Mortgage Doors Closed. Now They’re Shutting Personal Loans Too

Walk into a Korean bank branch in the third week of June, and you’ll notice the quiet. Mortgage lending has been tightened for months, and now banks are pulling back on personal (unsecured) credit lines as well. According to a June 20, 2026 report from christiandaily.co.kr, as mortgage borrowers were redirected toward personal credit, banks detected the surge and clamped down there too. For someone genuinely trying to buy a home or renew a lease, the exits are narrowing simultaneously.

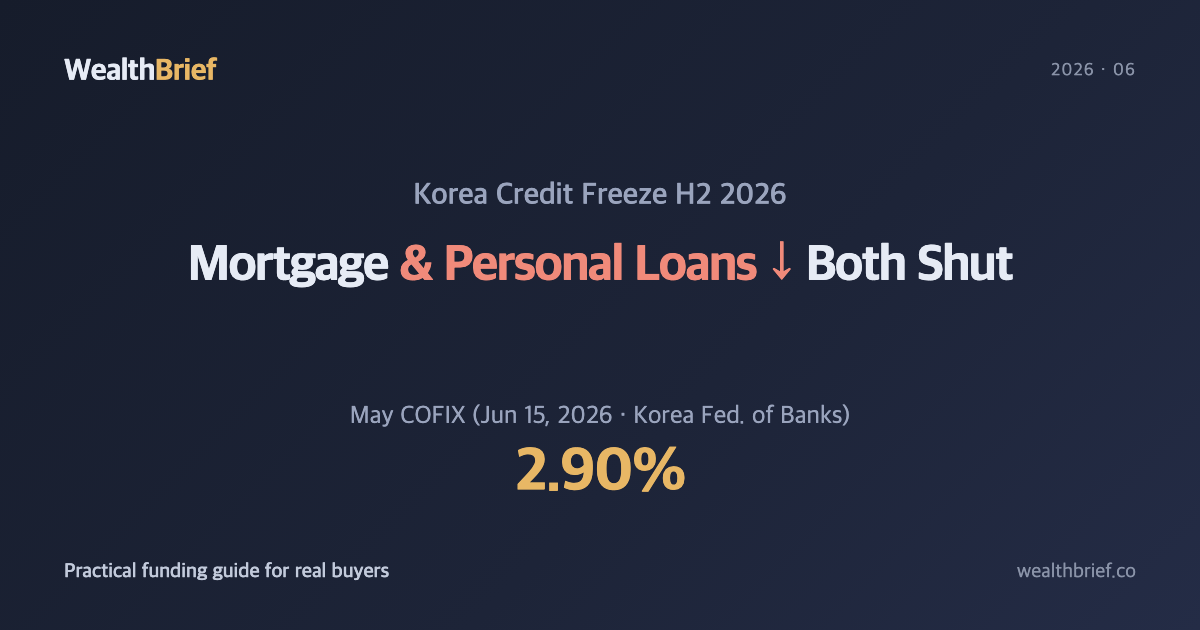

Start with the numbers that matter. On June 15, 2026, the Korea Federation of Banks published the May COFIX (Cost of Funds Index) at 2.90%, up 0.01 percentage points from April — the second consecutive monthly increase (source: Yonhap News). COFIX is the benchmark for variable-rate mortgages in Korea; when it rises, borrowers on floating-rate loans see their monthly payments recalibrated upward at the next reset date, typically every six or twelve months.

The group most exposed to this creep is substantial. A June 17, 2026 Newsis report found that roughly one in two mortgage holders in Korea currently carries a variable-rate loan. That means a significant share of homeowners has been silently absorbing higher costs each reset cycle — and will continue to do so as long as COFIX trends up.

Jeonse (Rental Deposits) Aren’t the Safe Harbor They Used to Be

Many Koreans’ fallback — renting on a jeonse (전세) contract, where a large lump-sum deposit replaces monthly rent — is under similar pressure. The Korea Construction & Economy Research Institute projected in a June 18, 2026 Yonhap report that jeonse prices will rise 5% in the second half of 2026 (with home purchase prices rising around 2.5%). Deposits are going up just as the loans needed to fund those deposits are becoming harder to secure.

