If You’re Holding Korean Semiconductor Stocks Right Now

In the past week, warning signals have been stacking up in the Korean equity market: Goldman Sachs flagged froth in the semiconductor sector, investor deposit balances hit a five-month low, and the Bank of Korea is widely expected to hike rates this week. Any one of these in isolation might be noise. Three pointing the same direction is worth checking.

This article outlines three variables that semiconductor investors in the KOSPI should verify this week. This is not investment advice. It presents facts, reasoning, and counterarguments — the conclusion is yours to draw.

1. What Goldman Sachs Actually Said

On July 8, 2026, HankyungMagazine reported in detail on Goldman Sachs’s warning about the semiconductor sector. The core argument had two parts: AI-driven earnings surprises are approaching their peak, and positioning in semiconductors has become too concentrated.

Goldman also recommended broadening AI exposure across hyperscalers more generally, rather than concentrating bets on a handful of chip names (Joongang Ilbo, June 26, 2026). The implication is that the current dynamic — where AI gains are disproportionately captured by Nvidia, SK Hynix, and Samsung Electronics — may not be sustainable.

Domestically, a parallel concern has emerged. According to NewsSpace (July 1, 2026), Samsung Electronics and SK Hynix together now account for close to 60% of KOSPI market cap, potentially triggering automatic rebalancing by passive funds that have internal concentration limits.

The counterargument from within the industry is clear: “Peak-out is at least two years away.” Memory chipmakers have been signing multi-year supply contracts with large customers, and analysts at Edaily (July 8, 2026) noted that DRAM spot prices aren’t declining — the rate of increase has simply slowed. Goldman’s warning may be a call for trimming, not an all-clear to exit.

2. The Arbiter of the Peak-Out Debate: Big Tech Earnings

Peak-out refers to an industry cycle turning from expansion to contraction. It’s currently the most contested debate in the global semiconductor market.

According to Newsis (July 11, 2026), Korea’s memory chipmakers are closely watching Big Tech earnings due at the end of this month. Amazon, Microsoft, Alphabet, and Meta will all report within days of each other, and their guidance on data center capital expenditure will directly shape demand forecasts for HBM (High Bandwidth Memory) and DDR5.

Bloter (July 8, 2026) put it plainly: “The answer to the peak-out question lies in Big Tech’s report cards.” Until those numbers land, both sides of the argument are arguing without data. That window of uncertainty — from now until late July — is where volatility is likely to be highest.

MarketIn (July 8, 2026) also flagged a supply-side risk. Samsung, SK Hynix, and Micron are all expanding HBM capacity simultaneously. If demand comes in even slightly below expectations, the industry could tip into oversupply. This is not a base case, but it’s a tail risk worth holding in mind.

3. Dry Powder and Rate Hikes: The Liquidity Picture

Stock prices don’t move on earnings alone. How much money is sitting on the sidelines, and which direction rates are heading, matter just as much.

