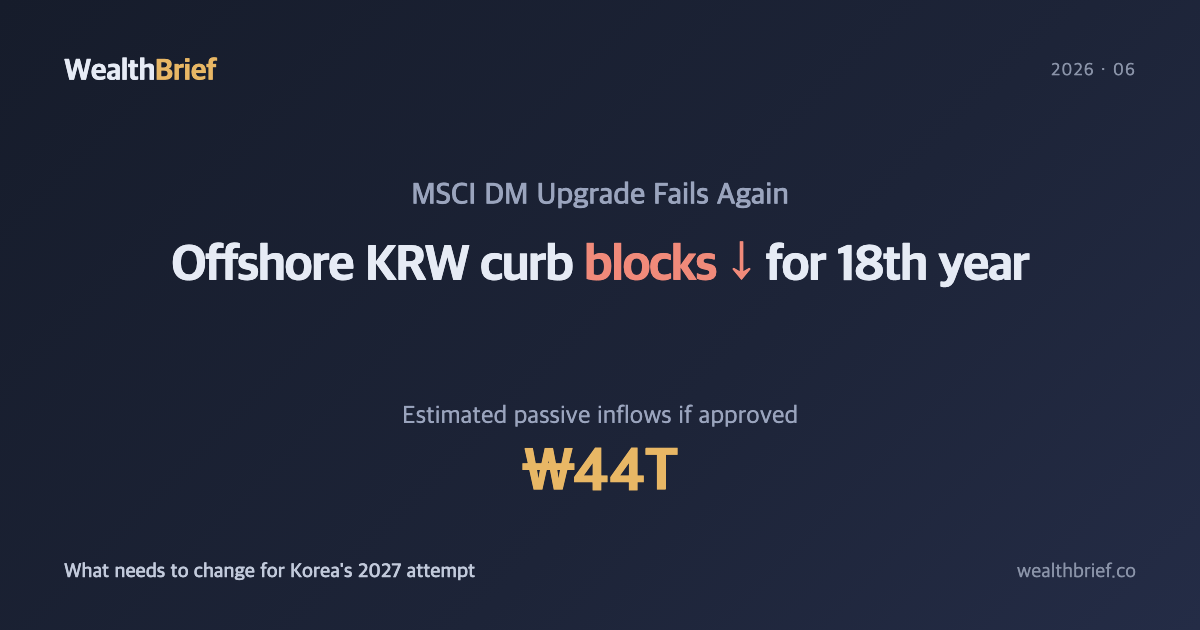

Eighteen Years, Same Answer

On June 23, 2026 (local time), MSCI released its annual market classification review. South Korea was, once again, left off the watch list for the Developed Market (DM) Index. MSCI cited “insufficient foreign exchange market accessibility” as the primary reason, according to Yonhap News Agency (June 24, 2026). Foreign investors responded by selling over ₩4 trillion worth of Korean equities on the day, even as the KOSPI managed a 3% rebound to close at 8,471 (EconomyScience, June 24, 2026). Korea has been aiming at this reclassification since 2008. That’s eighteen years. Same reason. Same result.

So what exactly is the problem? Across multiple news reports, two recurring obstacles stand out: restrictions on offshore KRW trading, and short-selling regulations. Of the two, it was the currency issue that played the decisive role in the 2026 decision.

What Is “Offshore KRW Trading” and Why Does It Matter?

Offshore trading simply means the ability to buy and sell a currency outside its home market, around the clock. The dollar, euro, and yen can be freely exchanged in London, Singapore, or New York at any hour. The Korean won cannot. It can be traded within Korea’s expanded foreign exchange session (currently 9 a.m. to 2 a.m. the following morning), but true offshore settlement — the ability to convert won-denominated proceeds into foreign currency outside of Korean market hours — remains restricted.

This matters enormously for the large passive funds that track MSCI indices. When a fund manager in New York sells Korean stocks at 3 p.m. Eastern time, she needs to be able to settle the trade and repatriate the proceeds in a predictable, frictionless way. Hedging currency risk against a currency that isn’t fully accessible offshore adds costs and complications. Maeil Business Newspaper Market (June 24, 2026) put it directly: “Without allowing offshore won trading, the free movement of foreign capital into and out of Korean equities remains structurally constrained.”

The South Korean government has taken steps. Foreign exchange sessions were extended to near-24-hour trading since 2024. But according to Dailyan (June 24, 2026), the offshore clearing and settlement infrastructure — meaning the plumbing that lets won transactions actually settle abroad — is still not at the level MSCI requires. Improvement at the edges isn’t the same as full convertibility.

