June 23, 2026: Both Korean Markets Tripped a Sidecar Simultaneously

On June 23, 2026, the Korea Exchange triggered sidecar circuit-dampeners on both KOSPI and KOSDAQ at the same time — a rare event. KOSPI shed more than 4% and KOSDAQ fell roughly 5% in the opening hours, prompting the exchange to suspend program-sell orders for five minutes on each market. Foreign investors unloaded a net of approximately ₩1.6 trillion in a single session — that figure comes from mid-session data reported by Korea Economic Daily and The Korea Herald on June 23, 2026, and may have shifted by the close. KOSPI briefly breached 8,700 after failing to hold 9,000, erasing an estimated ₩411 trillion in market capitalization on the day (Seoul Times News, June 23, 2026).

The proximate trigger was not a macro shock — no rate surprise, no geopolitical headline. It was semiconductor profit-taking: Samsung Electronics and SK Hynix fell sharply in tandem, pulling the broader index with them (Edaily, Newsis, June 23, 2026).

Sidecar vs. Circuit Breaker: Not the Same Thing

The two mechanisms are routinely conflated. The practical difference matters for any investor watching a down day unfold.

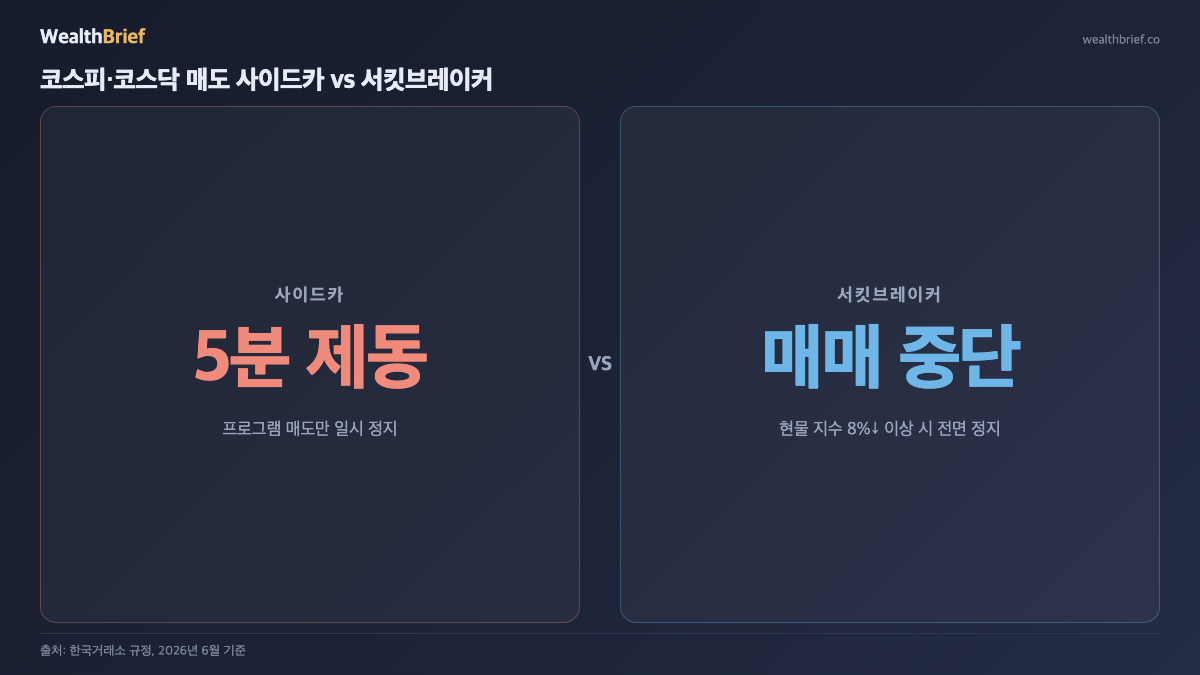

| Feature | Sidecar | Circuit Breaker |

|---|---|---|

| Trigger | Futures price moves ≥ 5% from prior close, sustained 1+ minute | Spot index drops 8%, 15%, or 20% from prior close |

