The July 15 Decision: A Rate Hike Is Coming

On July 15, 2026, the Bank of Korea’s Monetary Policy Board convenes — and unlike many recent meetings, this one is widely expected to end with a rate hike. The groundwork has been laid methodically. At its May 2026 meeting, the BOK held its benchmark rate at 2.50% for the eighth consecutive time, but Governor Shin Hyun-song made little secret of the direction: “We will raise rates at an appropriate time,” he said (Bank of Korea, May 28, 2026). Two weeks later, June consumer price inflation came in at 3.2% year-on-year — well above the BOK’s 2% target — all but sealing the decision (Statistics Korea, July 2, 2026).

The real debate now is not whether rates go up on July 15, but by how much. And that distinction matters enormously for anyone carrying a variable-rate loan.

Where the ‘Big Step’ Talk Came From

South Korean financial media has been buzzing with the term “big step” — a 50 basis-point hike, double the standard 25 bps increment. The framing gained traction in mid-June, when some analysts argued that a combination of entrenched inflation and a weak won demanded a stronger-than-usual response. Financial Today went so far as to describe a big step as “likely” on July 10, 2026.

Governor Shin cooled those expectations fairly quickly. When pressed on the possibility, he described his earlier remarks as “speaking in general terms” — a formulation widely read as walking back the big-step narrative (Yonhap News, July 9, 2026). The Seoul Economic Daily reported the same day that “big-step probability has diminished.” That said, the possibility hasn’t been completely ruled out; the BOK has a history of surprising markets.

The most useful frame isn’t to bet on a specific increment, but to stress-test your finances against both scenarios. KB Securities forecasts two hikes — July and October — taking the benchmark to 3.00% by year-end (Businesspost, June 2, 2026). At the other end, some analysts see the terminal rate stopping at 3.25% (Yonhap Infomax, June 29, 2026). The cumulative range under discussion: anywhere from 75 to 100 basis points above today’s 2.50%.

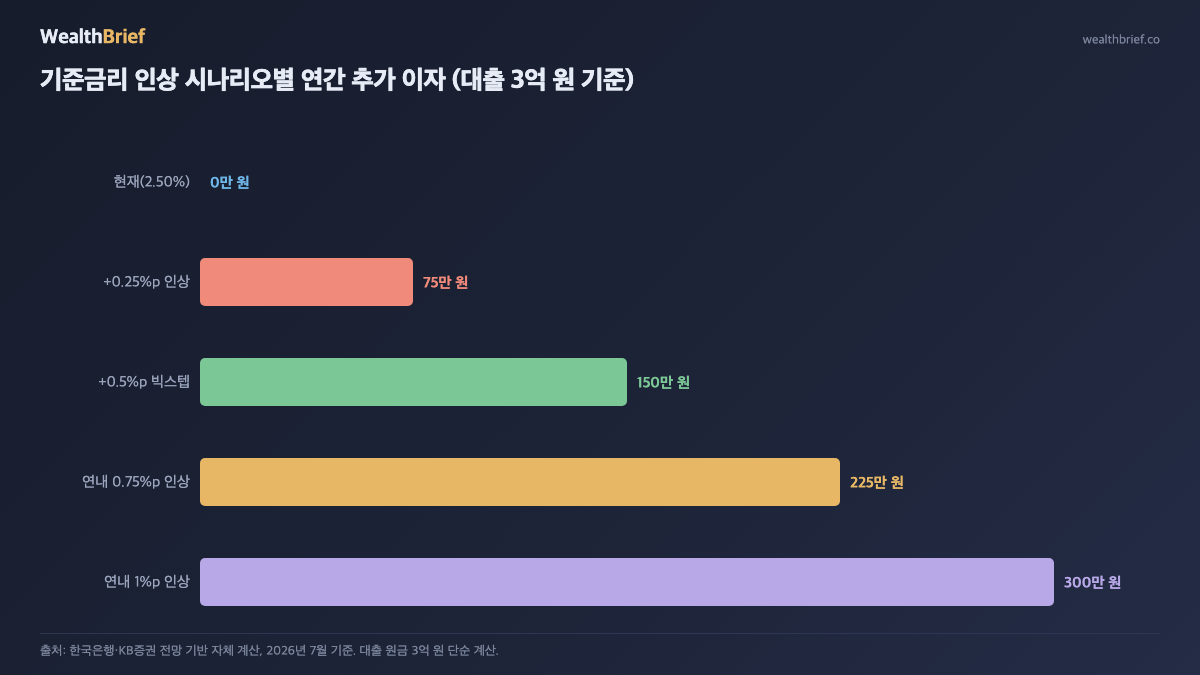

What a Rate Hike Actually Costs You: Scenario Math

For variable-rate borrowers, the transmission mechanism works like this: the BOK raises its policy rate → banks’ funding cost benchmark (called COFIX, or Cost of Funds Index) moves in tandem, typically with a one-to-three-month lag → variable-rate loan interest rates reprice accordingly.