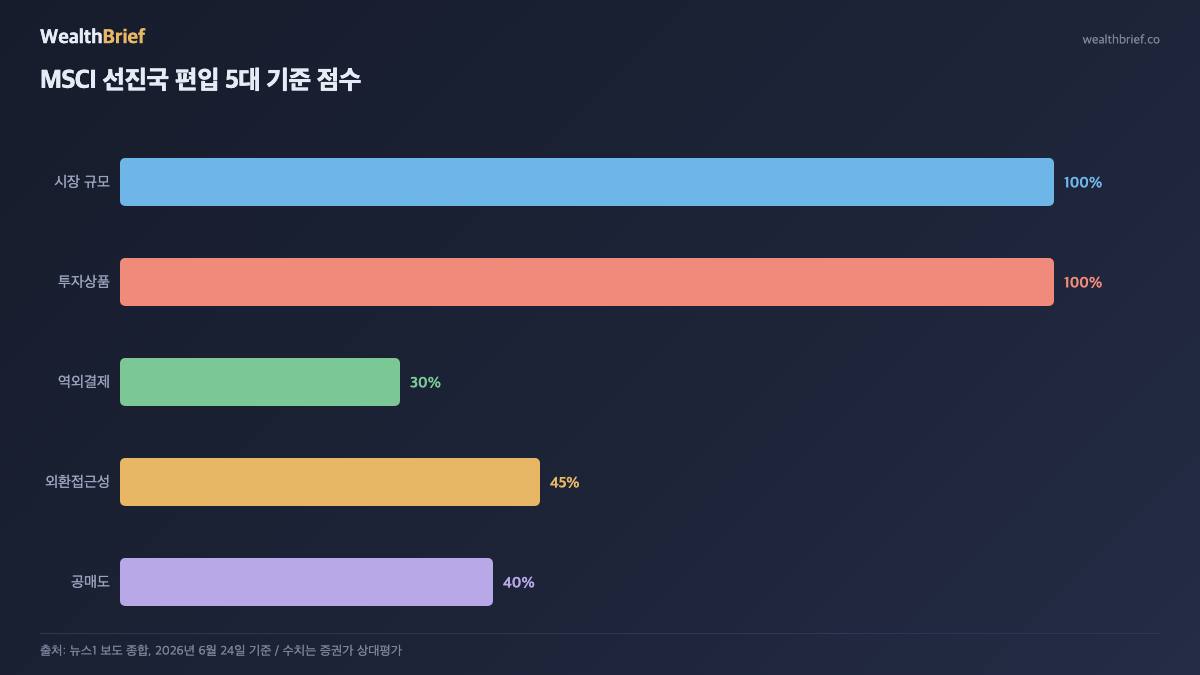

The Five Barriers — Two Cleared, Three Still Standing

| Criteria | MSCI Requirement | Korea’s Status | Assessment |

|---|---|---|---|

| Market size & liquidity | Sufficient scale | KOSPI ranks top 12 globally by market cap | ✅ Met |

| Investment product range | Derivatives, ETFs accessible | Wide range available | ✅ Met |

| Offshore KRW trading & settlement | 24-hour offshore settlement possible | Offshore settlement still restricted | ❌ Insufficient |

| FX market accessibility | Free hedging & conversion | Extended hours but offshore limits remain | ❌ Insufficient |

| Short-selling framework | Global-standard access | Retail short-selling restrictions in place | ❌ Insufficient |

Source: News1 analysis (June 24, 2026), compiled across multiple reports

What Would Inclusion Have Been Worth?

Market analysts had estimated that full inclusion in the MSCI DM Index could bring in up to ₩44 trillion in passive fund inflows (EBN, June 19, 2026; Etoday, June 23, 2026). Even the watch-list announcement alone would likely have triggered anticipatory buying by foreign funds preparing for eventual reclassification.

There is, however, a counterintuitive risk that some analysts highlighted before the announcement. Maeil Business Newspaper (June 17, 2026) noted that a small number of analysts estimated that actual inclusion could cause a short-term outflow of roughly ₩8 trillion. The logic: Korea currently holds a 10–12% weight in MSCI’s Emerging Markets (EM) Index. In the DM Index, Korea would likely account for just 1–2%. The large EM-tracking passive funds — worth hundreds of billions of dollars globally — would be forced to sell Korean equities as Korea exits their benchmark. DM passive money would eventually replace and exceed those outflows, but the transition could be disruptive in the short term. This scenario, for now, remains theoretical.

The Road Ahead

MSCI reviews its market classifications every June. The next window is June 2027. Before Korea can be reclassified as a developed market, it must first be added to the watch list — and that typically requires a minimum of twelve to twenty-four months before the actual reclassification happens. Even if Korea cleared every outstanding issue today, actual DM index inclusion would be 2028 at the earliest.

The prevailing view in the Korean securities industry, per Infostock Daily (June 24, 2026), is that the realistic next target is the 2027 watch-list entry. For that to happen, two things need to move: an amendment to foreign exchange law expanding offshore won settlement, and a meaningful upgrade to the short-selling infrastructure accessible to foreign investors.

What Investors Should Be Checking Now

Despite foreign selling exceeding ₩4 trillion on June 24, the KOSPI closed up 3% at 8,471 — suggesting the market had already priced in a substantial probability of failure. But that doesn’t mean the next few weeks will be smooth.

- Review DM-anticipation exposure: Large-cap Korean IT and financial stocks that ran up partly on MSCI inclusion hopes may carry a premium that is now being repriced. A clear-eyed look at valuation is warranted.

- Currency risk hasn’t gone away: As long as offshore won trading remains restricted, the structural factors that keep KRW volatility elevated will persist. Investors with low foreign-currency asset exposure may want to revisit that balance.

- Mark your calendar for 2027: Anticipatory buying tends to emerge months before the June MSCI announcement. If Korea does make meaningful progress on FX reform, the next cycle’s run-up could begin as early as late 2026.

Eighteen years of the same answer is a policy failure, not a market one. Whether that changes depends on what the Korean government does with its foreign exchange framework in the next twelve months.

Related

- KOSPI’s 9.99% ‘Black Tuesday’ — What Happened the Day After a Record High

- Korea’s Dual Market Sidecar — What Triggered It and What to Check Now

- Korea Leans Toward Hikes While the Fed Eases

This article is for informational purposes only and does not constitute investment advice. Investment decisions should be made based on individual judgment and personal responsibility.

Leave a Reply