| Effect | Program sell orders suspended for 5 minutes only | All trading halted (20 minutes to full-day) |

| Retail orders | Unaffected — individual orders still execute | Fully halted |

In plain terms: a sidecar is a brief brake on algorithmic program selling, not a pause button on the entire market. Retail and institutional discretionary orders continued to execute throughout Tuesday’s session (CBC News, Herald Economy, June 23, 2026). If your sell order went through during the sidecar window, that is exactly how the system is designed.

What Actually Drove the Selloff

The setup was visible from the day before. On June 22, KOSPI closed at the 9,100 level and SK Hynix briefly overtook Samsung Electronics as the largest stock by market cap — the culmination of a narrow “half rally” driven almost entirely by two semiconductor names (Aju Business Daily, Daum Finance, June 22, 2026). When foreign investors decided the short-term move was exhausted, both stocks dropped in synchronized fashion on June 23, and the program-sell algorithms amplified the move fast enough to trigger the sidecar mechanism.

The pattern is structurally significant: the same two stocks that pulled KOSPI above 9,000 were responsible for dragging it back below that level. That concentration risk is the central issue — not the index level itself.

Related: Korea’s KOSPI Half-Rally: What It Means for Your Portfolio | KOSPI at 9000 — Portfolio Checkup

The Structural Vulnerability Behind the Numbers

A market in which two stocks account for an outsized share of total capitalization is inherently more fragile to concentrated selling. When foreign investors — who held roughly ₩1.6 trillion in net sell pressure in just one session — reverse direction on the semiconductor thesis, the index has very little cushion from other sectors to absorb the blow. The sidecar bought five minutes. It did not change the underlying weight distribution.

Historical episodes of semiconductor-driven profit-taking in Korea have resolved in different ways: some recovered within weeks as earnings revisions came in; others extended into multi-month corrections. The current outcome is not yet determinable from the available data.

Practical Checkpoints for Your Own Portfolio

These are general analytical considerations, not personalized investment advice. Individual circumstances vary.

- Semiconductor concentration: If Samsung and SK Hynix together exceed 30% of your equity exposure, your portfolio will swing more sharply than the index on days like today. Whether that concentration is appropriate depends on your own risk parameters, not on today’s price action alone.

- ETF layering: Holding a KOSPI or semiconductor ETF alongside individual positions in Samsung or Hynix often means more semiconductor exposure than the headline weight suggests. Worth quantifying explicitly.

- Panic vs. rebalancing: Selling during a sidecar event and selling because your target allocation has drifted are different decisions with different logic. The former is reactive; the latter is procedural. Most portfolio frameworks distinguish between the two.

- Currency offset: Large foreign sell flows typically pressure the Korean won as well. Investors with dollar-denominated assets or overseas equities may find the FX movement partially offsets domestic equity losses in home-currency terms. See our analysis of the won at ₩1,500+ territory.

What to Watch From Here

Sidecar activations are not inherently alarming — they are a designed feature of the market’s plumbing. What matters is the reason behind the speed of the move. This time, the catalyst was concentration unwinding, not a macro discontinuity. Whether KOSPI reclaims 9,000 quickly or continues to correct depends on whether foreign selling pressure is exhausted or ongoing, and on whether Samsung and SK Hynix earnings revisions give the semiconductor thesis new legs.

Neither question has a clear answer today. What is observable: a market that rallied on two names is now correcting on those same two names. The appropriate investor response is not a directional bet on the outcome — it is a clear-eyed inventory of where your current exposure actually sits.

This article is provided for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. All data is cited as of June 23, 2026, and is subject to revision as markets close. Investment decisions and their outcomes are the sole responsibility of the individual investor.

Leave a Reply