Micron’s 15x Profit Surge: What It Actually Means for Korea’s Chip Stocks

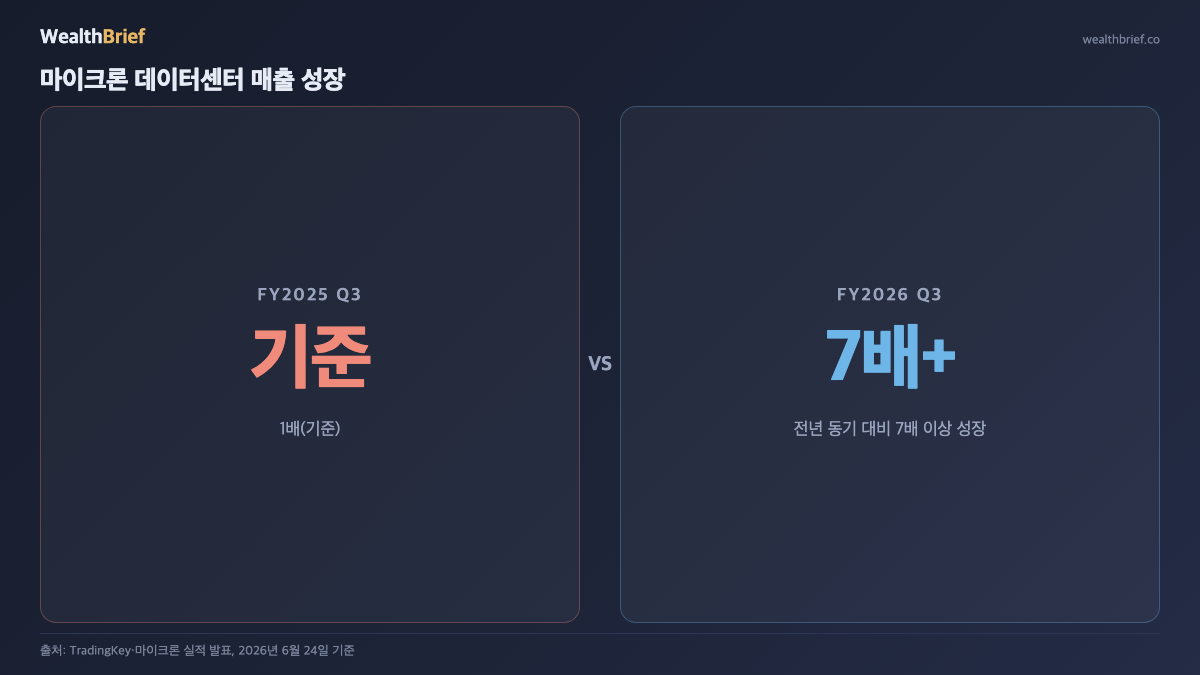

On June 24, 2026, Micron Technology (MU) reported its fiscal Q3 results — and the numbers were hard to ignore. Net income surged roughly 15-fold year-over-year (Financial Times, June 24, 2026), EPS came in $4.62 above Wall Street’s consensus estimate (Investing.com, June 24, 2026), and data center revenue — the segment powering the AI boom — grew more than 7x compared to the same period last year (TradingKey, June 24, 2026). Micron’s stock jumped 15% in after-hours trading (CNBC, June 24, 2026).

This is more than a U.S. chip story. Micron, Samsung, and SK Hynix together control the global DRAM and NAND market. When Micron’s management guided that the chip shortage will persist beyond 2027 (WSJ, June 24, 2026), they were indirectly setting expectations for the entire memory semiconductor industry — including Korea’s two dominant players.

Why AI Memory Demand Is Different This Time

The memory required to run AI workloads has little in common with what goes into a laptop. A single Nvidia H100 GPU carries 80GB of HBM2e; an AI training rack stacks thousands of gigabytes across dozens of accelerators. Micron CEO Sanjay Mehrotra put it plainly on the earnings call: “Memory today is where GPU was three years ago” (Benzinga, June 24, 2026). The implication — memory has become the structural bottleneck in the AI supply chain, the same role that GPUs played when that craze kicked off in 2023.

