Why the Airport Shows ₩1,621 When the News Says ₩1,553

Korea’s won closed at around 1,537 per dollar on July 4, 2026. Walk up to a currency exchange counter at Incheon International Airport and you’ll pay closer to 1,620 won for that same dollar. The gap — over 80 won — isn’t a mistake or a rip-off. It’s a spread, and understanding how it works is the fastest way to stop handing money over for nothing.

The rate on the news is the interbank reference rate (매매기준율), the wholesale price at which banks trade large amounts of currency with each other. When you exchange cash at a counter, the bank adds a spread — its margin and handling cost. For U.S. dollars, the typical spreads in Korea look like this:

- Wire transfer / foreign currency deposit: ~1% spread above reference rate.

- Cash exchange at a city bank branch: ~1.5–1.75% spread.

- Airport or hotel counter: 3–4% spread (higher rent, higher cost, higher price).

- Travel card (paying by card overseas): 0–1% — closest to the reference rate.

With a reference rate of 1,537 won, that means the cash rate at a city bank branch is around 1,563 won, and at an airport counter it can reach 1,598–1,621 won. A report in early July 2026 noted airport exchange counters had already crossed 1,621 won per dollar (Nate, July 2, 2026).

Why the Spread Hurts More When Rates Are High

Percentage spreads look the same whether the rate is 1,200 or 1,550. But in absolute terms the damage grows. At 1,200 won, a 1.75% spread costs you 21 won per dollar. At 1,550 won, the same rate costs 27 won per dollar.

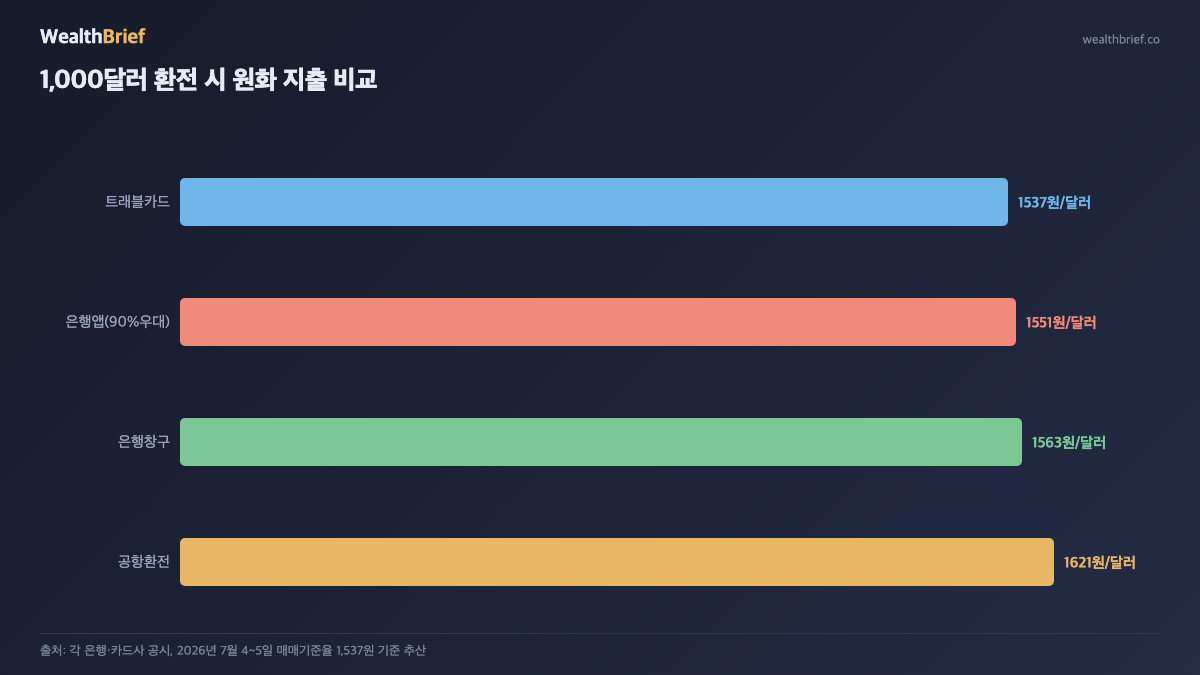

Exchanging 1,000 USD (roughly ₩1.55 million) under current rates:

