When Markets Rally and Rates Rise, What Should You Check First?

The KOSPI crossed 9,000 in June 2026. The Bank of Korea began officially signaling a rate hike. The won-dollar exchange rate averaged over 1,500 for the first time since the 1997–98 financial crisis (Yonhap News, June 28, 2026). Amid all this noise, the question most Korean investors should be asking isn’t “where do I put my money?” — it’s “which account structure do I use?”

Korea’s three main tax-advantaged accounts — ISA (Individual Savings Account), Pension Savings (연금저축), and IRP (Individual Retirement Pension) — are legal frameworks for reducing the tax drag on investment returns. Same returns, different containers, different after-tax outcomes. In a rising rate environment, this gap widens. Higher rates mean more interest income, which means higher tax exposure on that income — unless it’s sheltered inside one of these accounts.

ISA: Korea’s Tax-Free Investment Wrapper

The ISA (Individual Savings Account) bundles deposits, funds, ETFs, and bonds into a single account where net gains are subject to tax benefits rather than being taxed asset by asset. Gains and losses are netted — if you earn ₩2 million on one fund and lose ₩1 million on another, only the net ₩1 million counts for tax purposes.

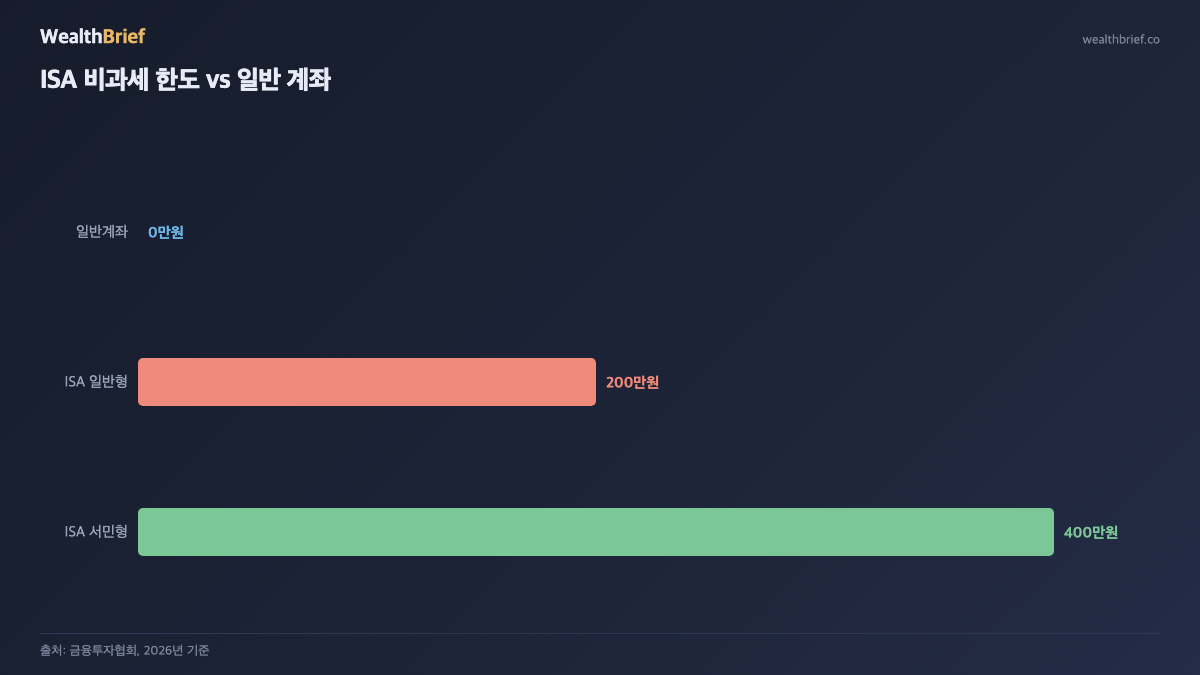

- Tax-free ceiling: ₩2 million (general), ₩4 million (low-income earners with annual salary ≤ ₩50 million)

