It Wasn’t Gangnam — Dongtan Just Posted Korea’s Highest Monthly Apartment Price Gain

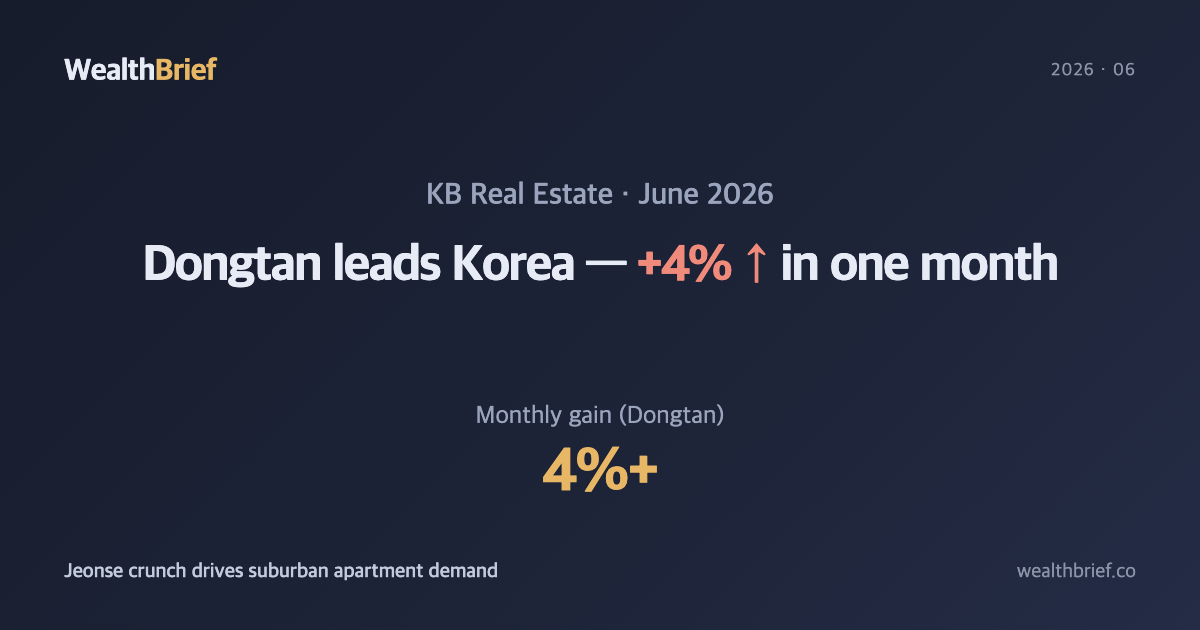

For most of the past decade, when you asked which part of Korea was seeing the fastest home price increases, the answer was usually Gangnam, Seocho, or one of Seoul’s elite southern districts. June 2026 changed that story. According to KB Real Estate’s latest housing price index, Dongtan (Hwaseong) recorded the highest monthly apartment price gain in the country — surpassing 4% in a single month (KB Real Estate, June 2026). Gangnam and Seocho weren’t even close.

This isn’t just a curiosity. The structure driving that number reveals something broader happening across the Seoul metropolitan area.

When Renting Costs as Much as Buying — Jeonse at Eight Figures

To understand what’s pushing buyers out of Seoul and into areas like Dongtan, start with the rental market. KB Real Estate’s June 2026 report noted that you now need a minimum of ₩800 million in jeonse deposit (Korea’s lump-sum rental system) just to live in the Gangnam district. The jeonse appreciation rate for Seoul hit its highest point of the year in June.

Jeonse works like this: a tenant hands over a large lump-sum deposit — often equal to 60–80% of the purchase price — lives rent-free, and gets the full deposit back at lease end. When jeonse prices rise to ₩800 million in Gangnam, the calculus shifts. For a similar capital outlay, a buyer could instead purchase a mid-sized apartment in Dongtan or neighboring Gwangmyeong, Seongnam, or Hanam — especially now that GTX-A makes Dongtan about 20 minutes from Suseo Station in southern Seoul.

