Six Months Ago, Everyone Expected Rate Cuts. Now Wall Street Says “No.”

At the start of 2026, the script seemed clear: the Federal Reserve would cut rates in the second half of the year, the dollar would ease, and Korean mortgage rates would drift lower. Markets positioned accordingly. Then June happened.

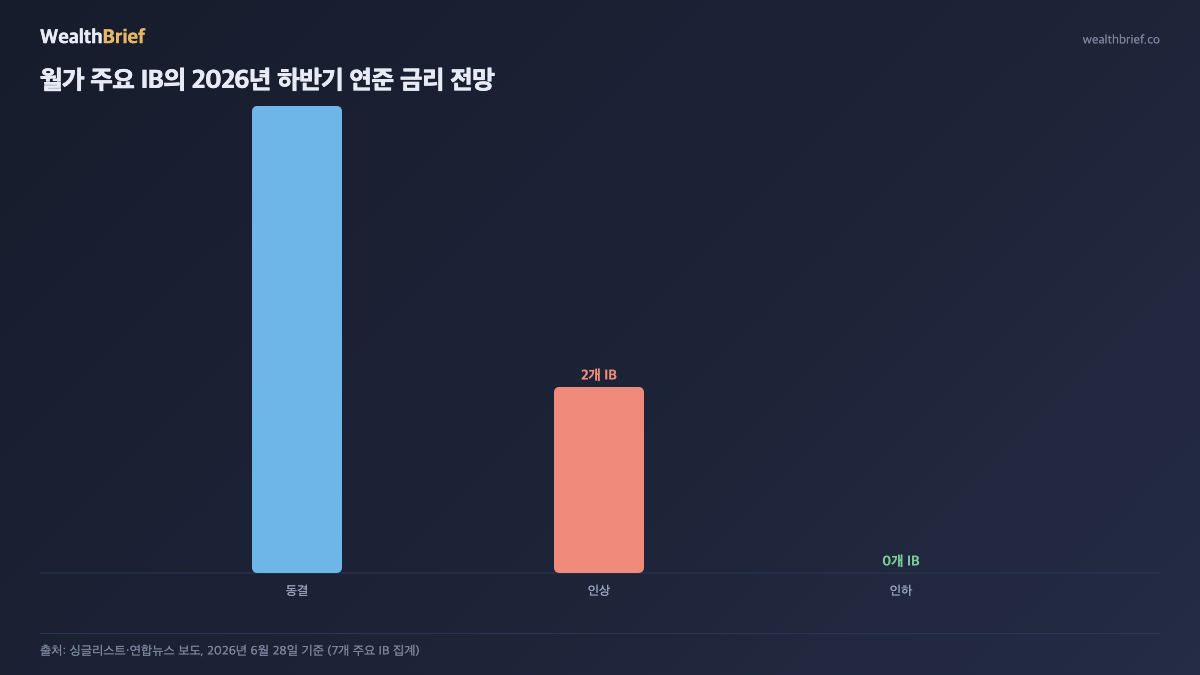

Between June 28 and 30, 2026, major Korean and international financial media reported a striking shift in Wall Street sentiment: among seven major investment banks surveyed, most now expect the Fed to hold rates through year-end — and Bank of America (BoA) and Deutsche Bank are forecasting outright hikes (Singlelist, June 28, 2026).

BoA’s call is the sharpest: three rate hikes starting September 2026 (v.daum.net, Blockchain Today, June 23, 2026). The Bank of Korea’s New York office confirmed that the majority of major IBs now view the Fed’s rate-cut cycle as over, with the base case shifting to a hold or tightening bias (MBC News, YTN, late June 2026).

Why the Reversal — and Why It Matters for Korean Households

The pivot isn’t hard to explain. US inflation — specifically the Fed’s preferred gauge, the PCE (Personal Consumption Expenditures) deflator — has stayed stubbornly above the 2% target. Add in pre-midterm fiscal stimulus, lingering tariff pass-through effects, and a Fed internally wary of repeating the 1980s mistake (easing too early, only to face an inflation comeback), and the case for cuts has evaporated.

For Korean households, the consequences flow through three channels:

- Exchange rate: A Fed that holds or hikes keeps the dollar strong. The won closed at ₩1,551.20 per dollar on July 1, 2026 (Yonhap Infomax, July 1, 2026) — levels not seen in 17 years. Sustained dollar strength keeps the pressure on.

- Bank of Korea pressure: A weaker won forces the BOK’s hand. The BOK has already signaled a hike possibility in internal documents. If the Fed moves toward tightening, the BOK’s rationale for hiking strengthens further.

- Mortgage rates: If the BOK raises its base rate, analysts warn that Korean fixed mortgage rates could breach 8% (Digital Times, June 10, 2026). The upper band on fixed-rate home loans already sits at approximately 7.33%.

Three Scenarios, One Table

| Scenario | Fed Path | BOK Likely Response | Korean Mortgage Rate Direction |

|---|---|---|---|

| ① Prolonged hold | No change through Dec 2026 | Possible hike on FX pressure | Stays in 7% range or nudges higher |

| ② BoA scenario | 3 hikes from September | Strong push to hike | Potential break above 8% |

| ③ Late pivot | 1 cut in Q4 2026 | Hiking pressure eases | Possible return toward high 6% |

Scenario ③ is currently the minority view. Rate futures markets have dramatically pared back the probability of a 2026 cut — a broad reflection of IB consensus, not just one firm’s call.

Three Things to Check Right Now If You Have a Mortgage

The macro shift above isn’t abstract if you carry Korean home loan debt. Here’s where to start:

- Fixed or variable? Variable-rate loans reprice when the BOK moves. Fixed-rate loans are insulated — until maturity. If you locked in a five-year fixed rate in 2021, your repricing date arrives this year.

- Repricing schedule: Most Korean variable mortgages reset every 6 or 12 months, tied to the COFIX index (Cost of Funds Index — the benchmark banks use to price loans). Find your next reset date.

- Buffer calculation: On a ₩300 million 30-year loan, a rate move from 7% to 8% adds roughly ₩250,000 per month in interest. Model your own numbers now, not after the BOK decision.

The Counter-Case

BoA’s “three hikes” call is an outlier, not a consensus. Fed Chair Powell has publicly maintained that current policy is “sufficiently restrictive” — he hasn’t signaled a turn toward hikes. Some economists argue that if US consumer spending weakens and employment cools through Q3, the Fed could slip in one cut by year-end, taking pressure off the won and Korean rates.

That remains a possibility. But building a borrowing or property strategy around the assumption of imminent Fed cuts — when Wall Street’s majority view has flipped to “hold or hike” — carries meaningful downside risk.

Bottom Line

Six months ago, the question was “when will rates come down?” Today it’s “what if they go higher?” Wall Street’s consensus shift, combined with a 17-year low for the won and the BOK’s documented hike bias, makes the second half of 2026 a period where Korean borrowers should stress-test their finances against higher rates — not plan around lower ones.

This article is for informational purposes only and does not constitute financial or investment advice. For decisions related to mortgages or interest rate exposure, consult a qualified financial adviser or your lending institution.

Leave a Reply