Wait — Aren’t These All Just “Flexible Savings Accounts”?

If you’ve spent any time in Korean personal finance forums, you’ve seen the debate: parking account, CMA, or MMF for your emergency fund? The three products look nearly identical on the surface — put money in, earn daily interest, pull it out whenever you need. But underneath, the structures are completely different. And those differences matter a lot when it comes to safety, yield, and how fast you can actually get your cash.

This guide breaks down all three as of July 2026, runs a real interest simulation on ₩10 million, and gives you a clear framework for which one fits which type of money.

Three Products, Three Different Structures

Understanding where your money actually goes is the key to choosing correctly.

Parking Account (파킹통장) is a bank deposit product — a high-yield demand deposit offered mainly by Korean internet banks like KakaoBank, K Bank, and Toss Bank. Because it’s a bank deposit, it falls under the Depositor Protection Act. As of September 2025, the protection limit was raised from ₩50 million to ₩100 million per person per institution (Source: Korea Deposit Insurance Corporation, KDIC). Your principal is guaranteed up to that limit even if the bank fails.

CMA (Cash Management Account) is a brokerage account product. Securities firms take your deposited funds and invest them overnight in short-term instruments — most commonly RP (Repurchase Agreements backed by government bonds or high-grade corporate bonds), MMFs, or proprietary notes. There are four sub-types:

- RP-type — The most common. Backed by government or high-grade bonds held as collateral.

- MMF-type — Automatically invested into an MMF (see below).

- Issuance Note-type (발행어음) — The brokerage issues its own short-term notes. Only large, licensed brokerages can offer this.

- Comprehensive Finance-type (종금형) — Operates under a separate comprehensive finance license and does carry deposit protection up to ₩100 million.

With the exception of the 종금형, standard CMA accounts are not covered by the Depositor Protection Act. That said, RP-type CMAs are backed by collateral bonds, which significantly reduces practical risk.

MMF (Money Market Fund) is a fund — a pooled investment vehicle that buys ultra-short-term instruments: call loans, government bonds, certificates of deposit (CDs), and commercial paper (CP). Returns are performance-based, not guaranteed, which means there is a theoretical risk of loss. In practice, Korean MMFs rarely lose principal, but a few did post small losses during the 2008 financial crisis. MMFs are not covered by deposit protection.

Interest Simulation: ₩10 Million Over One Year

The figures below use representative rate ranges observed in the Korean market as of July 2026. Actual rates vary by institution and product — always confirm current rates directly through each provider’s official app or the Financial Supervisory Service’s product comparison tool (finlife.fss.or.kr).

| Product | Observed Rate Range (annual, pre-tax) | Rate Used | Pre-tax Interest (₩10M × 1yr) | After-tax Interest (15.4% withheld) |

