The Bank of Korea Just Put “Rate Hike” in Writing

On June 24, 2026, the Bank of Korea (BOK) released its semi-annual Financial Stability Report. Buried inside was a sentence that made markets sit up: “It is necessary to raise the policy rate at an appropriate time to curb the accumulation of financial imbalances.” For a central bank that typically hedges its language, spelling out a rate hike this explicitly is a meaningful signal — not a hint, not a possibility, a stated direction.

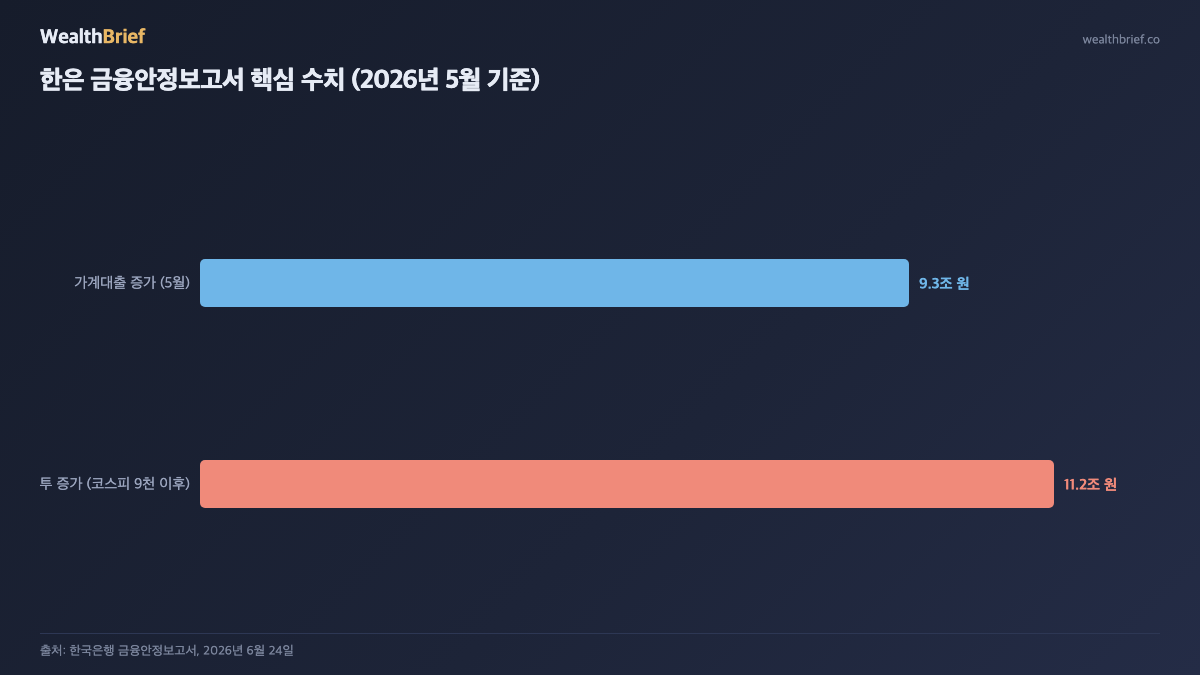

The report identified two pressure points driving the warning. First: housing prices are climbing again. Second: leveraged stock investing — what Korean retail investors colloquially call bittoo (debt-financed speculation) — has surged. In May alone, household debt grew by ₩9.3 trillion (source: BOK Financial Stability Report, June 24, 2026). Leverage in equities — through margin accounts, uncovered trades, and stock-backed loans — rose by ₩11.2 trillion since the KOSPI broke 9,000 (source: BOK Financial Stability Report, June 24, 2026). Total household credit now stands at ₩1,993 trillion, a whisker away from the symbolic ₩2,000 trillion mark (source: Bank of Korea, June 2026). The BOK’s Financial Stability Index (FSI) — a composite gauge of systemic stress, where readings above the long-term average signal elevated risk — has entered what it classifies as the “caution” zone.