The blowout earnings were driven not by consumer PCs or smartphones, but by data center memory — primarily HBM and server DRAM. Demand is outrunning production capacity, and Micron said so directly. That supply-demand imbalance, projected to last into 2028, is what sent Wall Street into a frenzy.

How Korean Chipmakers Responded

On June 25, SK Hynix surged 12% on the Seoul exchange. The catalyst was doubled: Micron’s blowout earnings landed the same day SK Hynix announced plans for a blockbuster Nasdaq ADR listing in the United States (CNBC, June 25, 2026). Samsung Electronics also moved sharply higher. As one Korean financial publication put it, Micron “lit a pillar of fire” under domestic semiconductor names.

The next day, however, KOSPI plunged 5.81%, triggering circuit breakers after Apple announced sweeping price hikes in response to tariffs. The semiconductor tailwind evaporated in 24 hours. This sequence matters: macroeconomic shocks can override sector-specific positives almost instantly in today’s market environment.

Does Micron’s Gain Automatically Mean Korea’s Gain?

The bullish case for SK Hynix and Samsung is intuitive. If Micron’s data center revenue grew 7x, the same structural demand applies to SK Hynix — the dominant supplier of HBM3e to Nvidia’s Blackwell GPU platform — and to Samsung, which is working through HBM3e qualification. The rising tide should lift all boats.

But the picture is more complicated than that. Micron is an American company, which means different exposure to geopolitical risks. U.S.-China export controls on advanced chips, for instance, affect Samsung and SK Hynix’s China-based operations more directly. More importantly, Micron’s HBM production ramp is a competitive threat to its Korean rivals in the medium term, not just a positive signal. If Micron captures a larger share of HBM3e orders going forward, that comes at someone else’s expense.

| Factor | Micron (U.S.) | SK Hynix (Korea) | Samsung Semiconductor (Korea) |

|---|---|---|---|

| HBM Market Position | Expanding HBM3 supply | Lead supplier of HBM3e to Nvidia | HBM3e qualification ongoing |

| Data Center Revenue Growth | +700%+ YoY (FY26 Q3) | Record earnings expected in 2026 | Recovery trend, figures pending |

| Geopolitical Risk | Lower (U.S. domicile) | Medium (some China export limits) | Higher (significant China fab exposure) |

Bank of America’s $1,500 Target and the Bull Case in Full

On June 23, 2026 — the day before earnings — Bank of America raised its Micron price target to $1,500, citing the structural durability of AI memory demand (BeInCrypto, June 23, 2026). It is a bold call, and the underlying thesis is not without merit: AI infrastructure spending is being driven by hyperscalers with multi-year capex commitments, not by consumer mood swings.

Still, the bear case deserves a hearing. Micron’s stock surged 15% on earnings night, then closed down 6% two days later after Apple’s tariff-driven price hike wiped out the tech rally (CNBC, June 26, 2026). Memory semiconductors have one of the most violent business cycles in all of manufacturing — a pattern of shortage → overinvestment → glut → crash that has repeated across multiple decades. Whether AI demand has broken that cycle permanently, or simply extended the upturn’s duration before an eventual, larger correction, is a question that no one can answer with certainty yet.

What This Means if You Hold Korean Chip Stocks

For investors holding Korean semiconductor exposure, the Micron report is useful context. Funds heavily weighted to SK Hynix — such as TIGER Semiconductor or KODEX Semiconductor ETFs — have the most direct leverage to the HBM demand surge. Products with heavier legacy DRAM or NAND exposure will see a different risk-reward profile, even if they carry the same “semiconductor” label.

One practical note: the KOSPI is trading in volatile territory near the 9,000 level as of late June 2026. As this week’s whipsaw demonstrated, global macro factors — tariffs, Fed policy, geopolitics — can override chip-specific fundamentals over short timeframes. Analyzing whether the cycle favors memory stocks is a question about direction; managing a portfolio through that cycle is a separate question about timing and position sizing. Conflating the two is where most investors get into trouble.

This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on individual financial circumstances and risk tolerance.

Leave a Reply