The table below shows estimated additional annual interest costs by loan size, across the two scenarios most actively discussed.

| Loan Principal | +25 bps hike / +0.25%p (annual) | +50 bps hike / +0.50%p (annual) |

|---|---|---|

| ₩100 million | ₩250,000 / yr (≈₩21,000/mo) | ₩500,000 / yr (≈₩42,000/mo) |

| ₩200 million | ₩500,000 / yr (≈₩42,000/mo) | ₩1,000,000 / yr (≈₩83,000/mo) |

| ₩300 million | ₩750,000 / yr (≈₩63,000/mo) | ₩1,500,000 / yr (≈₩125,000/mo) |

| ₩500 million | ₩1,250,000 / yr (≈₩104,000/mo) | ₩2,500,000 / yr (≈₩208,000/mo) |

※ Estimates based on full outstanding principal. Actual costs vary by remaining balance, amortization structure, and spread components. Not financial advice.

A borrower with ₩300 million in variable-rate mortgage debt would absorb roughly ₩125,000 per month in additional interest if the BOK moves by 50 bps. That’s manageable on its own. But if KB Securities’ double-hike forecast plays out, the cumulative burden doubles again by year-end.

Three Things Variable-Rate Borrowers Should Check Now

- Your rate type and reset schedule. Variable-rate loans in Korea reprice on 3-, 6-, or 12-month cycles. Check your loan agreement or banking app to determine when your next repricing date falls — that’s when the hike will actually show up in your payment.

- Whether a fixed-rate switch still makes sense. The window for switching from variable to fixed at a favorable spread narrowed considerably once rate hike expectations became consensus. A switch now will almost certainly come at a higher fixed rate than six months ago — plus potential early repayment fees. Run the break-even math before acting.

- Your “spread” or margin above the base rate. The 가산금리 (add-on spread) that banks layer on top of COFIX can also shift — particularly at loan renewal. In a rising-rate environment, banks sometimes tighten terms on renewal, especially for borrowers with weaker credit profiles or collateral that hasn’t kept pace with assessed values.

Fixed-Rate Borrowers: Not Off the Hook

If you’re locked into a fixed rate, you’re insulated for now — but not indefinitely. Many Korean mortgage products use a hybrid structure: a fixed rate for the first two or three years, converting to variable thereafter. If you took out a loan in 2023 or 2024 at near-cycle lows, your fixed period may be ending in 2026 or 2027 — precisely as rates are moving higher.

Pull up your original loan agreement and find the date your rate converts. If it falls within the next 12 months, start modeling what your monthly payment looks like at 3.00%, 3.25%, and 3.50% on the remaining balance. The number shouldn’t be a surprise.

The Bigger Picture: Back-to-Back Hikes vs. One Big Move

Whether the BOK chooses 25 bps now or 50 bps now is almost a secondary question. The market’s base case — two hikes of 25 bps each — produces the same 50 bps cumulative effect over six months, just distributed across two shocks rather than one. The practical difference for most borrowers is the pace of adjustment.

What matters more is the terminal rate. If the tightening cycle ends at 3.00%, current variable-rate borrowers face a 50 bps total adjustment. If it extends to 3.25%, that’s 75 bps — an additional ₩1.5 million per year on ₩200 million in debt. At 3.50%, the math approaches ₩2 million annually on the same loan.

None of these scenarios are catastrophic in isolation. The risk is that most borrowers find out about the impact not from a proactive review, but from the first payment statement after the hike lands.

This article is prepared for informational purposes based on publicly available news reports and institutional forecasts. It does not constitute financial or investment advice. Actual loan cost changes depend on individual loan terms, remaining principal, and contractual repricing conditions. Consult your lender or a licensed financial advisor before making significant borrowing decisions.

Leave a Reply