The government’s own figure stands at ₩550 trillion (Gyeonggi Ilbo, June 29, 2026) — a gap likely explained by differing time horizons and scope definitions. Either number represents transformative infrastructure spend for a country of Korea’s size.

The Physical Constraints: Power and Cooling

There is no avoiding the engineering reality. GW-scale data centers demand power grid infrastructure that Korea does not currently possess at that scale. The government has committed to national-level support for electricity, water, land, and labor — but transmission line construction routinely encounters community opposition and multi-year permitting delays.

Cooling is the other binding constraint. AI servers generate extreme heat; at gigawatt scale, cooling water consumption becomes a genuine hydrological variable. The water availability of the Chungcheong region will matter in ways that sound abstract in a press release but become concrete during an August heat wave.

In Cheongju, SK Hynix’s NAND flash capacity expansion of ₩100 trillion will proceed alongside the data center build-out, concentrating an extraordinary amount of semiconductor and compute infrastructure in a relatively compact corridor of central Korea.

The Money Map — Investment by Company and Region

Investment Commitments by Group

| Group | Total Domestic Investment | Key Allocations | Source / As Of |

|---|---|---|---|

| Samsung Group | ₩2,655 trillion | Semiconductors ₩2,030T incl.; Honam fabs ₩400T; Chungcheong packaging ₩81T | Gyeonggi Ilbo, Jun 29 2026 |

| SK Group | ₩1,100 trillion | AI data centers ₩1,000T; Honam semiconductors ₩400T; Cheongju NAND ₩100T | Gyeonggi Ilbo, Jun 29 2026 |

| Combined Private Sector | ₩3,755 trillion+ | Samsung + SK; additional groups not yet included | Gyeonggi Ilbo, Jun 29 2026 |

Investment by Region

| Region | Core Project | Investment (est.) | Lead Entity |

|---|---|---|---|

| Gwangju & South Jeolla (Honam) | 4 memory semiconductor fabs | ₩800 trillion | Samsung ₩400T + SK ₩400T |

| Gumi (North Gyeongsang) | Robotics Mother Factory + AI Data Center | Not separately disclosed | Samsung Electronics, Samsung SDS |

| Ulsan / Busan / Geoje | Batteries / Packaging / Shipbuilding AI | — | Samsung affiliates |

| Cheongju (North Chungcheong) | NAND expansion + AI data centers | ₩100 trillion+ | SK Hynix, SK Group |

| Chungcheong (overall) | AI data center cluster | ₩550 trillion (govt. figure) | SK Group-led |

| North Jeolla | K-Robot Physical AI Validation Center | ₩218 billion (supplementary budget) | Government |

Global Comparison — The Semiconductor and AI Arms Race

| Country | Initiative | Scale | Strategic Character |

|---|---|---|---|

| 🇺🇸 United States | CHIPS Act + private AI investment | $52.7B (CHIPS) + $1T+ private | Re-shoring fabs, AI infrastructure build-out |

| 🇨🇳 China | 3rd National Semiconductor Fund | ~$40 billion (2024) | Self-sufficiency push, equipment indigenization |

| 🇯🇵 Japan | Rapidus 2nm program | ¥4 trillion government support | Rebuilding domestic advanced-node capability |

| 🇹🇼 Taiwan | TSMC homeland defense strategy | — | Overseas diversification while defending leading-edge on home soil |

| 🇰🇷 South Korea | Three Mega-Projects | ₩3,755 trillion+ (~$2.8T) | Private-led, state-backed infrastructure; regional industrial rebalancing |

Stock Market Implications — Sector-by-Sector Analysis

The following is a structural analysis of sectors likely to see demand changes — not a recommendation to buy or sell any specific security. This article is not investment advice.

