1,095 Trillion Won — and Still Climbing

On June 24, 2026, the Bank of Korea released its semi-annual Financial Stability Report. Buried in the data was a record that nobody wanted to see: total financial debt held by Korea’s self-employed sector has hit ₩1,095.5 trillion — the highest figure ever recorded (Bank of Korea, Financial Stability Report, June 24, 2026).

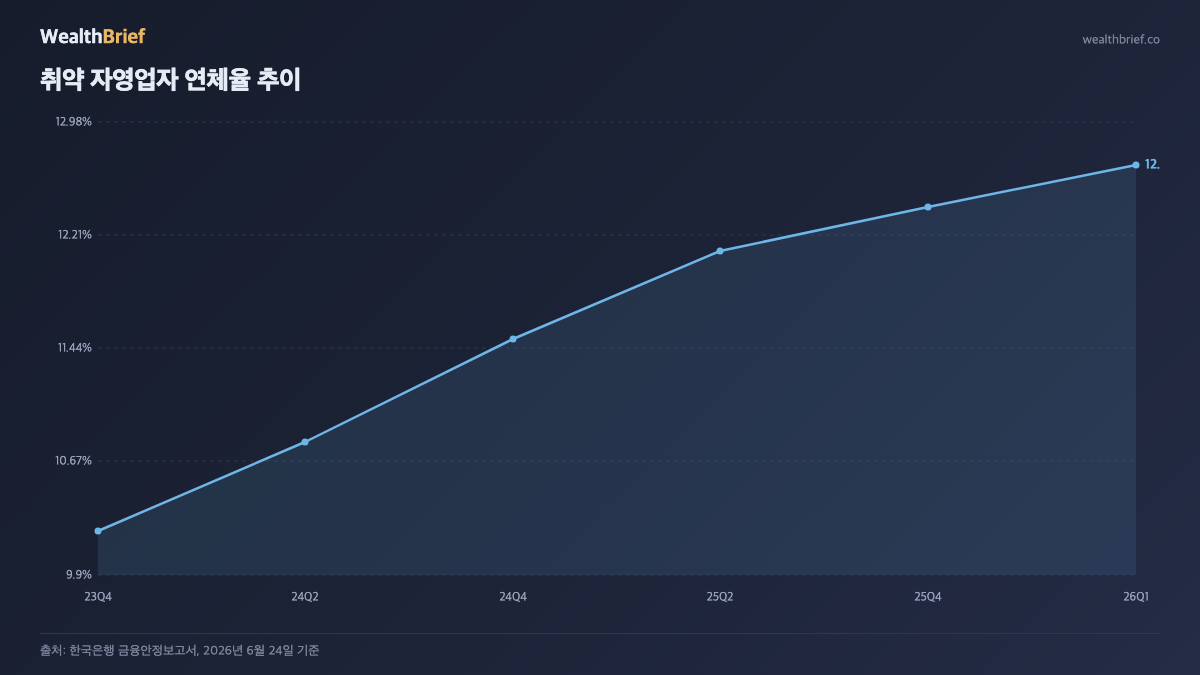

That number alone is alarming. But what the report emphasizes is not just the size of the debt — it’s the delinquency rate among the most vulnerable borrowers. Among self-employed individuals classified as financially vulnerable (those who are low-income, low-credit, or carry multiple loans simultaneously), the delinquency rate stands at 12.68%. More troubling: this marks the 10th consecutive quarter of double-digit delinquency (Chosunbiz, June 24, 2026). For two and a half years, this cohort has not once dipped below 10%.

After the Chicken-Shop Dream — The Aging Trap

The Bank of Korea devoted an entire chapter to a demographic shift that has been building for over a decade. Self-employed borrowers aged 60 and above now hold ₩405.7 trillion in financial debt — a 4.2-fold increase from ₩96 trillion ten years ago (MoneyToday, June 24, 2026).

The story behind this is straightforward. The baby boom generation began retiring from corporate jobs in the early 2010s. Lacking pension income sufficient to sustain their lifestyles, many opened small restaurants, convenience stores, and franchise businesses — funded largely by bank loans and policy-backed credit. Low interest rates at the time made monthly payments manageable.

