Sixty percent of Americans say they’re uncomfortable with their level of emergency savings — and 31% describe themselves as “very uncomfortable,” according to Bankrate’s 2026 Emergency Savings Report (February 2026). Separate research from U.S. News found that 43% of adults couldn’t cover a $1,000 surprise expense without borrowing. That’s the baseline: a lot of people know they’re exposed, but most aren’t sure how exposed, or what to do about it.

The standard advice — “save three to six months of expenses” — is fine as a starting point. The problem is that it papers over a lot of variation. A tenured federal employee and a freelance graphic designer face completely different income risk. And with CPI up 4.2% year-over-year through May 2026 (per the U.S. Bureau of Labor Statistics), the dollar amount behind “six months of expenses” has quietly climbed even if your lifestyle hasn’t changed.

This guide walks through how to calculate a target that actually fits your situation, what counts as an “expense” in the first place, and where to stash the money so it earns something real.

The 3–6–9 Month Framework (and Which Applies to You)

The classic three-to-six-month rule was designed for dual-income households with stable W-2 jobs. If that’s you, it still holds. But life is messier than that, and the right target really does depend on your risk profile.

| Your situation | Recommended target | Why |

|---|---|---|

| Dual income, both W-2, stable industries | 3 months | Low re-employment risk; two income streams reduce single-point-of-failure |

| Single income, W-2, stable employer | 4–6 months | One income stream; job search takes longer than most people expect |

| Freelance, 1099, commission-based | 6–9 months | Income can vanish in a week; irregular cash flow means you need more buffer |

| Self-employed, business owner | 9–12 months | Business and personal expenses can blur; slow quarters compound quickly |

| Health conditions, sole provider for dependents | 6–12 months | Medical costs and caregiving can spike unpredictably |

Source: framework adapted from guidance published by the Consumer Financial Protection Bureau (CFPB) and NerdWallet (2026 edition). Always verify your specific situation with a financial planner.

What Actually Counts as a Month of “Expenses”?

This is where most people either over- or underestimate. The emergency fund is designed to cover the stretch of time between losing your income and finding new income — so you want to count the expenses you’d still have to pay even if you cancelled every discretionary spend.

Essential monthly expenses (include these):

- Rent or mortgage payment (including property tax escrow if applicable)

- Utilities: electricity, gas, water, internet

- Groceries (essential food — not restaurants or delivery)

- Minimum debt payments: student loans, car payment, credit cards

- Health insurance premiums (this stays even if you lose your job — COBRA or marketplace plans)

- Transportation: gas or transit passes to get to interviews or essential trips

- Childcare or eldercare you genuinely can’t cut

Leave out: subscriptions, gym memberships, dining out, vacations. In a real emergency you’d cut those. Don’t let them inflate your target — it just makes the goal feel impossible and you never start.

Worked Example: Calculating Your Target

Say you’re a single-income household in a medium-cost city, renting, with a W-2 job. Your essential monthly expenses break down like this:

| Expense | Monthly cost |

|---|---|

| Rent | $1,600 |

| Utilities + internet | $180 |

| Groceries | $400 |

| Health insurance (marketplace plan) | $280 |

| Car payment + insurance | $510 |

| Student loan minimum | $230 |

| Total essential | $3,200/month |

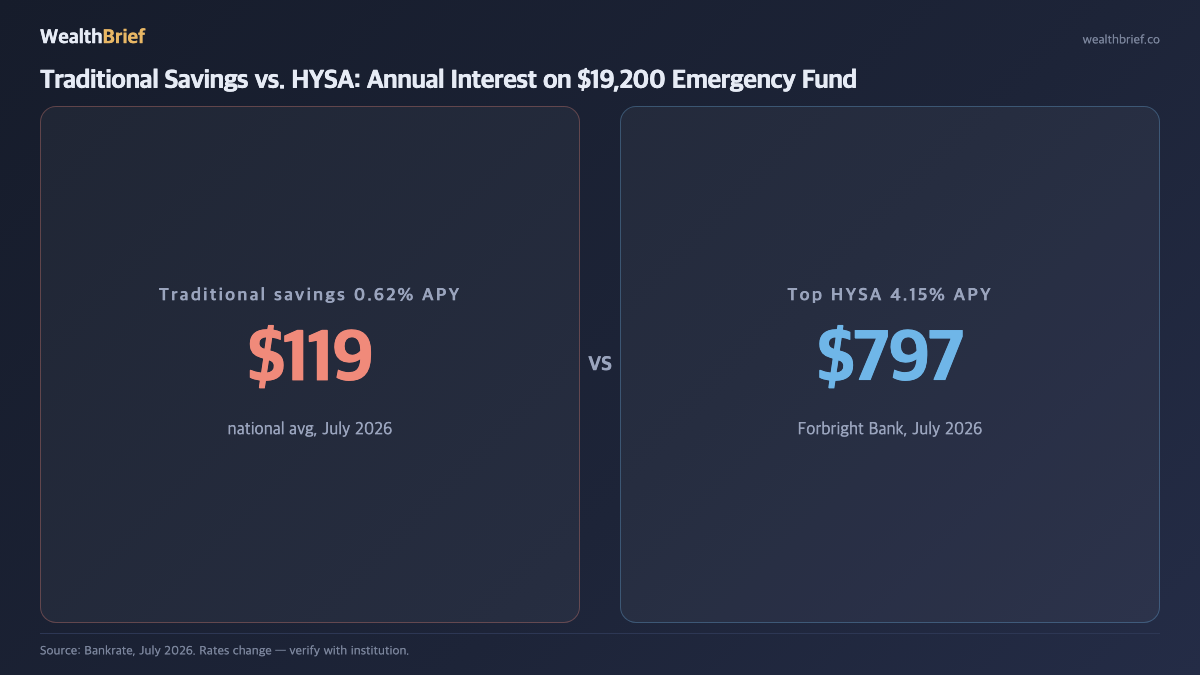

At a 6-month target: $3,200 × 6 = $19,200.

With CPI up 4.2% through May 2026 (BLS), if your rent and groceries have climbed even modestly, recalculate annually — the same “six months” now buys less than it did two years ago. A good rule: update your target number every January with your actual current expenses, not last year’s.

Where to Keep It (This Part Matters More Than You’d Think)

An emergency fund has two jobs: be safe and be accessible within one to two business days. That rules out most investment accounts. It doesn’t mean you have to settle for a 0.01% traditional savings account, either.

| Account type | Typical yield (July 2026) | FDIC/NCUA insured? | Access speed |

|---|---|---|---|

| Traditional bank savings | 0.01%–0.62% APY* | Yes (up to $250k) | Same/next day |

| High-yield savings (HYSA) | 4.15%–4.26% APY* | Yes (up to $250k) | 1–2 business days |

| Money market account | 3.5%–4.5% APY* | Yes (up to $250k) | Same day / check |

| Treasury bill ETF (e.g., SGOV, BIL) | ~4.5%–5.0%* | No (but backed by US govt) | T+1 to T+2 after sale |

| Stocks / equity ETFs | Variable — could be negative | No | T+1, but value uncertain |

*Rates as of July 2026. Sources: Bankrate (4.15% top HYSA, Forbright Bank), Investopedia (4.26% top HYSA), CNBC Select. National average traditional savings: 0.62% APY (Bankrate, July 2026). Rates change frequently — verify directly with the institution.

The practical winner for most people is a high-yield savings account. Top rates as of July 2026 are running 4.15%–4.26% APY, FDIC-insured up to $250,000. On a $19,200 emergency fund, the gap between 0.62% and 4.15% is roughly $681 a year in extra interest — free money for doing nothing except moving the account.

One caveat on T-bill ETFs: they’re fine for the bulk of a larger fund, but if you need the cash on a Saturday morning because your boiler just died, you need to sell first and wait for settlement. Keep at least one month’s expenses in a liquid savings or money market account for true immediate access.

Building It: A 4-Step Plan That Actually Sticks

- Set your number first. Use the worked example above with your own figures. Write it down. A vague goal of “save more” fails; a specific target of “$14,400 by March 2027” doesn’t.

- Open a dedicated account, separate from your checking. Keeping emergency money in the same account you spend from is a proven way to spend it. A separate HYSA at a different institution adds one transfer day of friction — usually enough to prevent impulse withdrawals.

- Automate a fixed transfer on payday. Even $50 biweekly is $1,300 a year. Increase it by $25 every quarter without re-examining the budget. Small, invisible increments compound without triggering lifestyle resistance.

- Define what “emergency” means before one hits. Car repair: yes. Flight home for a wedding: probably not. Medical co-pay you didn’t plan for: yes. New phone because yours feels old: no. Writing down your own definition prevents the fund from slowly evaporating on quasi-emergencies.

One More Thing: Inflation-Adjusting Your Target

The number that felt adequate in 2023 may be 8–10% too small by the end of 2026. With CPI up 4.2% year-over-year through May 2026 (BLS), every year you skip this step you’re quietly underfunded. The fix is simple: every January, re-run the “essential monthly expenses” calculation with actual current bills, and top up if needed. Think of it like rebalancing a portfolio — once a year, ten minutes, done.

In 3 Lines

- The right emergency fund is 3–9 months of essential expenses depending on your income stability — not a flat rule that fits everyone.

- With top HYSA rates at 4.15–4.26% APY (FDIC-insured, July 2026 per Bankrate and Investopedia), there’s no reason to let your emergency fund sit earning 0.62% in a traditional account.

- Recalculate your target annually — with CPI up 4.2% through May 2026 (BLS), last year’s number buys fewer months of runway than you think.

For information only, not financial advice. Rules, rates, and limits change — confirm current HYSA rates with the institution directly, and FDIC insurance details at FDIC.gov. For personalized guidance, consult a qualified financial advisor or visit CFPB.gov for free resources.

Leave a Reply