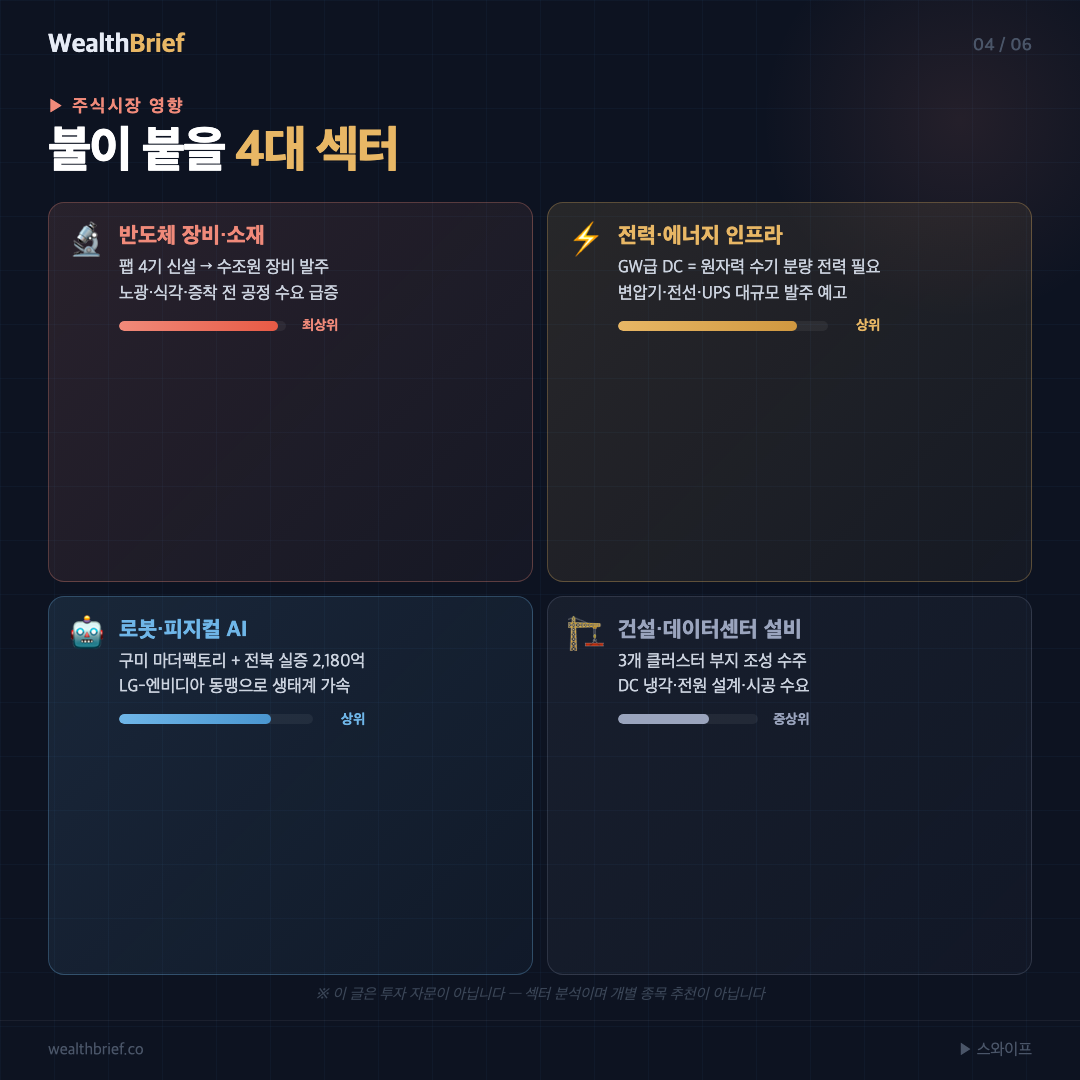

① Semiconductor Equipment & Materials

If four fabs reach groundbreaking, the first and most tangible commercial beneficiaries are likely to be the equipment and materials supply chain. Each fab requires hundreds of piece-types of specialized machinery — EUV lithography systems, etch tools, deposition equipment, and chemical mechanical planarization (CMP) systems. Materials requirements include photoresists, CMP slurries, ultra-pure water, and specialty gases.

Korean equipment and materials companies have cultivated deep relationships with Samsung and SK Hynix over decades. A synchronized four-fab build could create concentrated procurement cycles that pressure capacity across the domestic supply chain. The timing caveat is real: purchase orders follow construction commitments, which follow regulatory approvals.

② Robotics & Physical AI

The Gumi Mother Factory and the North Jeolla validation center create a test-and-diffuse model for industrial robotics adoption. Sectors most likely to see structural demand shifts include collaborative robots (cobots) suited for human-robot shared workspaces, robotic actuators and precision sensors, and robot control software stacks. The LG-NVIDIA partnership’s timeline for commercial product launches will be a meaningful signal for the broader ecosystem.