- Above the ceiling: 9.9% flat tax — lower than the standard 15.4% on financial income

- Minimum holding period: 3 years (withdraw early and the tax benefits disappear)

- Pension rollover bonus: Roll matured ISA funds into a pension account and get an additional 10% tax deduction on the transferred amount (up to ₩3 million)

In a rate hike environment, the ISA edge becomes clearer. A regular savings account earning ₩1 million in interest gets ₩154,000 withheld at source (15.4%). Inside an ISA with the ₩4 million tax-free allowance? That ₩1 million is fully sheltered. Same deposit, same rate — different after-tax result.

Pension Savings (연금저축): Two Benefits at Once

The Pension Savings account (연금저축) provides a tax credit on contributions and defers tax on investment gains until retirement withdrawal. It’s the engine for compounding without annual tax friction.

- Annual contribution limit: ₩18 million (combined with IRP)

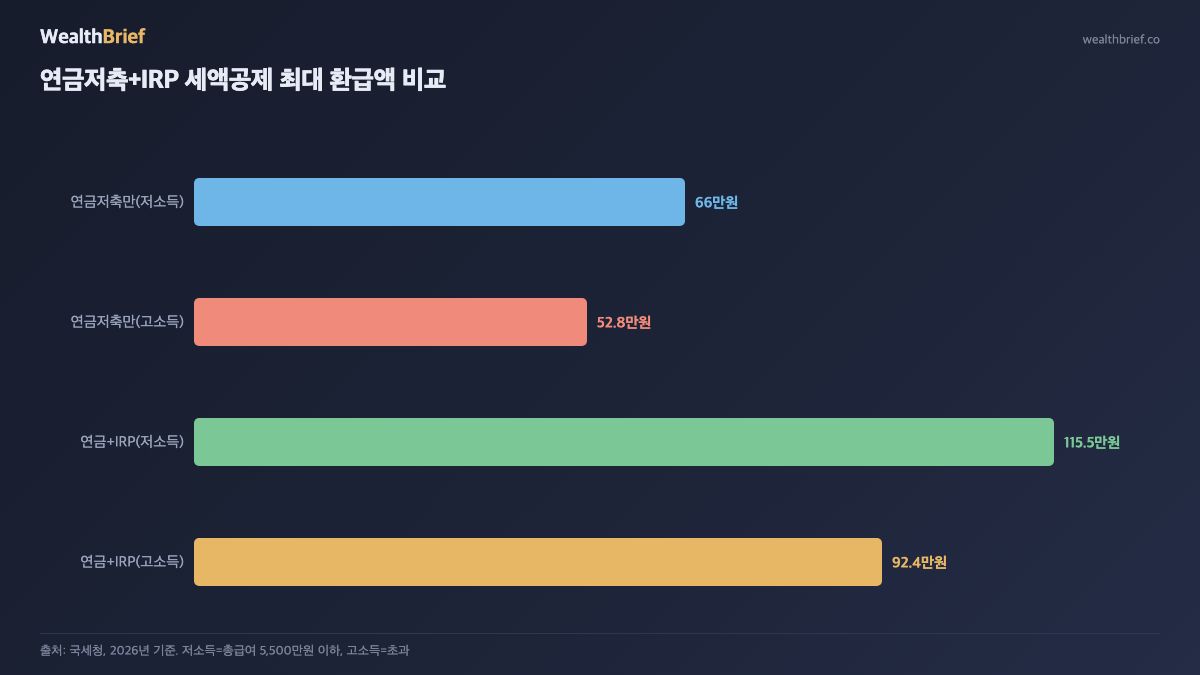

- Tax credit base: Up to ₩4 million for Pension Savings alone

- Tax credit rate: 16.5% for annual salary ≤ ₩55 million; 13.2% above

- Maximum annual refund (Pension Savings only): ₩4 million × 16.5% = ₩660,000

The catch: withdraw before age 55 and you’ll owe 16.5% as miscellaneous income tax — effectively clawing back every tax credit you received. This account is designed for the long game; only money you’re genuinely comfortable locking away belongs here.

