Fixed Rates Keep Rising — So Why Is Everyone Choosing Variable?

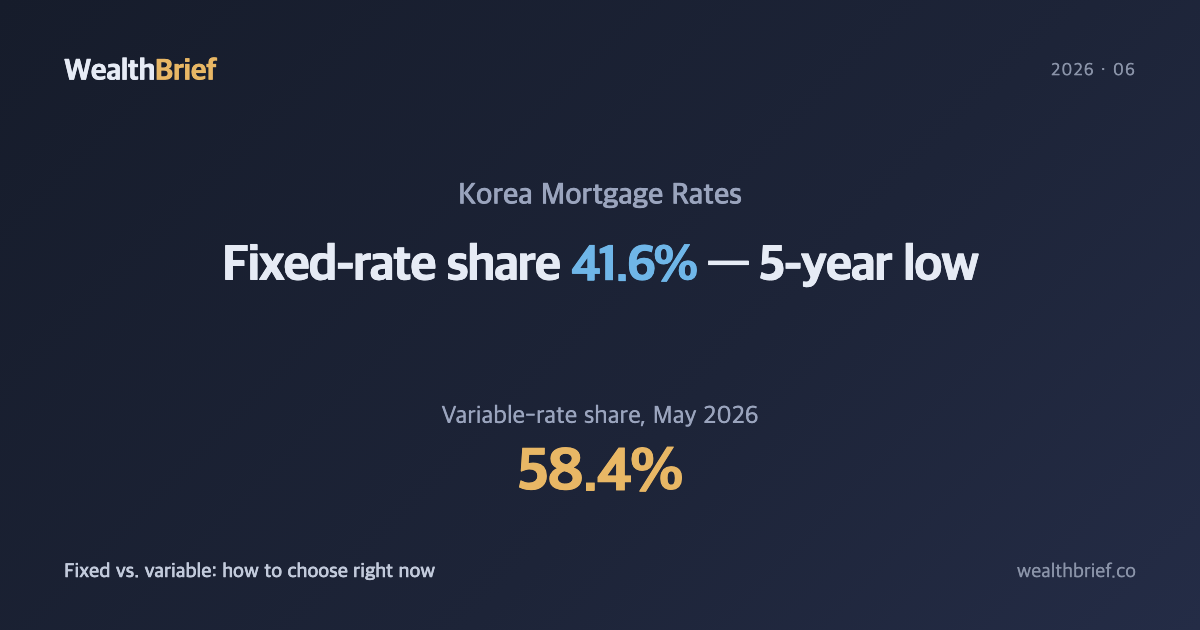

In May 2026, nearly six out of ten new mortgage borrowers in South Korea chose a variable-rate loan. That’s according to data compiled by the Bank of Korea and reported by Yonhap News on June 26, 2026. The share of fixed-rate mortgages fell to 41.6% — the lowest in roughly 59 months, or about five years — while the average interest rate on new home loans ticked up to 4.32% after a month of decline. In just two months, the fixed-rate share dropped nearly 19 to 20 percentage points.

The reason borrowers are fleeing fixed rates isn’t hard to find: fixed-rate products — tied to bank bond yields — have risen for eight consecutive months. When the spread between fixed and variable rates widens, the monthly payment difference becomes real money. “Start variable, refinance to fixed later” sounds reasonable. Whether it turns out that way depends on what happens to interest rates next — and nobody knows that for sure.

The Numbers Behind the Shift

| Metric | March 2026 | May 2026 | Change |

|---|---|---|---|

| Fixed-rate share | ~60% | 41.6% | ▼ ~19 ppts |

| Variable-rate share | ~40% | 58.4% | ▲ ~19 ppts |

| Avg. new mortgage rate | ~4.20% | 4.32% | ▲ 0.12 ppts |

Source: Bank of Korea, Yonhap Infomax, Yonhap News, as reported June 26, 2026. March figures are comparison values cited in news coverage.

What Is COFIX — and Why It Matters

COFIX (Cost of Funds Index) is the benchmark that determines variable mortgage rates in South Korea. It reflects the average cost at which major banks fund themselves — through deposits, bonds, and similar instruments. When COFIX falls, variable-rate payments ease. When it rises, they go up, typically with a six-month lag baked into most loan contracts.

Recently, COFIX has eased slightly, which is one reason variable-rate loans look comparatively cheap right now. But COFIX isn’t fixed. During the 2022 rate-hiking cycle, it climbed nearly two percentage points within a year. Variable-rate borrowers absorbed every bit of that increase, month by month.

Three Layers of Risk in Variable-Rate Loans

- Rate reset cycles: Most variable loans reprice every six months based on COFIX. If rates are higher at the next reset, your monthly payment goes up — automatically, without warning.

- Stress DSR: Stress DSR (Debt Service Ratio) is a regulatory stress test that adds a buffer rate on top of actual variable rates when calculating a borrower’s repayment capacity. Variable-rate borrowers are effectively stress-tested at a higher rate, which can reduce their maximum loan size compared to fixed-rate applicants under the same income.

- Refinancing costs: Switching from variable to fixed mid-loan triggers early repayment fees. The “refinance later” option is real — but it isn’t free.

To be fair, the counterargument has merit. If the Bank of Korea cuts its benchmark rate — say, in response to slowing growth or a softer property market — variable rates could end up meaningfully cheaper over the loan’s life. That’s a plausible scenario. It’s also not guaranteed. The honest answer is that the outcome depends on a policy path no one can call with certainty.

How to Think About the Choice

Trying to predict which rate type will cost less over a ten- or twenty-year mortgage is a losing game. A more practical frame: how much rate volatility can your household cash flow actually absorb?

- If your monthly principal and interest payment already exceeds 40% of take-home income, work out what happens if your rate rises by 1 percentage point. If the math breaks your budget, the variable-rate downside isn’t theoretical — it’s a real exposure.

- If you have a firm plan to sell or pay off the loan within three to five years, then short-term rate forecasting matters more. Over shorter horizons, variable can win even in a rising-rate environment if the initial savings outpace the eventual increase.

- If your horizon is ten years or more and you value predictability, fixed-rate premiums function more like insurance than waste.

The average rates published in news reports are system-wide averages. The rate you’ll actually be offered depends on your credit score, LTV ratio, loan size, and the specific bank’s current pricing. Korea’s Financial Supervisory Service operates a comparison tool (“금융상품 한눈에”) where you can see actual rates across lenders. That step is worth taking before any decision.

What to Watch in the Second Half of 2026

COFIX is recalculated monthly. The next several readings — alongside Bank of Korea Monetary Policy Committee decisions scheduled for the second half of 2026 — will tell a clearer story about where variable rates are headed. There’s also a regulatory wildcard: if household debt growth picks up again, financial authorities could tighten DSR thresholds or adjust stress-rate assumptions, which directly affects how much borrowers can take on.

If you already have a variable-rate loan, note your next repricing date. That’s when your rate gets recalculated against the prevailing COFIX. Having a few months’ lead time to consider refinancing — rather than reacting after the fact — is the most concrete thing you can do right now.

This article is for informational purposes only and does not constitute financial or investment advice. Individual circumstances vary; consult a qualified financial professional before making borrowing decisions. Data cited reflects reporting as of June 26–27, 2026.

Leave a Reply