What Changed at Midnight — July 1, 2026

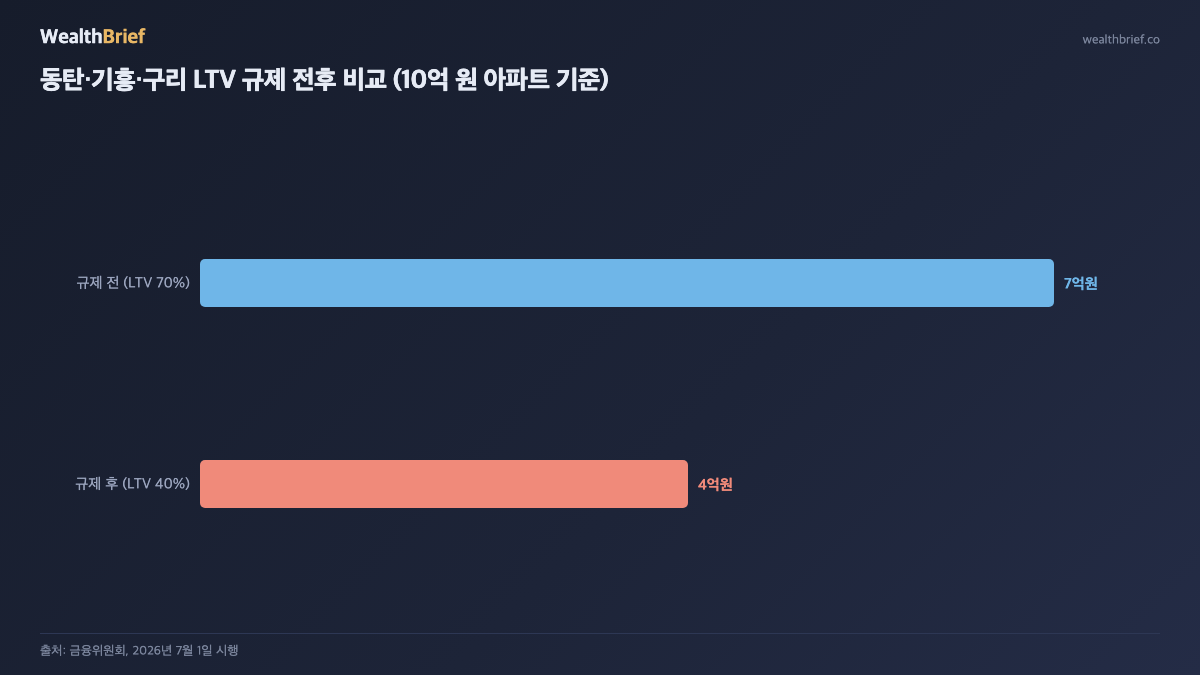

Three satellite cities outside Seoul — Hwaseong Dongtan, Yongin Giheung, and Guri — woke up on July 1, 2026, under a triple-layer of real estate controls. As of midnight, all three were designated Adjustment Target Zone, Overheating District, and Land Transaction Permit Zone simultaneously. The immediate effect: the loan-to-value (LTV) cap on mortgage lending dropped from 70% to 40% (Financial Services Commission, June 30, 2026).

That’s not a minor tweak. For a buyer looking at an apartment worth ₩1 billion (roughly $725,000 at current rates), the maximum borrowable amount just fell from ₩700 million to ₩400 million — a ₩300 million gap that has to come from somewhere else, namely the buyer’s own pocket.

Why These Three? The Semiconductor Money Trail

The three areas share a common thread: they’ve all been carried up by the semiconductor investment wave.

- Hwaseong Dongtan: Adjacent to Samsung Electronics’ Hwaseong and Giheung campuses. It briefly posted the highest monthly apartment price gains nationwide, with some data showing roughly 11% appreciation over a five-month window in early 2026 (Korea Real Estate Board weekly survey, May 2026).

- Yongin Giheung: Samsung Electronics’ primary campus. Employment demand from semiconductor expansion has been translating directly into housing demand.

- Guri: Benefited from GTX-B metro line expectations and proximity to northeast Seoul, generating sharp short-term appreciation.

