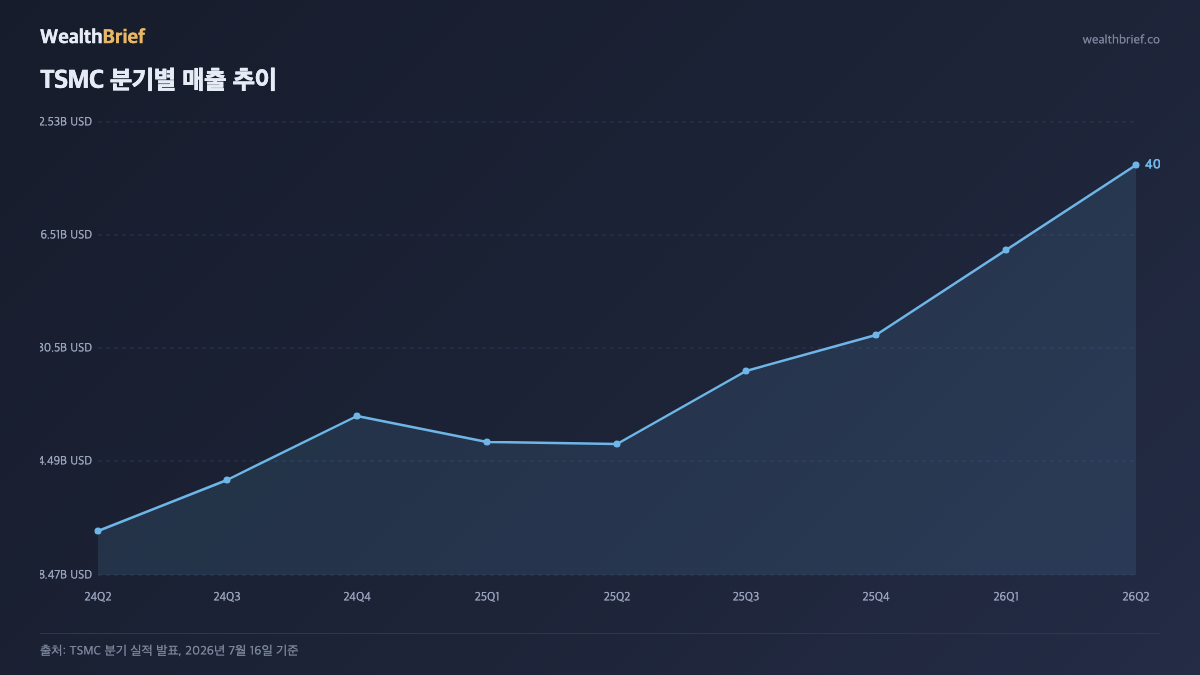

TSMC Q2 2026: The Numbers That Matter

On July 16, 2026, TSMC reported its second-quarter results — and blew past every forecast. Revenue hit $40.2 billion, a new all-time high for the fifth consecutive quarter, while net profit surged more than 77% year-on-year to approximately NT$1.13 trillion (around $22.6 billion USD). (Source: TSMC Q2 2026 earnings release, July 16, 2026)

Operating profit growth reached 65%. The company also raised its Q3 and full-year 2026 guidance, citing what management called “robust and continuing AI demand” on the earnings call.

| Metric | Q2 2025 | Q2 2026 | Change |

|---|---|---|---|

| Revenue | ~$25.4B | $40.2B | +58% |

| Net Profit | ~$12.8B | ~$22.6B | +77% |

| Operating profit growth | — | — | +65% |

| Consecutive record quarters | 4 | 5 | New record |

Source: TSMC Q2 2026 earnings release (July 16, 2026). USD figures based on prevailing exchange rates as of July 16, 2026.

How AI Demand Is Structurally Reshaping the Foundry Market

This isn’t just “AI chips selling well.” The structural shift runs deeper. A single AI accelerator die is five to ten times larger than a smartphone application processor, and it demands leading-edge nodes — 3nm today, 2nm tomorrow.