| Exchange Method | Approx. Rate Applied | Total Cost (KRW) | Extra vs. Reference Rate |

|---|---|---|---|

| Bank app (90% discount on spread) | ~1,551 | 1,551,000 | +₩14,000 |

| Bank branch counter (no discount) | ~1,563 | 1,563,000 | +₩26,000 |

| Airport counter | ~1,600–1,621 | 1,600,000–1,621,000 | +₩63,000–84,000 |

| Travel card (overseas spending) | Reference rate +0–1% | ~1,537,000–1,552,000 | ~₩0–15,000 |

Estimates based on the reference rate of approximately 1,537 won as of July 4–5, 2026. Actual rates vary by bank, timing, and discount tier.

The ₩9 Trillion Travel Card Market

Travelwallet, one of Korea’s biggest fintech travel cards, reported annual overseas spending of approximately ₩9 trillion as of mid-2026 (Chosunbiz, June 30, 2026). Add in similar products from Toss, Kakao, Shinhan, and Hana and the category dwarfs that figure. The reason is straightforward: travel cards apply an exchange rate close to the interbank reference rate with minimal fees, directly at the point of sale.

The one catch: the rate applied is the rate at the time of the transaction. If you expect the won to weaken further, loading foreign currency in advance locks in today’s rate. If you expect recovery, paying at the moment of purchase could work in your favor. Neither bet comes with a guarantee.

The July 6 Change: 24-Hour FX Trading Starts Tomorrow

Starting July 6, 2026, won-dollar trading extends to 2 a.m. Korean time — up from the previous 3:30 p.m. close. Korea’s Ministry of Economy and Finance described it as a step toward full internationalization of the won (Yonhap, July 3, 2026). An analysis by NewsSpace (July 2, 2026) offered a more nuanced take: morning gaps in the exchange rate will shrink, but overnight volatility may increase as global events now move the rate in real time.

Three things change for everyday users:

- No more single daily close: The 3:30 p.m. “closing rate” loses its significance. The rate moves through the night.

- Overnight U.S. data moves the rate immediately: Fed remarks, payroll numbers, CPI prints — these used to create a gap at the Korean open the next morning. From July 6, they move the rate as they happen.

- Bank app exchange hours are changing: Some banks are extending app-based exchange to night hours. Check your own bank’s schedule before counting on a midnight currency transfer.

A Practical Checklist for High-Rate Times

This is general information, not personalized financial advice. That said, a few principles tend to reduce unnecessary losses:

- Airport exchange is a last resort: The spread can be two to three times higher than a bank app. If you must use an airport counter, look for the exchange discount coupons many banks issue in advance.

- Bank app with a spread discount: Most Korean banks offer a 90% discount on the spread through their apps. That typically saves ₩10–15 per dollar versus walking up to the counter.

- Travel card for overseas spending: Zero or near-zero spread on most current products. For routine foreign spending, this is the most cost-efficient channel available.

- Dollar deposits: Buying dollars now into a foreign currency deposit gains if the won weakens further, loses if the won recovers. Either outcome is plausible — the second quarter 2026 average hit levels not seen in 28 years (v.daum.net), but institutional forecasts range from a return to the ₩1,400s all the way to a break above ₩1,600.

- Avoid the double-spread trap: Exchanging cash both ways — won to dollars and back — means you pay the spread twice. Unless you need physical notes for a specific reason, spending with a card overseas sidesteps this entirely.

The Most Common Mistake Right Now

Waiting for the rate to drop before exchanging, then ending up at the airport counter anyway. The second quarter 2026 won/dollar average marked a 28-year high. Plenty of travelers waited, the rate didn’t fall, and they paid airport spreads on top. Exchange rate direction is genuinely hard to call — professional forecasts diverge widely. What’s certain is the spread. Minimizing the spread is the one variable squarely within your control.

This article is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any financial product. Individual circumstances vary. Consult a qualified financial professional before making significant currency or investment decisions.

Leave a Reply