Joongang Ilbo described the phenomenon as “semiconductor money flooding into Dongtan, Giheung, and Guri” (June 30, 2026). When an industrial boom inflates local housing prices faster than incomes can follow, the government’s instinct is to tighten credit — which is exactly what’s happening here.

The Numbers: How Borrowing Power Has Shrunk

LTV sets the ceiling on how much you can borrow against a property’s appraised value. Here’s what the shift looks like at different price points:

| Apartment Value | Max Loan (LTV 70%) | Max Loan (LTV 40%) | Reduction |

|---|---|---|---|

| ₩1 billion | ₩700 million | ₩400 million | –₩300 million |

| ₩800 million | ₩560 million | ₩320 million | –₩240 million |

| ₩600 million | ₩420 million | ₩240 million | –₩180 million |

The mortgage crackdown doesn’t stand alone. Jeonse (Korea’s lump-sum deposit rental system) loans are simultaneously restricted for non-resident homeowners. The state-backed guarantee ratio from HUG and SGI has also been tightened. For leveraged buyers who relied on jeonse tenants to cover a large portion of the purchase price — the so-called “gap investment” strategy — this triple restriction effectively closes the playbook.

What the Triple Designation Actually Means

Each layer of regulation brings its own restrictions:

- Adjustment Target Zone: Heavy capital gains tax surcharges for multi-home sellers; mortgage LTV capped at 50%.

- Overheating District: LTV further tightened to 40%; restrictions on transferring reconstruction cooperative membership.

- Land Transaction Permit Zone: Transactions above certain size thresholds require district office approval. Buyers must demonstrate genuine intent to occupy — which functionally bans gap investment.

Yonhap News called it a “gap investment blockade” (June 30, 2026). That’s the right framing. The combination of LTV 40%, jeonse loan restrictions, and occupancy requirements means that buying purely as an investment — without actually moving in — is now extremely difficult without substantial cash reserves.

Will It Work? The Honest Answer

The government says price momentum “will ease” (Financial Services Commission, June 30, 2026). Some reports noted sellers pulling listings or trimming asking prices immediately after the announcement.

The skeptics have a point too. Women’s Economy News raised the concern that suppressing jeonse loans while restricting supply could worsen the jeonse shortage rather than fix the broader problem (June 30, 2026). If mortgage buyers can’t borrow enough and jeonse tenants can’t secure loans either, housing market demand doesn’t simply vanish — it shifts and concentrates elsewhere.

There’s a precedent to consider. After the June 27, 2025 measures, prices stabilized briefly before resuming an upward trend. Whether this round holds depends heavily on new supply — apartments scheduled to come online in the Dongtan, Giheung, and Guri pipeline over the next 12–24 months.

What It Means Depending on Where You Stand

If you’ve already signed a contract: Whether your loan is processed under the old 70% or new 40% cap depends on when the loan application is formally submitted — not when you signed the sales contract. Verify immediately with your bank, today.

If you’re considering a purchase: The affordable price ceiling has fallen sharply. A buyer with ₩400 million in cash could approach properties worth up to roughly ₩1.33 billion under the old 70% LTV (₩400m ÷ 0.3). Under 40% LTV, the same buyer is looking at ₩667 million (₩400m ÷ 0.6). That’s a fundamentally different market segment.

If you’re a jeonse tenant: Non-resident landlords losing access to jeonse loans at renewal may pressure tenants to either reduce the deposit or convert to monthly rent. Check your contract end date and whether you have remaining renewal rights under the Tenant Protection Act.

Bottom Line

As of today, buying an apartment in Dongtan, Giheung, or Guri requires ₩300 million more in cash for a ₩1 billion property than it did yesterday. The government is betting that cutting credit access cools prices; the risk is that it simultaneously inflates the jeonse market and squeezes genuine owner-occupiers. Both things can be true at once — and often are.

This article is for informational purposes only and does not constitute investment or financial advice. Loan conditions vary by lender, application timing, and individual circumstances. Consult a licensed financial professional for guidance specific to your situation.

Leave a Reply