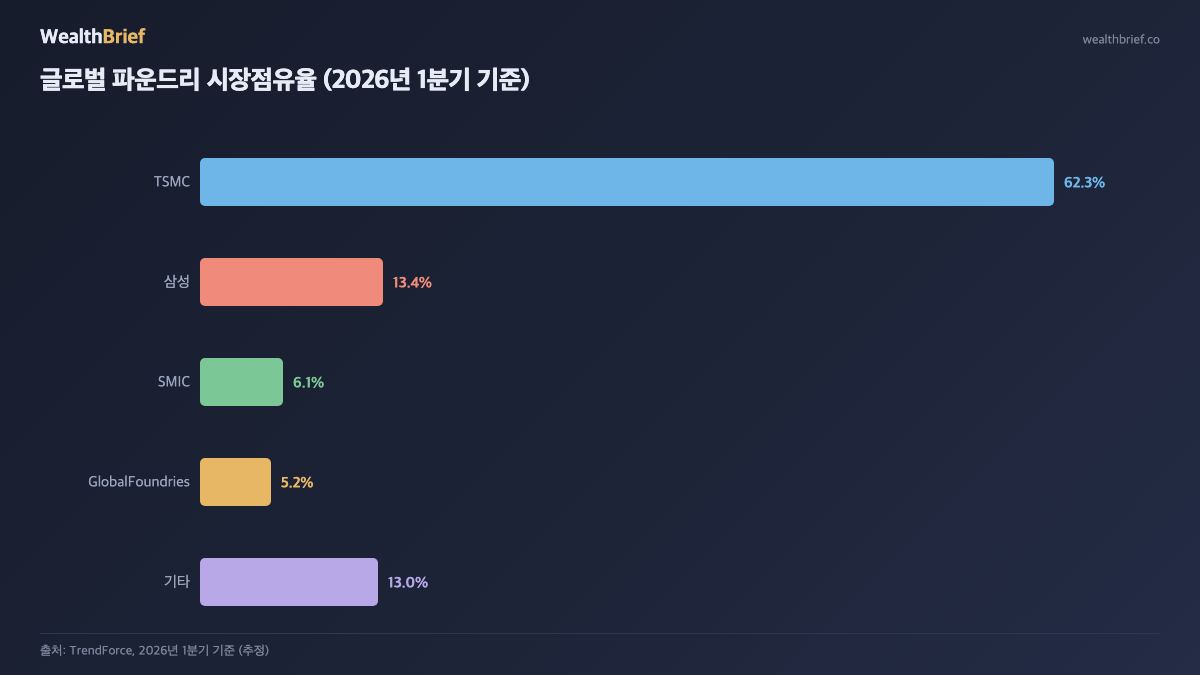

That creates a compounding advantage for TSMC. First, larger dies mean more wafer area per chip, driving up average selling price (ASP) even before accounting for process premiums. Second, AI customers — Nvidia, AMD, Apple — have no credible alternative to TSMC for leading-edge logic. That pricing power is structural, not cyclical.

TSMC’s management was unusually direct on the earnings call: “AI demand remains robust.” The upward guidance revision translates that confidence into hard numbers.

3 Signals for Korean Semiconductor Investors

TSMC’s blowout quarter doesn’t exist in isolation. Paired with ASML’s strong Q2 results, it signals broad health across equipment, materials, logic, and memory. Here are the three most actionable implications for Korea’s semiconductor value chain.

Signal 1 — Samsung Foundry’s Path to Profitability Gets Clearer

Samsung’s foundry division has posted cumulative operating losses since 2023. But in a market where TSMC’s capacity is oversubscribed, customers have reason to develop a second source.

Samsung’s Gate-All-Around (GAA) process yield improvements have been reported in industry media (Source: Electronic Times, July 2026). That said, translating improved yield into actual new orders typically takes two to four quarters — investors pricing in a quick turnaround should temper expectations accordingly.

Signal 2 — SK Hynix HBM Benefits Directly from TSMC’s Order Book

Every AI accelerator pairs a logic die (made by TSMC) with High Bandwidth Memory, or HBM — a high-performance memory type built by stacking DRAM chips vertically to achieve much faster data transfer rates. SK Hynix and Samsung are the primary HBM producers. More TSMC-made accelerators shipped means proportionally more HBM units demanded.

SK Hynix holds an estimated 50%+ share of HBM supply to leading AI accelerator customers as of H1 2026, driven in part by its lead in HBM3E — the current highest-specification HBM generation. (Source: industry estimates, H1 2026.) As long as that share holds, TSMC’s upward guidance functions as a leading indicator for SK Hynix’s next earnings print.

Signal 3 — Extended Foundry Capex Cycle Reshapes Equipment and Materials Demand

Semiconductor equipment and materials companies typically lag foundry capex decisions by six to twelve months. TSMC’s announcement of an additional $102 billion (approximately ₩148 trillion) investment in U.S. fabs (Source: TSMC, July 16, 2026) implies order momentum that could sustain into 2027.

One counterpoint worth noting: U.S.-based fab investments skew toward U.S. and Japanese equipment suppliers over Korean ones. Korean equipment firms may capture less of this particular wave than domestic headlines suggest.

Three Checkpoints Before the Next Earnings Season

| Checkpoint | Why It Matters | When to Check |

|---|---|---|

| TSMC Q3 guidance delivery | If TSMC meets its raised Q3 guidance, the foundry super-cycle narrative holds. A miss signals potential demand softening. | TSMC Q3 earnings, October 2026 |

| KRW/USD exchange rate | TSMC reports in USD. A strengthening Korean won erodes the KRW-denominated return on Korean semiconductor holdings even when underlying business is strong. | Weekly monitoring |

| Nvidia & AMD customer inventory levels | If hyperscalers are sitting on AI chip inventory, new orders to TSMC slow — a leading indicator for the next quarter’s foundry demand. | Nvidia and AMD quarterly earnings |

The exchange rate point is easy to overlook. Even if TSMC’s business continues to fire on all cylinders, a sharp KRW appreciation could compress returns for Korean investors holding related equities.

3-Line Summary

- TSMC posted a fifth consecutive record quarter in Q2 2026: revenue $40.2B (+58% YoY), net profit up 77% — a clear earnings surprise with guidance raised further. (Source: TSMC, July 16, 2026)

- AI accelerator demand is structurally — not cyclically — lifting foundry pricing power, opening realistic paths to profitability for Samsung Foundry and extending SK Hynix’s HBM tailwind.

- Before the next earnings season, track three variables: TSMC Q3 guidance delivery, KRW/USD moves, and inventory levels at Nvidia and AMD.

This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own judgment and at your own risk. Figures cited reflect stated sources and reference dates and may have changed since publication.

Leave a Reply