IRP: The Extra ₩300 Million Slot

The IRP (Individual Retirement Pension) sits alongside Pension Savings and pushes the combined tax credit base from ₩4 million to ₩7 million. It’s the extension cord that adds ₩3 million more in tax-deductible space.

- Combined Pension Savings + IRP tax credit ceiling: ₩7 million

- Maximum refund (salary ≤ ₩55 million): ₩7 million × 16.5% = ₩1,155,000

- Maximum refund (salary > ₩55 million): ₩7 million × 13.2% = ₩924,000

One IRP-specific constraint: equity assets (stock funds, equity ETFs) can only occupy up to 70% of the portfolio. The remaining 30% must be in principal-guaranteed products — deposits, bonds, money market funds. In today’s rate environment, that mandatory 30% conservative allocation is actually less of a penalty than it used to be.

The Sequencing Question: Which Account First?

If you can’t fully fund all three accounts at once, sequencing matters. The commonly followed priority order (for reference only — individual circumstances vary):

| Priority | Account | Reason | Annual Target |

|---|---|---|---|

| ① | Pension Savings | Highest tax credit efficiency; low 3.3–5.5% tax on withdrawals at retirement | ₩4 million |

| ② | IRP | Adds ₩3 million more deductible space once Pension Savings is maxed | ₩3 million |

| ③ | ISA | Flexible, accessible after 3 years; tax-free wrapper for surplus savings | Remaining surplus |

One important caveat: if you think you might need access to the money within five years, ISA should come before IRP. IRP withdrawals before retirement are restricted by law and carry tax penalties. ISA is accessible after three years without those complications.

Rate Hikes and These Accounts: What Changes?

As the Bank of Korea moves toward rate hikes, household loan rates have risen for three consecutive months as of June 2026 (Gangwon Ilbo, June 2026). The implication for tax-advantaged accounts isn’t obvious at first glance, but it matters.

Inside an ISA, short-term bond ETFs and money market funds benefit from rising yields — and the interest income stays sheltered from the 15.4% tax. Inside Pension Savings and IRP, TDF (Target Date Fund) products automatically shift toward more fixed income as the market environment evolves; rate hikes eventually mean higher bond yields on newly issued debt, which is favorable for these long-duration accounts.

A common concern: “Won’t bond prices fall as rates rise?” Short-term, yes. But these accounts operate over 10–20 year horizons. Locking in higher yields now, then benefiting from capital gains when rates eventually decline, is a strategy worth understanding — though not a guarantee, since no one can reliably predict the rate path ahead.

Three Mistakes Worth Avoiding

① Withdrawing from ISA before the 3-year mark. All tax benefits evaporate. You end up with a regular account that just had some administrative restrictions attached to it.

② Breaking open a Pension Savings account before age 55. Tax credits received get effectively reversed through a 16.5% penalty tax. The math usually doesn’t work in your favor.

③ Stopping contributions at the tax credit ceiling. Beyond the ₩7 million deductible ceiling, contributions up to the ₩18 million annual limit still benefit from tax-deferred compounding. No credit, but no annual tax on gains either — still worth it if you have the cash.

Three Things to Check Right Now

- How much have you contributed to Pension Savings and IRP so far this year? If the combined ₩7 million hasn’t been reached, set a plan to hit it before December 31.

- Do you have an ISA? The 3-year clock starts on the day you open it. Open it now and it’s accessible from 2029 onward. Delay costs you years.

- What’s inside your tax-advantaged accounts? In a rate-rising environment, short-term bonds and money market instruments within ISA or the fixed-income portion of IRP are worth a look — though always sized to your own risk tolerance.

This article is for informational purposes only and does not constitute financial or investment advice. Tax rules referenced reflect the Korean tax code as of 2026. Individual circumstances vary — consult a licensed financial advisor before making any investment or contribution decisions.

Leave a Reply