|---|---|---|---|---|

| Parking Account (internet bank) | 2.5% – 3.3% | 3.0% | ₩300,000 | ₩253,800 |

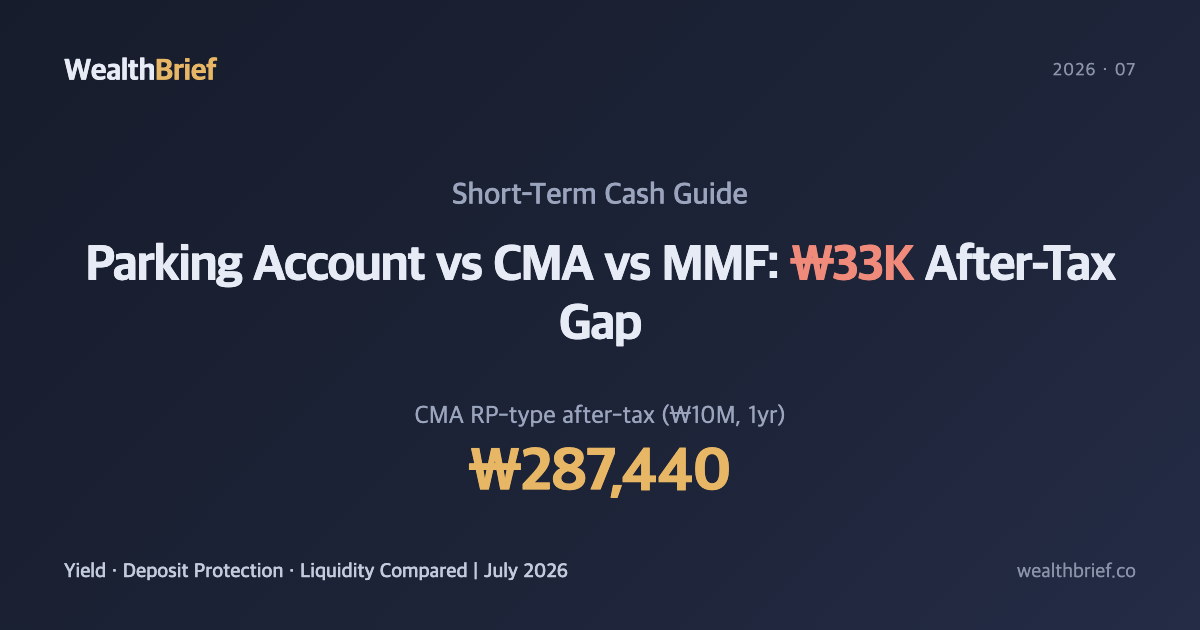

| CMA RP-type (major brokerages) | 3.1% – 3.6% | 3.4% | ₩340,000 | ₩287,440 |

| MMF | 2.5% – 3.0% | 2.8% | ₩280,000 | ₩236,880 |

After withholding tax (14% income tax + 1.4% local tax = 15.4%), the CMA RP-type comes out roughly ₩33,000 ahead of the parking account and ₩50,000 ahead of the MMF on ₩10 million over a year. That gap scales linearly — at ₩100 million, you’re looking at ₩330,000 to ₩500,000 in additional after-tax interest simply by picking the right product.

Deposit Protection: Only the Parking Account Offers Full Certainty

Since the Depositor Protection Act amendment took effect in September 2025, protected funds now cover up to ₩100 million per person per institution. Here’s how the three products stack up:

- Parking Account — Protected ✓ (up to ₩100M)

- CMA 종금형 (Comprehensive Finance type) — Protected ✓ (up to ₩100M)

- CMA RP-type / Issuance Note / MMF-type — Not protected ✗

- MMF — Not protected ✗ (funds are excluded from deposit protection by law)

Unprotected doesn’t automatically mean dangerous. RP-type CMAs are collateralized by government bonds, and Korean MMFs are heavily weighted toward short-term government securities. Real-world default risk is low. But if you’re parking ₩100 million or more, the peace of mind from full deposit protection may be worth the small yield trade-off.

Liquidity: Can You Actually Get Your Money Right Now?

All three are marketed as “liquid,” but the fine print differs:

- Parking Account — Instant transfer via banking app. True real-time availability, including weekends for most internet banks.

- CMA RP-type — Same-day withdrawal available. But large interbank transfers may follow banking business hours; weekend settlement can vary by brokerage.

- MMF — Redeemed at the prior day’s NAV (Net Asset Value). In most cases, redemption proceeds arrive on T+1 (the next business day). If you need cash today, you may need to request redemption yesterday.

The MMF T+1 settlement is the most commonly overlooked detail. If a credit card payment is due tomorrow, don’t count on MMF redemption proceeds arriving in time — request a day early.

Which Product Fits Which Money

No single answer works for everyone. Here’s a practical framework:

- Parking Account — Best for emergency funds you may need immediately, amounts above ₩100 million where deposit protection matters, or people who value simplicity and use the same bank for daily transactions.

- CMA RP-type — Best for stock market dry powder (cash waiting to be invested), or anyone already using a brokerage account who wants slightly higher yield without complexity.

- MMF — Best for planned near-term expenses (1–2 months out) where you can predict when you’ll need the funds. Not ideal as a true emergency fund given the T+1 lag.

Many investors use all three: emergency fund in a parking account, investment float in CMA, and short-term goal savings in MMF. There’s nothing wrong with splitting across products.

One more thing to consider: if your annual financial income (interest + dividends) exceeds ₩20 million, you’re subject to comprehensive income tax. Running high-yield short-term products inside an ISA account (Individual Savings Account) can shelter up to ₩2–4 million in income from taxation. That’s worth a separate look if you’re consistently generating meaningful interest income.

Bottom Line

Parking accounts, CMAs, and MMFs aren’t the same product wearing different names. The parking account gives you the clearest deposit protection; CMA RP-type often offers the highest yield among the three; MMF sits in the middle but requires planning around T+1 redemption. In July 2026’s rate environment, the yield gap between products is meaningful enough to matter — especially on larger sums.

Rates change frequently. The figures in this article are for reference based on July 2026 market observations. Before opening any account, confirm current rates through the institution’s official app or the FSS financial product comparison portal at finlife.fss.or.kr.

This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any financial product. Product terms, rates, and regulations are subject to change — always verify with official sources including the Financial Supervisory Service (fss.or.kr) and the Korea Deposit Insurance Corporation (kdic.or.kr) before making financial decisions.

Leave a Reply