The following case is a composite reconstructed from real accounts. Names, amounts, and any identifying details have been anonymized or rounded, and the case does not refer to any specific individual.

The Same Crisis, Three Different Outcomes

Incheon, Michuhol District, autumn 2022. Person A — a salaried worker in their early thirties — signed a jeonse lease on the advice of a real estate agent who assured them it was the safe choice. Jeonse is Korea’s unique deposit-based rental system: instead of paying monthly rent, tenants hand over a large lump sum — typically 60 to 80 percent of the property’s market value — which the landlord returns in full at the end of the lease. For decades, this arrangement worked. That autumn, it didn’t. A’s deposit was roughly ₩200 million. By the time A checked the property registry a year later, the building was already buried under senior-ranking liens. When the property was foreclosed and auctioned off, the proceeds barely covered the creditors ahead in line.

Person B, a self-employed renter in their mid-thirties who lived one floor above, chose litigation. With the landlord in hiding, a court judgment seemed like the only path to recovery. Legal fees ran to several million won. The case dragged on for more than a year. B eventually won — and then received an “unenforceable judgment” because the landlord had no attachable assets left.

Person C, in their late twenties and living on the ground floor, moved differently. C filed immediately for official victim recognition under Korea’s Special Act on Jeonse Fraud Relief, applied for an emergency bridge loan from the Korea Housing Finance Corporation (HF), and covered moving costs within weeks. When the Korea Land and Housing Corporation (LH) announced its distressed-property purchase program, C applied. Six months later, C was living in the same unit — now as a subsidized public tenant.

Three years on, the gap between them is not about luck. It’s about knowing which levers existed and pulling them in the right order.

What Actually Happened — The Scale and the Law

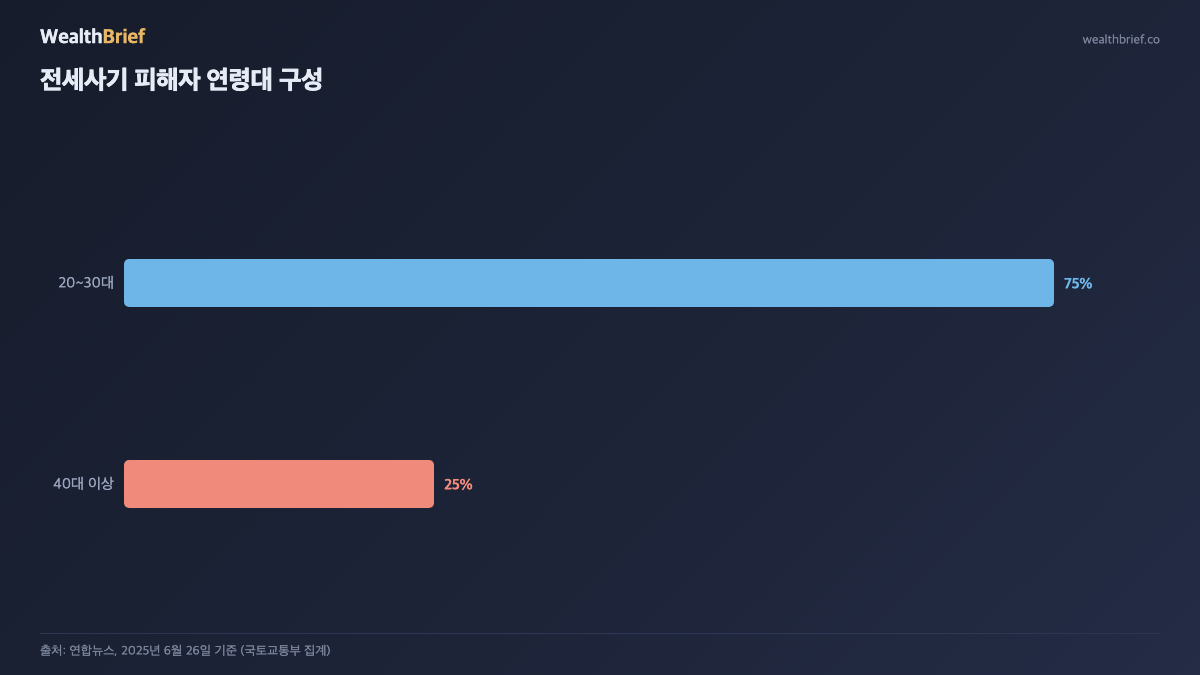

South Korea’s jeonse fraud crisis peaked in 2022 and 2023, concentrated in the greater Seoul metropolitan area. As of May 6, 2026, the Ministry of Land, Infrastructure and Transport had officially recognized a cumulative 38,503 cases of jeonse fraud victimization.[1] Three-quarters of all recognized victims were in their twenties or thirties; 60 percent lived in the greater Seoul area.[2] In 97.6 percent of cases, the lost deposit was ₩300 million or less — for most victims, the entirety of years of savings.[3]