③ Power Infrastructure

Simultaneously adding GW-scale data centers and multiple semiconductor fabs to the national grid creates an electricity demand shock that Korea’s power infrastructure is not currently configured to absorb quietly. Korea Electric Power Corporation (KEPCO) transmission and distribution investment will likely need to accelerate. Transformer manufacturers, high-voltage cable producers, and power semiconductor components (SiC and GaN devices) are sectors where structural demand could increase materially. Renewable energy integration to serve these facilities adds another demand layer.

④ Construction & Civil Engineering

Industrial cluster development at this scale — site preparation, fab building construction (which requires specialized cleanroom expertise), access infrastructure, and residential support development — represents a multi-decade construction pipeline. Firms with proven cleanroom and data center construction credentials are positioned differently from general contractors.

⑤ Data Center Cooling & Power Systems

At gigawatt scale, cooling efficiency directly determines operating economics. Liquid immersion cooling technology, precision air handling, uninterruptible power supply (UPS) systems, and power distribution units (PDUs) designed for AI workloads are specialized niches where demand could accelerate faster than supply capacity.

Disclaimer: All sector observations above are analytical in nature. They do not constitute a recommendation to trade any security. All investment decisions carry risk and are the sole responsibility of the investor.

Real Estate Market Implications

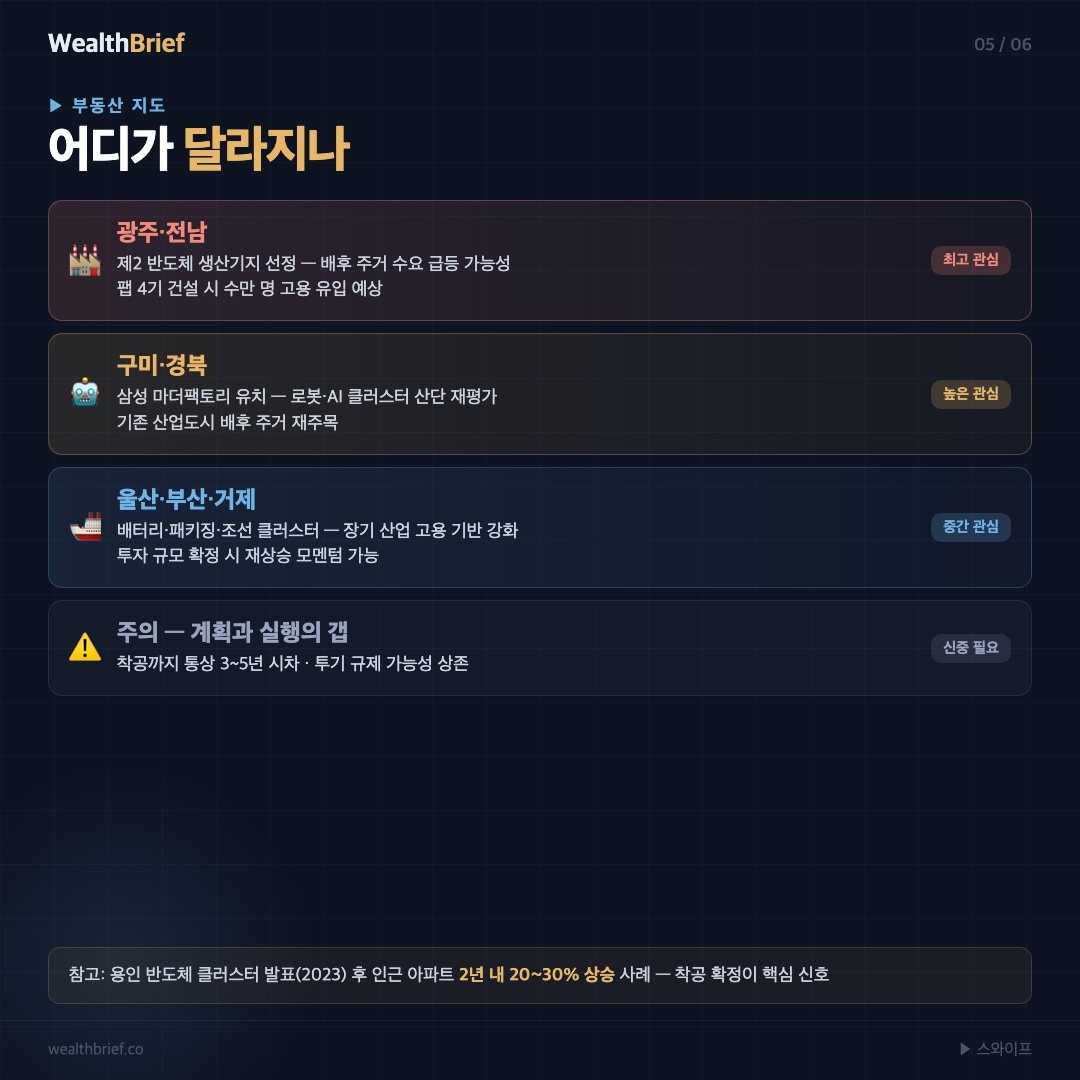

Honam (Gwangju & South Jeolla): Industrial Workforce Housing Demand

A single semiconductor fab employs thousands of engineers, technicians, and support workers, many of whom relocate with their families. Four fabs would generate demand for tens of thousands of housing units in a region that currently lacks the residential infrastructure to absorb that influx. The analog is Samsung’s Pyeongtaek campus: following fab openings there, neighboring Pyeongtaek city saw sustained residential demand that had been largely absent before the facilities arrived.

The risk of front-running this dynamic is that speculative demand arrives before construction workers do. Government intervention — through designation of speculation-control zones — is a standard policy response that could compress short-term price gains in areas perceived to be in the path of the development.

Yeongnam Hub Cities: Gumi, Ulsan, Busan, Geoje

Gumi already has Samsung infrastructure; the Mother Factory announcement opens a new investment cycle for a city that had been experiencing modest population drift. Ulsan and Busan’s battery and packaging additions overlay AI-sector demand on existing heavy-industrial labor markets. Geoje, centered on shipbuilding, is the most speculative of the four — the physical AI-shipbuilding integration story is real but the timeline is the least defined.

Precedent: The Yongin Semiconductor Cluster