So Why Can’t the BOK Just Hike Now? The Dilemma

Declaring an intention and pulling the trigger are different things. Here’s the bind the BOK is in:

| If it raises rates | If it holds |

|---|---|

| Mortgage and credit line rates rise further → household interest burden increases | Housing prices continue climbing → debt grows further |

| Margin calls hit leveraged investors → potential equity selloff | KRW/USD exchange rate stays entrenched near 1,540–1,550 |

| Distress deepens in construction and vulnerable sectors — the BOK’s own “weak links” | Leveraged investment continues to expand → systemic risk grows |

The BOK’s report specifically named construction and other vulnerable industries as the “weak links” most exposed to a rate shock (source: Chosun Ilbo / Newspim, June 24, 2026). These sectors are already under pressure from unresolved project-financing (PF) defaults. A rate hike would hit them hardest and fastest.

On the other side: if the BOK does nothing, the won stays weak. On June 25, 2026, USD/KRW closed at 1,543.10 — still in the elevated range that has persisted for over three weeks (source: Yonhap News, June 25, 2026). A rate hike would help narrow the Korea-U.S. rate differential and provide at least some support to the currency.

The timing question — July or August meeting — is still open. Market consensus is leaning toward a hike in the second half of 2026, but the exact month depends on incoming data. No one should treat this as certain.

Three Things Borrowers Should Check Right Now

If Korea is moving into a rate hike cycle — even a gradual one — the structure of your debt matters more than the headline rate. Three practical checks:

- ① Find your rate reset date

Mixed-rate mortgages (혼합형 주담대) are fixed for an initial period — typically 3 to 5 years — then switch to variable. If your reset date falls in the second half of 2026, now is the moment to compare refinancing to a fixed product or switching lenders before rates move. - ② Tally up your variable-rate short-term debt

According to Maeil Business Newspaper (June 24, 2026), 37% of mortgage borrowers in Korea also carry personal credit loans. Credit lines and revolving facilities reprice quickly. Prime-credit borrowers are already seeing credit line rates above 5% annually (source: Newsis, June 2026). Variable-rate short-term debt is first in line when the policy rate moves up. - ③ Stress-test your leveraged positions

The BOK flagged ₩11.2 trillion in new equity leverage as a specific risk. If you’re using margin, uncovered credit, or stock-backed loans, calculate what a 0.25%p rate hike does to your monthly interest cost — and check how much buffer sits between your current portfolio value and any forced liquidation threshold.

₩1,993 Trillion and What It Means for You

Household debt at ₩1,993 trillion means that a 0.25 percentage point rise in the policy rate translates — across variable-rate loans — into billions of won in additional annual interest payments flowing from households to banks. That money comes directly out of consumption. The macro effect shows up as a drag on domestic demand; the personal effect shows up in your monthly bank statement.

The BOK report did note that the financial system should be able to absorb a rate increase without systemic shock. That’s a different claim from saying individual borrowers won’t feel it. The system may hold — your cashflow is a separate question.

Bond Markets Are Already Moving

You don’t have to wait for a policy rate announcement to see the effect. Korean government bond yields across all maturities are converging toward 4% (source: Aju Business Daily, June 23, 2026). When bond yields rise, banks’ funding costs follow, and lending rates follow those. The market is already repricing — ahead of any official move.

Waiting for the official hike announcement to act means responding after the signal, not before it.

The Bottom Line from This Report

- The direction is set: the BOK has put “rate hike” in its formal policy document. The question is when, not if.

- The two triggers: housing prices resuming their climb, and ₩11.2 trillion in new leveraged equity bets.

- Action items now: check rate reset dates, tally variable-rate short-term debt, stress-test leveraged investment positions.

- Bond markets are already moving toward 4%. Policy rate decisions lag market rates — don’t wait for the announcement.

Related

- Korea Leans Toward Hikes While the Fed Eases — What the 2026 Rate Decoupling Means for Your Money

- Korea’s Jeonse Loan Squeeze: Who Gets Hit by the Triple Crackdown

This article is for informational purposes only and does not constitute investment advice or a recommendation of any financial product. Individual borrowing and investment decisions should be made in consultation with a qualified financial professional.

Leave a Reply