Fraud risk adds another layer. The government announced plans to overhaul the Safe Jeonse App (안심전세앱) in September 2026, adding pre-contract screening for tax delinquencies, senior liens, and other red flags — making it easier to spot problem landlords before signing (Newsis, June 18, 2026). Until that upgrade rolls out, renters entering contracts now have no automated safety net. Manual checks remain the only defense: pull the property registry (등기부등본), request proof that the landlord has no outstanding national or local taxes, and verify eligibility for jeonse deposit insurance (전세보증보험) before transferring any money.

A Practical Map — Where You Stand Right Now

Understanding the regulatory environment is only useful if it tells you what to do next. Three common situations, and what each one calls for:

| Situation | Core Risk | Check This First |

|---|---|---|

| Holding a variable-rate mortgage | Rising COFIX translates directly to higher monthly payments at each reset | Remaining loan term, cost of switching to fixed rate vs. projected interest increase |

| Facing a jeonse renewal | Deposit increase but borrowing capacity reduced | Whether jeonse insurance covers the new amount (typically capped at 80% of appraised value), landlord’s tax status |

| Planning to buy for the first time | DSR caps mean the loan you qualify for may be smaller than you expected | Recalculate your maximum loan under DSR 40% at current income; check eligibility for policy mortgage products |

Should You Switch to a Fixed Rate Now?

Two consecutive months of COFIX increases do not by themselves make fixed-rate conversion the right call. The math depends on three things: the early repayment fee on your current loan (usually 0.5–1.5% of outstanding principal), the current spread between your variable rate and available fixed rates, and your read on where rates go from here.

A rough rule of thumb: if you have more than three years left on the loan, the gap between your variable and fixed options exceeds 0.5 percentage points, and you see meaningful further rate risk, conversion is worth pricing out carefully. If your variable rate is already within 0.2–0.3 points of the fixed option, the fee often wipes out the benefit — especially if you’re within the early repayment penalty window (typically the first three years of the loan).

This is general logic, not personalized advice. Your tax situation, cash flow, and refinancing eligibility will shift the conclusion.

Alternative Funding Channels — and Their Traps

When the major bank window closes, other channels remain. Each comes with conditions worth understanding before relying on them.

- Policy mortgage products (Teukrye Bogeumjari, Didimtol, Beotime): These carry income and asset thresholds, but often come with DSR carve-outs or subsidized rates. Check eligibility at the Korea Housing Finance Corporation (HF) website before assuming you qualify.

- Internet banks and savings banks (상호저축은행): May offer different limits than the big commercial banks, but typically carry higher lender spreads (가산금리 — the markup a bank adds to the base rate as its profit margin). Compare the all-in rate, not just the headline figure.

- Online P2P lending (온투업): Demand surged as borrowers sought regulatory workarounds — outstanding balances grew by roughly 140 billion won in a single month earlier this year, according to a February 2026 Global Economic report. Regulators are watching. Rates are higher, principal is at risk, and further restrictions are a live possibility.

How Much Debt Is Too Much Right Now?

In an environment where borrowing costs are rising, revisiting your leverage ceiling is worth the discomfort. A common reference point in Korean financial planning is keeping total household debt within five to six times annual income — beyond that range, the ability to absorb a rate increase or income interruption deteriorates quickly. This is a rough benchmark, not a universal rule.

The more actionable check: is your total debt service ratio (DSR) under 40%? If it is, you’re within the regulatory threshold and likely have some buffer. If it’s close to the limit, a modest rate increase could push your monthly obligations into uncomfortable territory without any change in income.

The question right now is not how much you can borrow — it’s how much you can still service if rates move another half-point higher or income drops temporarily. Build your loan size around that ceiling, not the maximum the bank will approve.

This article is for informational purposes only and does not constitute financial or investment advice. Consult a licensed financial professional before making any borrowing or investment decisions.

Leave a Reply