When Samsung announced its Yongin semiconductor cluster in 2023, land and housing transactions in adjacent Cheoin-gu and parts of Giheung-gu spiked. But the gap between announcement and actual groundbreaking meant that investors who entered at peak announcement-effect prices faced an extended holding period before demand fundamentals caught up. The pattern suggests distinguishing between announcement-driven price movement and construction-driven demand creation — these are different phenomena with different time horizons.

Key Risk Factors

- Typical timeline from fab announcement to groundbreaking: 3–7 years

- Government may pre-emptively designate overheating districts, capping speculative appreciation

- Project scale reduction or delay would deflate embedded demand expectations

- Korea’s structural population decline means industrial workforce inflow must outpace demographic headwinds in affected regions

Industrial & Social Implications — Talent, Labor, and Ecosystem

The Semiconductor Talent Gap

Building fabs is the easy part — in relative terms. Staffing them is harder. A single fab requires cleanroom process engineers, equipment specialists, yield engineers, and materials scientists, many with graduate-level training. The Honam region’s university ecosystem is not currently configured to produce this talent at scale.

The Samsung Pyeongtaek ramp-up required sustained internal transfer programs that pulled engineers from the Seoul region for multi-year rotations. If the Gwangju fabs follow the same pattern, the “regional development” narrative is more complex than it appears: highly skilled jobs may be filled by relocating workers rather than locally grown ones, at least in the first decade.

Resolving this requires parallel investment in semiconductor-focused universities, graduate programs, and technical training institutions in the Honam region — and those investments need to precede, not follow, the fab groundbreakings.

Physical AI and the Restructuring of Manufacturing Labor

As Gumi-style mother factory technology diffuses through Korea’s manufacturing base, the composition of factory work shifts. Repetitive manual assembly roles contract; robot maintenance, programming, and process engineering roles expand. The transition is not instantaneous — it plays out over a decade or more — but it puts significant pressure on mid-career manufacturing workers who need retraining programs that do not yet exist at adequate scale.

The SME Supply Chain Question

Large industrial clusters historically attract supplier ecosystems — first-tier, second-tier, and third-tier vendors gravitating toward the anchor customer. This can accelerate regional SME development. It can also increase supplier concentration risk: companies built almost entirely around a single chaebol customer lack the resilience to weather that customer’s strategic shifts. The policy design around SME ecosystem development will determine whether this becomes a genuine economic diversification story or a deeper form of chaebol dependency.

Korea’s Strategic Calculus — What This Looks Like from the Outside

Positioning in the US-China Tech Rivalry

The US CHIPS Act is explicitly designed to reduce dependence on East Asian chip production — including Korea’s. China’s semiconductor self-sufficiency drive aims to eliminate dependence on foreign memory suppliers, including Samsung and SK Hynix. These two pressures might seem to squeeze Korea. In practice, they create leverage.