The Special Act on Support for Jeonse Fraud Victims and Housing Stability came into force in June 2023. A strengthened amendment — centered on a “pay now, recover later” mechanism — passed the National Assembly on May 28, 2024, pushed through by the then-opposition Democratic Party without the participation of the ruling People Power Party. Under the revised law, the Korea Housing and Urban Guarantee Corporation (HUG) would use the Housing and Urban Fund to purchase victims’ lease-deposit return claims outright, providing upfront compensation, and then pursue the landlord for recovery through subrogation rights.[4]

Floor leader Choo Kyung-ho of the People Power Party said the party would ask President Yoon Suk-yeol to veto the bill, calling it fundamentally flawed.[4] The presidential office indicated the legislation was unacceptable. A veto followed. After the 22nd National Assembly convened, a revised version passed with bipartisan support in August 2024. By March 2026, LH had completed more than 6,000 distressed-property purchases under the program.[5]

WealthBrief Analysis — Why This Keeps Happening

Three structural layers made jeonse fraud possible at scale.

First, the property registry blind spot. Tenants were responsible for pulling their own certified registry extracts (deunggibu deungbon) before signing. The legal obligation on real estate agents to proactively flag senior-ranking liens was ambiguous and weakly enforced. Many renters — especially first-timers moving to a new city — trusted the agent’s word. By the time they discovered that combined senior liens exceeded the auction value, they were already locked in.

Second, the zero-rate vintage. During Korea’s near-zero-interest-rate years from 2020 to 2021, jeonse deposits inflated toward 80–90 percent of purchase prices — so-called “empty-shell” (kkang-tong) properties. When rates rose sharply in 2022 and property values fell, landlords who had used deposit proceeds as operating capital found themselves with no way to repay. Some of these landlords were not fraudsters in the conventional sense; the math had simply inverted on them.

Third, jeonse itself as a structural anomaly. Jeonse is a product of Korea’s decades-long housing shortage and high savings culture. In effect, tenants extend an interest-free loan to landlords, secured against the property. When asset values rise, both sides gain. When they fall, the junior creditor — the tenant — absorbs the first loss. The system carries embedded directional risk that most renters never priced in.

The relief framework is real and growing, but gaps remain. Obtaining formal victim recognition takes time; the property sale and settlement process takes longer. New variants — trust-deed fraud, in which buildings are registered under financial trust structures that bypass standard protections for tenants — continue to emerge. The law is catching up, but not instantaneously.

If You Are About to Sign a Jeonse Lease — A Checklist

- Pull the registry extract yourself, the day of signing: Do not rely on a copy handed to you by the landlord or agent. Request a fresh certified copy from the Supreme Court registry system. If the combined senior-ranking liens plus your deposit exceed roughly 80 percent of the estimated market value, treat it as a red flag.

- Verify jeonse deposit insurance eligibility before contract: Check whether the property qualifies for coverage under HUG or HF’s deposit return guarantee programs. Properties that fail the eligibility screen fail for a reason.

- Register and get your official date-stamp on move-in day: Complete your jeonse registration (전입신고) and secure a certified date stamp (확정일자) the same day you pay the balance. A single day’s delay drops you behind any lien filed in the interim.

- Know the response sequence if things go wrong: (1) File a report with your local government. (2) Apply for official victim recognition through the Ministry of Land’s Jeonse Fraud Victim Support Committee. (3) Apply for an HF emergency bridge loan and the LH distressed-property purchase program. (4) Pursue litigation as a last resort — a favorable court judgment is worth nothing if the landlord has no reachable assets. The Korea Legal Aid Corporation provides free legal support.

- Watch for trust-deed properties: If the registered owner is a trust company rather than an individual landlord, the contractual structure differs materially. A lease signed without the trustee’s explicit consent may not carry standard tenant protections.

Sources

- Marketin, “Jeonse fraud victims reach cumulative 38,503 decisions… distressed property purchases accelerating,” May 6, 2026 (data as of May 6, 2026)

- Yonhap News, “60% of jeonse fraud victims are from greater Seoul… 75% are in their 20s–30s,” June 26, 2025, https://www.yna.co.kr

- Nongmin Sinmun, “Jeonse fraud toll keeps rising… 97.6% of cases involve deposits of ₩300 million or less,” March 4, 2026

- News1, “‘Special Jeonse Fraud Act’ passes National Assembly with opposition only… Choo Kyung-ho: ‘Will recommend a presidential veto’,” May 28, 2024, https://www.news1.kr/articles/5430000

- ChosunBiz, “Jeonse fraud victim recognition rate 62.2%… distressed property purchases exceed 6,000 units,” March 4, 2026

Disclaimer: This article is for informational purposes only and does not constitute investment advice or a financial recommendation. Outcomes vary by individual circumstance. Any investment decision is made at your own risk. WealthBrief bears no liability for results based on this content.

Leave a Reply