How Much Have Prices Actually Moved?

| Segment | Price Change | Source / Reference Date |

|---|---|---|

| Seoul apartments (12-month) | +12% | Yonhap Infomax, June 27, 2026 |

| National apartments (12-month) | +4.0% | Yonhap Infomax, June 27, 2026 |

| Dongtan (Hwaseong) – monthly | +4%+ in June alone | KB Real Estate, June 2026 |

| Gangnam jeonse floor (approx.) | ₩800M minimum | KB Real Estate, June 2026 |

| Incheon buy/sell ratio | Demand exceeded supply for first time in 4 years 7 months | Jungbu Ilbo, June 28, 2026 |

Seoul’s 12% over twelve months versus the national 4% confirms a familiar pattern: concentration at the top. But Dongtan matching the national annual gain in a single month is a different signal — it suggests catch-up momentum, not just the usual Seoul premium.

Why Dongtan? Three Structural Reasons

Supply, transit, and relative value are converging here at the same time.

First, GTX-A. The new express line connecting Dongtan to Suseo (southern Seoul) cuts commute times significantly. Buyers who couldn’t justify Dongtan’s distance from Seoul before are now reconsidering. Second, Dongtan 2 New Town offers large-scale apartment complexes built in the past decade — newer stock than much of Seoul’s mid-ring suburbs. Third, prices are still meaningfully lower than comparable Seoul units, even after this year’s appreciation.

That said, some cautions deserve honest attention:

- Ongoing supply in Dongtan 2: The new town still has remaining construction phases. If incoming supply exceeds absorption, a short-term price correction is possible — this has happened in other new town phases historically.

- Gap investment exposure: In Korean real estate, gap investment (갭투자) means purchasing a unit by layering your own capital on top of an existing jeonse deposit — using the tenant’s deposit as leverage. When jeonse prices rise, the gap narrows and this looks attractive. But if jeonse prices fall, owners face a situation called yeokjeonse (역전세) — where the jeonse value exceeds the sale price — potentially forcing them to return deposits they don’t have.

- DSR and LTV constraints remain: DSR (Debt Service Ratio) caps total annual loan repayments at 40% of gross income for first-tier banks. LTV (Loan-to-Value) limits how much a buyer can borrow relative to the property’s appraised value. Even in a rising market, these rules constrain actual purchasing power — price gains don’t automatically create matching borrowing capacity.

The Wider Picture: Debt Is Rising Too

A separate data point from the same week deserves attention. Per-capita bank loans for Korean borrowers in their 30s exceeded ₩100 million for the first time ever; loans to borrowers in their 40s have risen for three straight years (Maeil Business, June 28, 2026). Home prices rising alongside household debt loads is a combination that historically warrants attention — whether it leads to stress depends heavily on where rates go and how regulators respond.

The government has shown it will intervene when credit growth gets too fast. Stress DSR testing (applying a hypothetical higher rate to assess repayment capacity under stress scenarios) is already in the regulatory toolkit, and further tightening or loosening of LTV bands remains a live policy option.

What This Means If You’re Deciding Now

If you’re weighing a purchase decision in the outer Seoul metro area, a few reality checks are worth running before the headlines drive a decision:

- Run the DSR calculation first. Your borrowing ceiling is set by income, not by the asking price.

- Verify local supply pipeline. A 4% monthly gain is striking, but understanding what’s being built and when it delivers is just as important.

- Price-in the jeonse scenario. If you’re buying with an existing jeonse tenant or plan to place one, model what happens if jeonse prices soften 10–15% from here.

The structural logic — expensive Seoul jeonse pushing buyers toward suburban GTX-connected towns — is coherent and appears to be actively playing out in the data. Whether it has another month or another year of runway is a harder call, and one nobody can make with confidence right now.

This article is for informational purposes only and does not constitute investment, financial, or real estate advice. All figures cited reflect media reports and should be verified against official sources before being used in any decision-making context.

Leave a Reply