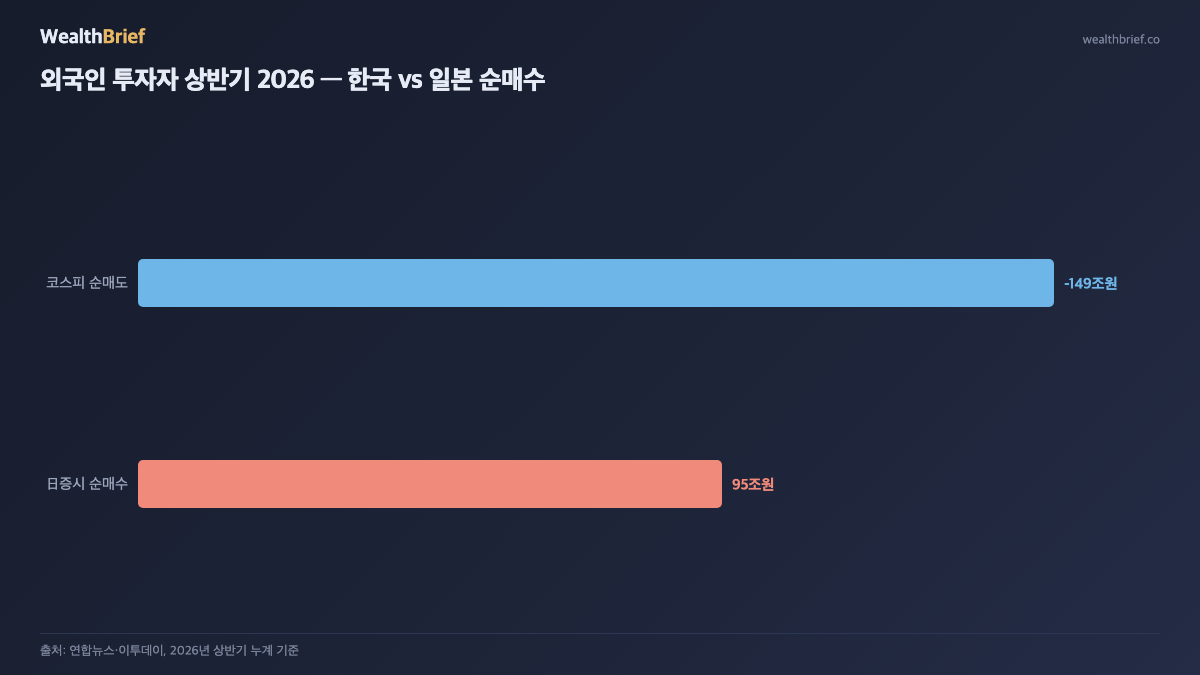

The Numbers First — ₩149 Trillion Sold, ₩95 Trillion Bought

In the first half of 2026, foreign investors sold a net ₩148–149 trillion worth of KOSPI shares (as of July 1, 2026; Yonhap, Maeil Business). Over the same period, Korean retail investors absorbed ₩99 trillion in net purchases, effectively propping up the market. Meanwhile, those same foreign funds were buying a net 10 trillion yen (approximately ₩95 trillion) of Japanese equities — a record high that surpassed even the peak of Abenomics (July 2, 2026; Edaily, Newspim).

The same capital, same time frame: selling Korea, buying Japan. What’s the calculation behind that move?

Three Reasons Foreigners Chose Japan Over Korea

① Yen Weakness + Potential FX Upside

The Japanese yen remained weak throughout H1 2026. Investing in yen-denominated assets with dollars creates a built-in option: if the yen strengthens, currency gains amplify equity returns. Korea offered no comparable setup — the won stayed stuck above ₩1,500 per dollar for 31 consecutive trading days (as of July 2, 2026; Maeil Business), with no clear catalyst for reversal.

② AI Supply Chain Repositioning — Japan’s Materials, Equipment & OSAT Sector

The areas where foreigners concentrated their Japan buying were materials, components, equipment, and outsourced semiconductor assembly and test (OSAT) firms connected to AI infrastructure (July 2, 2026; Newspim). Unlike Samsung Electronics and SK Hynix — which face direct memory cycle exposure — these Japanese firms are one or two steps removed from commodity pricing swings, offering a different risk profile within the same AI-investment theme.

③ Corporate Governance Reform and Rising Dividends

Since 2023, the Tokyo Stock Exchange has been pressuring companies with price-to-book ratios below 1x to improve capital efficiency. By H1 2026, buybacks and dividend hikes were materializing in actual corporate actions, building credibility among global allocators. Japan also sits in the MSCI Developed Markets Index — while Korea, in 2026, saw its DM upgrade bid rejected once again.

Why Foreigners Were Selling a Market That Gained 101%

KOSPI roughly doubled off its 2025 base by mid-2026. Yet foreigners kept selling. Two forces were at work simultaneously:

- Profit-taking and rebalancing: Funds that held heavy KOSPI positions during the rally locked in gains and trimmed overweight Korea positions. When a market doubles, a passive rebalancing mandate alone mechanically generates selling.

- Ownership ratios held up anyway: Despite the ₩149 trillion outflow, foreign ownership stakes in Samsung Electronics and SK Hynix stayed relatively stable in certain periods (May 2026, Yonhap). When share prices rise faster than selling volume, the remaining holdings grow in value — the “sell-Korea paradox” where selling and ownership percentage both coexist.

Will Foreigners Return in H2?

The majority of Korea’s sell-side analysts expect foreign outflows to continue into H2 2026 (July 1, 2026; JoongAng Ilbo). Three headwinds stand out:

- Exchange rate drag: Every day the won sits above ₩1,500, Korean equities lose value in dollar terms. If the rate drifts toward ₩1,600, the dollar-adjusted return profile deteriorates further.

- AI chip demand uncertainty: Meta’s cloud expansion announcement was read by markets as a pivot toward proprietary AI silicon — triggering a 7.89% single-day crash in KOSPI on July 2, 2026, led by semiconductor names. Until demand visibility improves, large foreign re-entry is unlikely.

- Fed rate freeze: The majority of Wall Street banks now forecast no Fed rate cuts in 2026 (Bank of Korea New York Office, July 2026). A firm dollar is structurally unfavorable for emerging market equity inflows, Korea included.

The counter-case: KOSPI in the 7,000–8,000 range looks historically cheap by valuation, and a strong earnings beat from Samsung or SK Hynix could restart foreign buying. That scenario, however, depends on earnings evidence arriving first — not on anticipation.

Three Things Korean Investors Should Check Now

| Item | Current Status | Implication |

|---|---|---|

| Semiconductor concentration | Heavy individual holdings in Samsung & SK Hynix common | Dual risk: earnings cycle + foreign selling → review sizing |

| Won/dollar at ₩1,500+ | 31 consecutive trading days as of end-June 2026 | Reassess foreign asset and dollar-denominated holdings ratio |

| Retail buyer capacity | ₩99 trillion net bought H1 — acting as market backstop | Volatility may expand before foreign flows stabilize |

The fact that foreign capital moved to Japan is not, by itself, a signal to buy Japanese ETFs today. Foreigners have already entered at scale; returns from here depend heavily on the yen’s trajectory and the timing of a potential reversal. Currency and rate direction need to be assessed before acting — that judgment belongs to each investor individually.

This article is for informational purposes only and does not constitute investment advice. All investment decisions and outcomes are the sole responsibility of the individual investor.

Leave a Reply