Samsung and SK Hynix together control over 70% of the global DRAM market and a dominant share of NAND flash. High-bandwidth memory (HBM) — the component that gives AI accelerators like NVIDIA’s H100 their computational headroom — is produced almost exclusively by Korean manufacturers. Neither the US nor China can fully execute their AI strategies without Korean memory. That structural dependency is Korea’s primary negotiating asset, and the Three Mega-Projects are designed to entrench it further.

The “Decisive Edge” Strategy: Logic and Limits

The Korean term chogeokccha (초격차), often translated as “decisive edge” or “insurmountable gap,” captures the strategic vision: invest so aggressively in manufacturing scale and technology depth that competitors cannot close the distance within a relevant time frame.

The counterargument deserves honest acknowledgment. Memory semiconductor markets move in brutal cycles — supply gluts regularly follow demand spikes. If the four Honam fabs come online simultaneously into a market where AI-driven memory demand has plateaued or where Chinese producers have made unexpected headway in legacy nodes, the economics deteriorate quickly. A ₩800 trillion fab complex running below capacity is not a regional development engine; it is a liability. Timing the cycle is a problem that even Samsung’s planners cannot solve with certainty.

Optimistic vs. Cautious Scenarios

| Domain | Optimistic Case | Cautious Case |

|---|---|---|

| Semiconductors | AI demand sustains HBM/DRAM supply tightness → fabs reach profitability ahead of schedule | Memory cycle turns down at fab completion → demand-supply mismatch, margin compression |

| Physical AI | Mother Factory validates technology → Korean robotics becomes global reference architecture | Hardware maturity lags AI software → commercialization timeline slips by 3–5 years |

| Data Centers | Global AI companies co-locate in Korea → Korea emerges as Northeast Asian AI hub | Power and cooling infrastructure delays push operational timelines out → SK absorbs stranded capital costs |

| Regional Development | Honam and Yeongnam talent inflows → genuine decentralization of Korea’s economic geography | Skilled workforce remains Seoul-centric → projects staffed by rotating metro workers, local benefit limited |