The rates are no longer low. The businesses, in many cases, are no longer growing. But the debt is still there.

Today, those aged 60 and above account for 41% of all self-employed borrowers in Korea (Chosunbiz, June 24, 2026). Meanwhile, the 20s and 30s cohort has been shrinking — younger Koreans are increasingly choosing employment or gig work over the uncertainty of running a small business. What’s left is an older, more indebted, more financially fragile base.

The Slide Into Non-Bank Lending

When a borrower’s credit deteriorates, the first door that closes is the bank’s. They move to savings banks, credit card loans, and capital companies — collectively Korea’s non-bank sector — where interest rates can run 12–15% annually versus 5–7% at commercial banks. Same principal, double the interest burden.

The Bank of Korea’s June report explicitly flags “non-bank credit quality among the self-employed” as a key risk area requiring monitoring. The concern is structural: borrowers who have already been pushed out of bank lending have few places left to turn if their situation worsens further. And with vacancy rates rising and consumer spending under pressure, the operating environment for small businesses is not improving.

| Indicator | Figure | Source & Date |

|---|---|---|

| Total self-employed debt | ₩1,095.5 trillion (all-time high) | Bank of Korea, Jun 24, 2026 |

| Vulnerable borrower delinquency rate | 12.68% (10th consecutive double-digit quarter) | Bank of Korea, Jun 24, 2026 |

| 60+ self-employed debt | ₩405.7 trillion (+4.2× over 10 years) | MoneyToday / Bank of Korea, Jun 24, 2026 |

| 60+ share of self-employed borrowers | 41% | Chosunbiz / Bank of Korea, Jun 24, 2026 |

| Rental business loan delinquency | +8× over 4 years | MaeIlKyungje, Jun 29, 2026 |

The Landlord Problem Underneath

A related but distinct problem is emerging in small-scale real estate rental businesses. Delinquencies among these borrowers have surged eightfold over four years (Maeil Kyungje, June 29, 2026). Vacancy rates have climbed. Rental income has declined. But the loan balances — often taken out during the cheap-money era — haven’t moved.

The overlap matters. It’s common for Korean self-employed individuals to simultaneously run a small business and own a small commercial property or officetel unit for rental income. When both income streams weaken at the same time, the debt load becomes difficult to service from either direction.

The Rate Hike Signal

Here is the uncomfortable irony. The same Financial Stability Report that documented all of the above also indicated that the Bank of Korea is considering tightening monetary policy — citing the re-acceleration of household debt and housing prices as factors creating financial imbalance (Poss Journal, June 24, 2026).

A rate hike would directly raise the interest burden on variable-rate loans, which make up a disproportionately large share of self-employed and small business financing. The Bank acknowledged this tension by calling for “targeted support for the most vulnerable.” In practice, that phrase signals what policymakers know but can’t say plainly: there isn’t enough capacity to rescue everyone.

Three Questions Worth Asking Now

This is not just macroeconomic background noise. If you have family members, friends, or colleagues running a small business or operating rental property — or if you are doing so yourself — the data in this report makes three specific questions worth revisiting:

- Multiple-lender exposure: Loans spread across three or more financial institutions raise the probability of being classified as a “multi-debt borrower” — a category that faces stricter access to refinancing.

- Non-bank share: If a significant portion of outstanding debt sits in savings banks, card companies, or P2P platforms, a modest rate increase translates to a faster and larger payment shock than it would for bank loans.

- Rental income coverage: For landlords, if vacancy periods have extended beyond three months, it’s worth calculating whether rental income still covers monthly debt service — not at current rates, but at rates 0.5–1.0 percentage points higher.

The Bank of Korea’s numbers describe a system that has been under chronic stress for over two years. The question now is whether a rate hike, if it comes, tips some of that stress from manageable to acute.

This article is for informational purposes only and does not constitute financial or investment advice. Individual circumstances vary; consult a qualified financial professional for guidance specific to your situation.

Leave a Reply