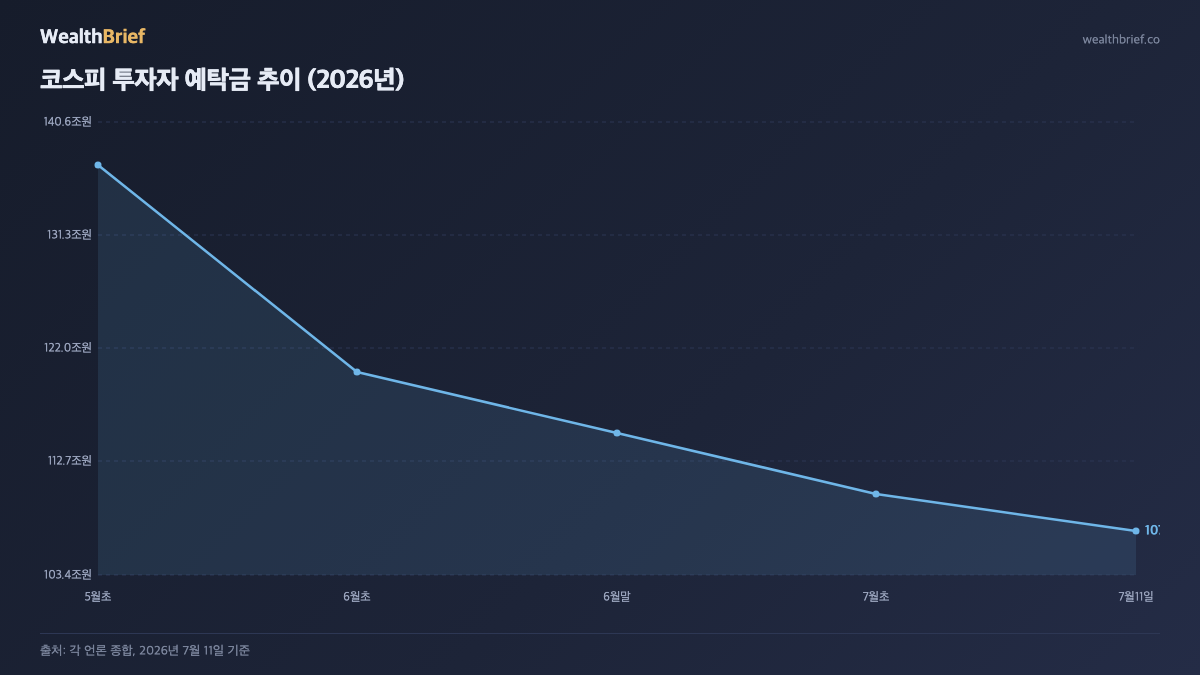

Investor deposit balances — cash sitting in brokerage accounts awaiting deployment — have dropped to approximately 107 trillion won, their lowest level in five months (Hankyung Magazine, Youth Daily, July 11, 2026). Aju Economy (July 10, 2026) reported that available market cash fell below 110 trillion won for the first time since February. At the KOSPI’s peak above 9,000, this figure stood near 137 trillion won — some 30 trillion won has left the sidelines in roughly two months.

Financial News (July 11, 2026) noted that retail investors, having absorbed about 12 trillion won of foreign selling, have themselves turned net sellers for three consecutive sessions. When retail buyers run dry and foreign selling continues, the bid-ask gap widens.

On rates, the most concrete catalyst is arriving this week. The Bank of Korea is widely expected to raise its benchmark interest rate for the first time in three and a half years at this week’s Monetary Policy Committee meeting, with some analysts calling the vote unanimous (Yonhap News, Edaily, July 10–11, 2026).

The benchmark rate is the rate at which the central bank lends to commercial banks; it serves as the reference point for most consumer and corporate borrowing costs. Rate hikes tend to compress valuations for high-growth, high-P/E sectors — and large-cap semiconductors carry exactly that kind of premium. Yonhap (July 11, 2026) cited analysts warning that the July hike may be followed by another in August or October, potentially marking the start of a new tightening cycle rather than a one-off adjustment.

Where Are Foreigners Going?

Chosunbiz (July 9, 2026) spotted an interesting pattern: foreign investors have been selling Samsung Electronics and SK Hynix while rotating into semiconductor materials, parts, and equipment (MPE) companies. This suggests sector-level conviction hasn’t collapsed — what’s changing is where within the sector they want to be positioned.

Newspim (July 7, 2026) reported that leveraged semiconductor ETFs amplified KOSPI’s 5% single-day drop on July 7. Leveraged products magnify both gains and losses; investors running levered exposure to Korean semis may want to review their position size in the current environment.

The Three Checkpoints

Here are the three things a KOSPI semiconductor investor should monitor this week:

- ① Bank of Korea rate decision (this week): The hike itself is largely priced in. What matters more is the tone of the governor’s statement — “one and done” versus signals of a sustained tightening cycle would produce very different market reactions.

- ② Foreign investor flow direction: The shift from large-cap chips to MPE stocks may be temporary, or it may be the beginning of a broader exit. Watch for sustained net selling over 10+ consecutive sessions as a threshold signal.

- ③ Big Tech earnings calendar (late July): Alphabet (July 29), Meta (July 30), Microsoft (July 30), Amazon (July 31). Data center capex guidance from these four companies will be the single most important data point in the peak-out debate.

If all three come in negative — a hawkish BOK, continued foreign outflows, and disappointing Big Tech data center numbers — near-term volatility in Korean semiconductor names could be significant. Conversely, a dovish BOK tone paired with strong AI capex guidance from hyperscalers would reopen the bull case.

The most dangerous move right now is reaching for a conclusion before the data exists. This week’s rate decision and late July’s earnings reports are the two scheduled moments where uncertainty resolves. Waiting for those before repositioning isn’t indecision — it’s patience.

This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made solely at the reader’s own judgment and risk. Past market behavior does not guarantee future outcomes.

Leave a Reply