An Investor’s Monitoring Checklist — Signals That Matter

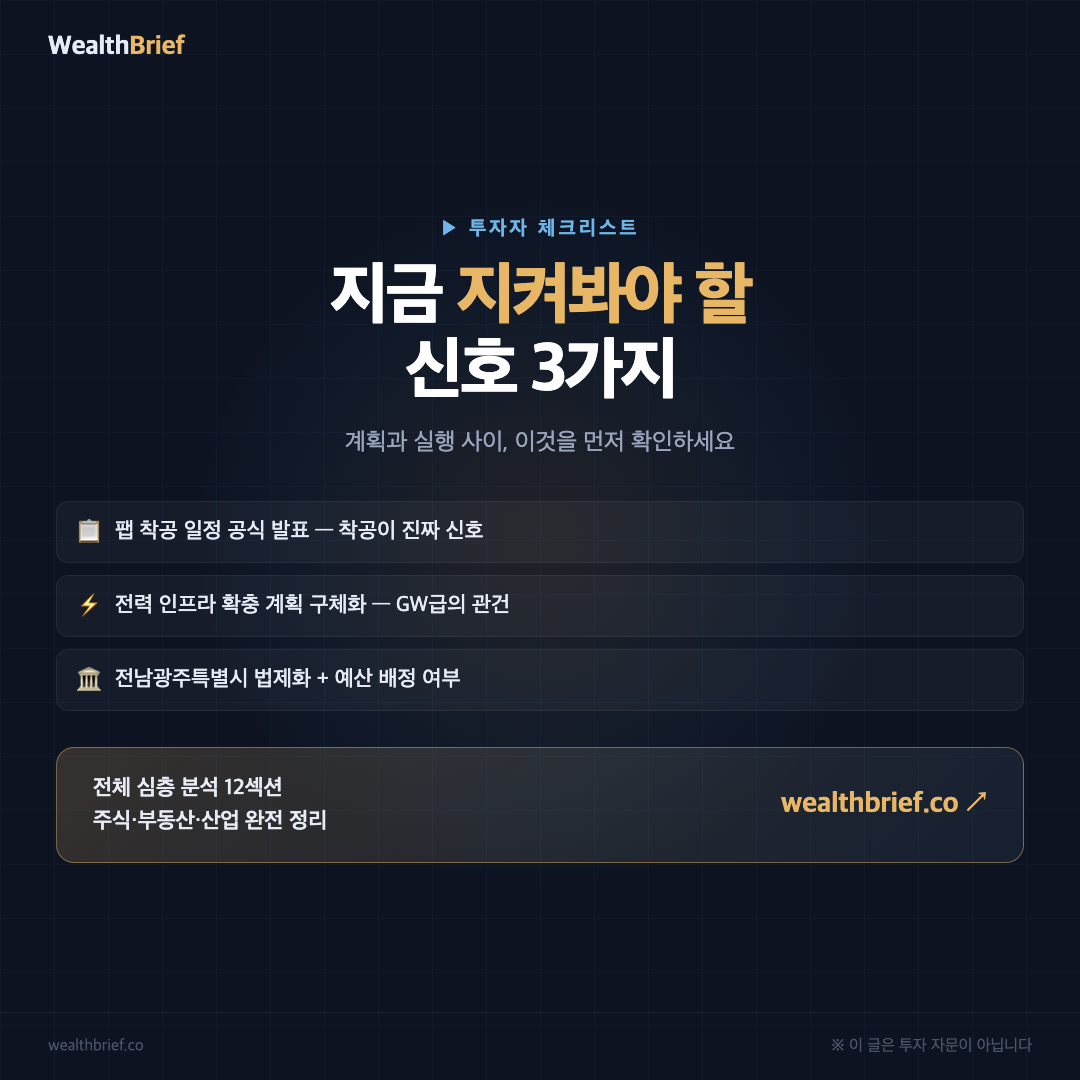

Announcements and execution are different things. The following are concrete signals that, as they materialize, would increase confidence that this program is transitioning from policy statement to industrial reality:

- Official fab construction schedules: A formal, dated groundbreaking announcement — distinct from an investment commitment — is the clearest near-term signal. Watch for public regulatory filings and environmental impact assessments.

- South Jeolla-Gwangju Special City legislation: Parliamentary bill introduction, committee hearings, and passage are sequential milestones. The special city status cannot function without legal foundation.

- Power infrastructure expansion plans: KEPCO capital expenditure disclosures, transmission line routing announcements, and additional generation capacity tenders will indicate whether the electricity math is being solved.

- Presidential attaché appointment for the Honam project: President Lee explicitly committed to assigning a direct oversight official. The appointment and the first budget under that official’s control will signal institutional seriousness.

- Samsung and SK Hynix board-level investment resolutions: Corporate governance filings confirming capital commitment — separate from press conference statements — carry legal and financial weight that announcements do not.

- 2026–2027 supplementary and main budget allocations: The government’s stated infrastructure support must appear as line items in actual budgets. Numbers in press releases are intentions; numbers in appropriations bills are commitments.

Korea’s industrial policy history includes both celebrated successes and quieter retreats from announced programs. The gap between ambition and execution is where investors get hurt. Each item on this list that gets checked off meaningfully raises the probability that the rest follows.

Disclaimer & Sources

This article is not investment advice. All investment decisions are the sole responsibility of the individual investor. This content is informational, based on publicly available media reporting and government announcements as of June 29, 2026. It does not recommend the purchase or sale of any security, real estate asset, or financial instrument. All investments involve risk, including the possible loss of principal. Past market behavior is not a guarantee of future results.

- Yonhap News Agency, “National Report on Korea’s Three Mega-Projects for the Great Leap Forward,” June 28, 2026.

- Kyunghyang Shinmun, “President Lee Jae-myung chairs National Report at Cheong Wa Dae Yeongbingwan,” June 29, 2026.

- Chosun Ilbo; BBS Buddhist Broadcasting System — President Lee Jae-myung remarks, June 29, 2026.

- Gyeonggi Ilbo, “Government announces ₩550 trillion AI data center investment figure,” June 29, 2026.

- Chosun Ilbo, “Samsung ₩400T + SK ₩400T: Four fabs in Honam region confirmed,” June 29, 2026.

- Gyeonggi Ilbo, “LG Electronics–NVIDIA physical AI alliance; Samsung Gumi Mother Factory,” June 29, 2026.

- Hankyung Business, “K-Robot Physical AI Validation Center: ₩218 billion in supplementary budget, North Jeolla Province,” 2026.

- Newspim, “SK Group commits ₩1,000 trillion to AI data centers,” June 29, 2026.

Leave a Reply